A new digital insurer has begun operations in India with a motor insurance product for private cars, entering a general insurance sector that analytics firm GlobalData forecasts will reach US$62.2 billion in gross written premium by 2030.

Kiwi General Insurance, founded by Neelesh Garg and Saurav Jaiswal, obtained regulatory approval in March 2026. The company is financially backed by Westbridge Capital and runs on a technology platform built entirely in-house. Its first product targets the private car motor insurance segment, with its design centred on the claims experience rather than premium pricing alone.

Motor insurance is the second-largest line of business in India’s general insurance market, accounting for 31.7% of gross written premium in 2025, according to GlobalData. Despite its scale, customer dissatisfaction with claims handling has been a persistent issue across the sector. Kiwi’s product attempts to address several of the friction points that discourage policyholders from filing claims. Under its no-claim bonus structure, branded “Super NCB,” a customer who files a claim steps down only one level on the discount scale rather than losing the full accumulated benefit. The company says this results in policyholders retaining up to 40% more discount compared with conventional no-claim bonus arrangements.

A second feature, “Flexi Repair,” allows customers to defer minor repair claims and consolidate them with a larger claim at a later date. Under standard policy structures, each individual claim – however small – attracts a compulsory deductible, which discourages policyholders from filing for minor damage. By allowing customers to bank smaller damages for later settlement, the feature reduces the out-of-pocket cost exposure that typically accompanies multiple separate claims.

The company also offers same-day cash transfers to a policyholder’s bank account when a vehicle is booked for repair. Called “InstaCash,” the transfer does not require the customer to file a claim first. For repairs carried out at garages outside Kiwi’s cashless network, a separate mechanism called “PayFirst” provides an instant payout at the point of repair, allowing policyholders to use a garage of their preference without bearing upfront costs. For its distribution network, Kiwi offers digital onboarding, reconciliation tools, performance dashboards, and claim tracking systems accessible to agents.

Neelesh Garg, founder of Kiwi General Insurance, pointed to entrenched industry practices as the problem the company was set up to solve. “The insurance industry has long been shaped by legacy processes that create customer apprehension. Our goal is to rebuild it from first principles using technology, data, and disciplined execution. We are focused on making insurance simple, fast, and consistent,” Garg said.

Saurav Jaiswal, managing director and chief executive officer, framed the company’s focus around predictability at critical moments. “Customers today expect clarity, speed, and reliability, especially in moments that matter. From instant policy issuance and real-time claim tracking to faster decisions and single-point ownership, every element is designed to reduce ambiguity. Starting with motor insurance, we aim to set a new standard for how insurance is delivered,” Jaiswal said. The company has indicated it will extend into other insurance lines in the months ahead.

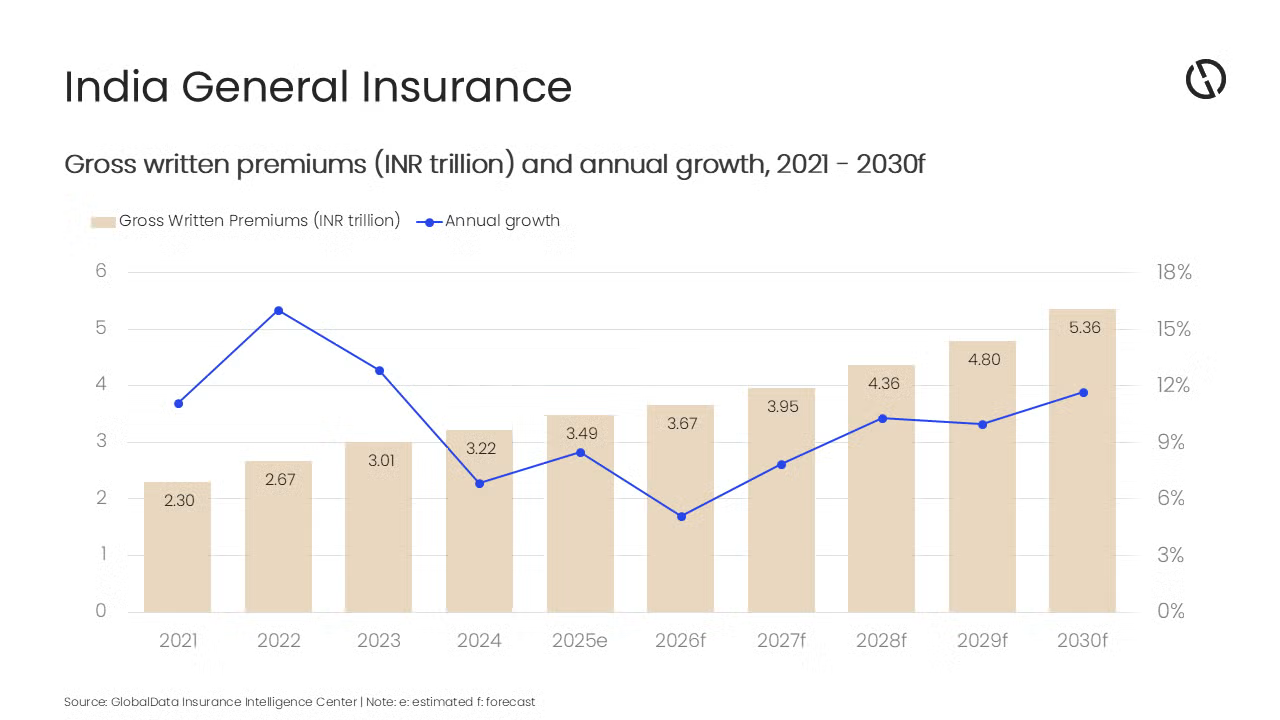

Kiwi’s market entry comes as India’s general insurance sector is undergoing structural changes on multiple fronts. GlobalData projected in April 2026 that the industry will expand at a compound annual growth rate of 10.0% between 2026 and 2030, climbing from INR3.6 trillion (US$43.4 billion) to INR5.4 trillion (US$62.2 billion). Premium growth in 2026 is expected to moderate to 5.1% following a post-GST-reform surge before picking up pace again from 2027.

Within the motor segment, GlobalData noted a shift toward electric vehicle insurance, reflecting higher vehicle values and greater component complexity. Usage-based products tied to telematics have also gained ground. Swarup Kumar Sahoo, senior insurance analyst at GlobalData, observed that some digital distribution channels have been assigning dedicated claims managers, coordinating with garages and surveyors, and pushing for faster dispute resolution on behalf of policyholders.

On pricing, Sahoo pointed to cost pressures in the segment. Car insurance premiums face upward pressure as reinsurers reprice catastrophe exposure and repair-cost inflation rises, he said. Sahoo also cautioned that the West Asia crisis has already pushed up risk premiums for marine, aviation, and transit business, as well as construction costs in India, with potential knock-on effects across the broader economy. Regulatory reforms at the industry level, including provisions for 100% foreign direct investment and composite licensing, are expected to draw additional capital into the sector and support product development over the medium term, according to GlobalData.