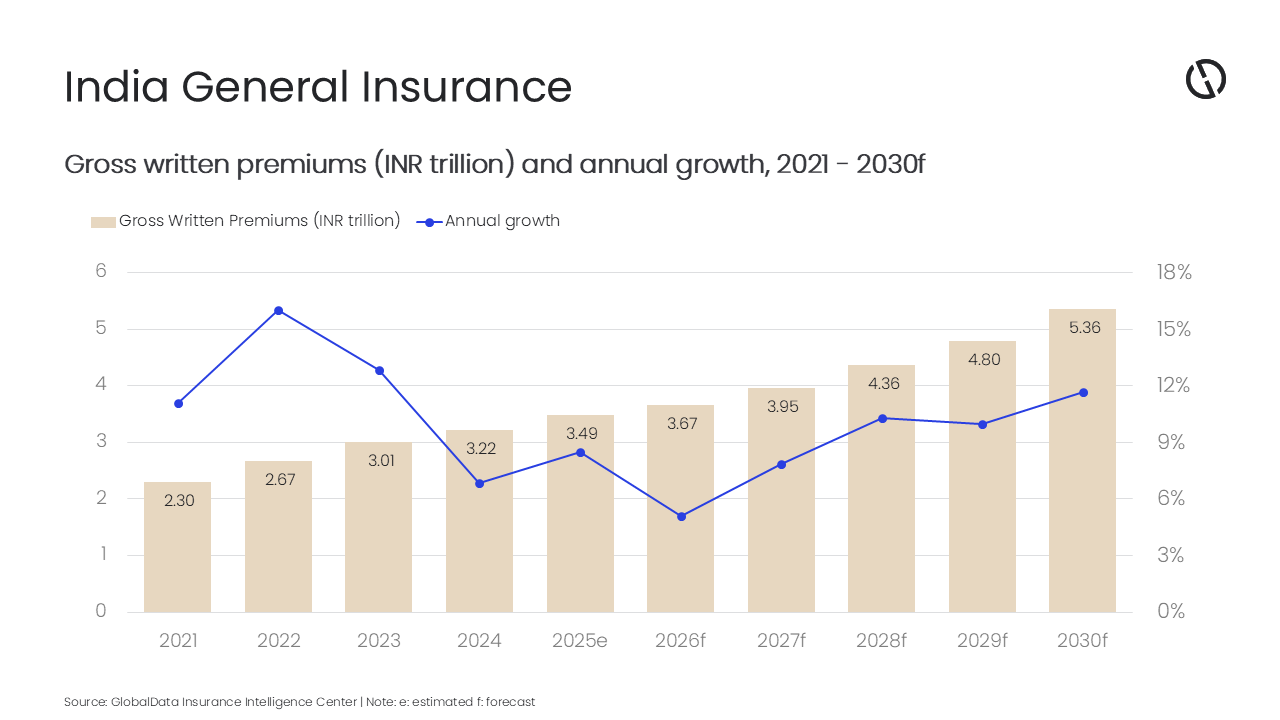

India’s general insurance sector is projected to reach INR5.4 trillion (US$62.2 billion) in gross written premium (GWP) by 2030, driven by regulatory change, digital channels, and shifting product mix, according to GlobalData. Data from GlobalData’s Insurance Database indicates that non-life premiums are expected to grow at a compound annual growth rate (CAGR) of 10% between 2026 and 2030, from an estimated INR3.6 trillion (US$43.4 billion) in 2026. The firm forecasts premium growth of 8.5% in 2025, easing to 5.1% in 2026 as the market adjusts after the post-GST surge and accounting changes, with faster growth expected from 2027. Motor and health lines together accounted for 72.6% of general insurance premiums in 2025, making them the largest contributors to portfolio risk and revenue for domestic carriers and for regional reinsurers with exposure to India.

GlobalData links the expected expansion of the sector to technology adoption and a series of policy initiatives over the past few years. “Digitalization of sales and claims processing, GST exemptions on key retail lines, and strong auto and health insurance demand have supported growth during 2021-25. Growth during 2026-30 is expected to be driven by stronger policyholder protection, faster claims settlement, and broader catastrophe-risk coverage,” said Swarup Kumar Sahoo, senior insurance analyst at GlobalData.

India’s reform agenda has included permitting 100% foreign direct investment, expanding the powers of the Insurance Regulatory and Development Authority of India (IRDAI), and advancing plans for composite licensing. According to GlobalData, these measures are expected