Malaysia’s general insurance industry recorded higher underwriting profits in 2025, with gains in fire, marine, and personal accident classes helping to counter continued losses in motor, according to data from the General Insurance Association of Malaysia (PIAM).

PIAM reported that the general insurance market generated gross written premium (GWP) of RM24.2 billion in 2025, up 4.8% from RM23.1 billion a year earlier. Underwriting profit increased to RM1.2 billion, RM125 million higher than in 2024, with the industry’s overall combined ratio reported at about 93%. Motor insurance remained the largest class of business, contributing 45.2% of total premiums. Fire insurance accounted for 20.9%, while personal accident (PA) represented 6.5%. Taken together, motor, fire, and PA delivered overall premium growth of 6.1% for the general insurance sector in 2025.

“The improvement in the general insurance industry’s underwriting performance is an operational milestone and reflects the sector’s ability to absorb rising claims costs while continuing to protect millions of policyholders. As we strengthen industry resilience; our focus remains on building a well-insured nation, ensuring a faster recovery for Malaysians with their assets, livelihoods, and operations safeguarded through the support of our insurers and reinsurers,” said PIAM chief executive officer Chua Kim Soon.

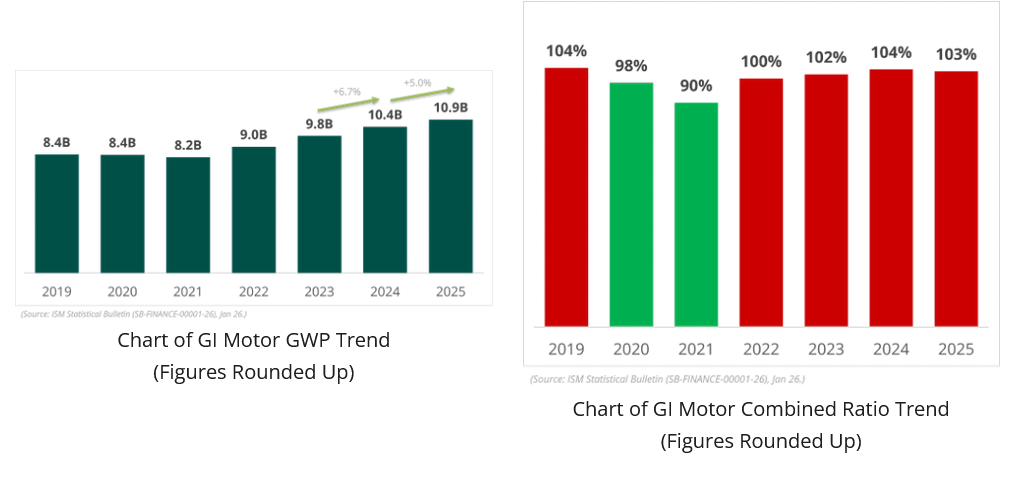

Motor GWP rose to RM10.9 billion in 2025, representing year-on-year growth of 5.0%, compared with 6.7% in 2024. Despite the increase in premiums, the motor segment remained in an underwriting loss position, with a deficit of RM289.3 million and a combined ratio of 103%. The modest improvement of 0.7 percentage point in the combined ratio relative to 2024 was linked to stricter underwriting practices. However, higher costs in the private car segment continued to push claims above premiums. Claims experience reflected both sustained frequency and higher average claim amounts. Private car claim frequency remained above 7% during 2025, with higher incidence observed in high-volume models such as the Proton X50 and X70, where a larger share of drivers are younger. Average claim severity for private cars increased to RM8,831, reflecting spare parts inflation across models including the Proton Saga and Proton X50.

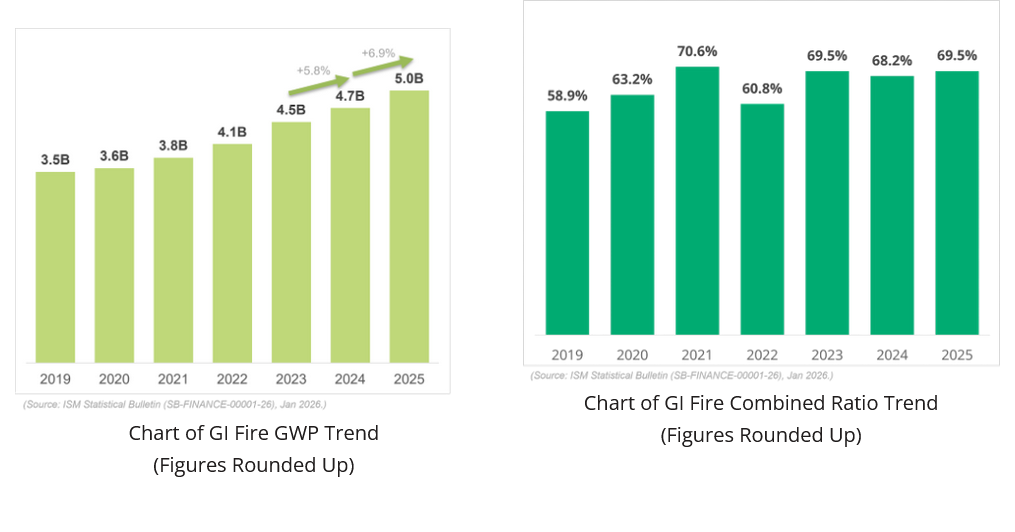

Fire insurance, the second-largest class in the portfolio, posted GWP of RM5.0 billion in 2025, compared with RM4.7 billion in 2024, an increase of 6.9%. The line reported underwriting profit of RM700.8 million and a combined ratio of 69.5%. Premium growth in fire was attributed to higher sums insured on residential sub-sales and rising rebuild costs, with more exposure associated with older landed properties in suburban areas.

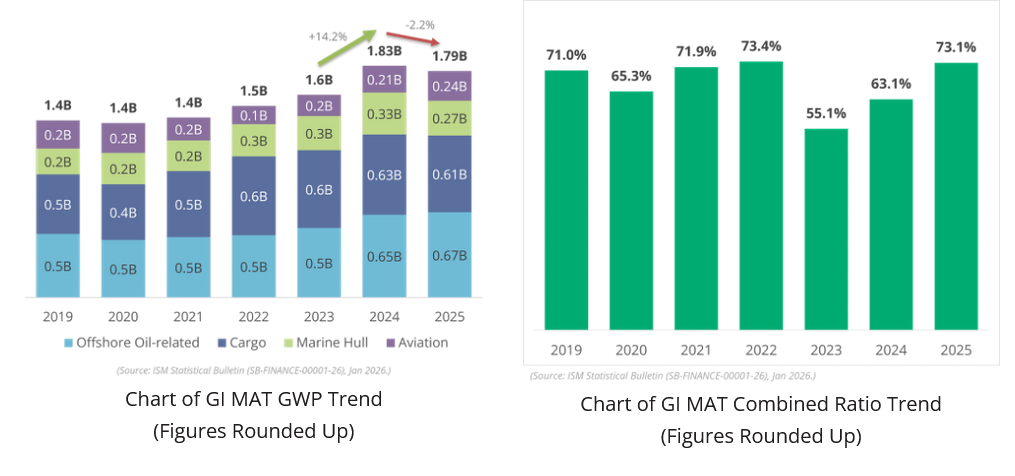

Marine, aviation, and transit (MAT) business saw a small decline in top-line premium but remained profitable overall. MAT GWP decreased 2.2% to RM1.79 billion from RM1.83 billion in 2024, amid softer conditions in offshore oil-related and cargo segments. These two segments accounted for 37.6% and 33.9% of the MAT portfolio, respectively. The MAT class generated underwriting profit of RM108.1 million with a combined ratio of 73.1%, lower than the RM161.8 million in underwriting profit reported for 2024. Cargo and marine hull lines together accounted for nearly 90% of MAT business.

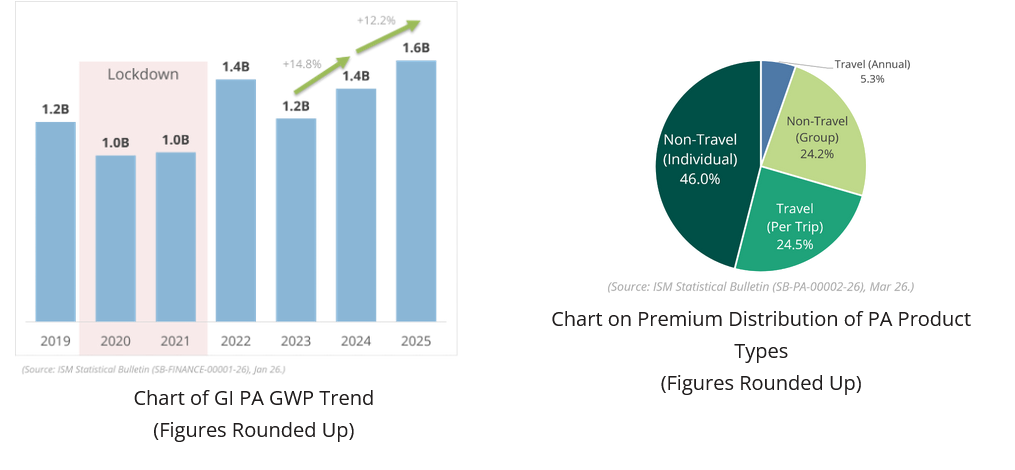

Personal accident insurance continued to expand in volume. GWP in PA rose 12.2% to RM1.6 billion in 2025 from RM1.4 billion in 2024. Higher demand for travel insurance, in line with ongoing recovery in outbound travel since 2023, together with wider adoption of digital distribution and a firmer economic backdrop, supported premium growth. Policy uptake was particularly strong for destinations where the ringgit provides relatively higher purchasing power.

PIAM noted that general insurers are placing emphasis on underwriting discipline, operating efficiency, and product development in areas such as electric vehicle cover, protection for climate-related perils, and digital distribution capabilities. Key factors shaping the operating environment include:

Read next: Malaysia’s RESET reform puts pressure on health insurers as costs sharply climb

At the community level, the industry continues to run road safety and theft-prevention programs, working with partners including VTAREC. Under the government-backed Perlindungan Tenang Voucher 3.0 initiative, 67,946 policies had been issued and RM2.04 million in vouchers redeemed as of April 14, 2026. The Digital Roadside Assistance application provides additional tools for motor claims handling, including real-time assistance, access to authorised towing services, and digital claims submission where available. Through collaboration with the Financial Industry Collective Outreach (FINCO), general insurers are also working with schools and communities in disaster-prone areas on disaster preparedness and insurance awareness.

Looking beyond 2025, GlobalData projects that Malaysia’s general insurance market will grow at a compound annual growth rate of 6.6%, from MYR24.6 billion in 2025 to MYR31.8 billion in 2029 in terms of GWP. Motor, property, and personal accident and health lines made up 82.6% of general insurance premiums in 2024 and are expected to remain the main contributors to premium growth over the forecast period. The combination of higher aggregate underwriting profit, ongoing structural pressure in motor, and a forecast expansion in overall premium volume points to a market where pricing, claims management, and capital deployment across lines will continue to be central considerations in Malaysia’s general insurance sector.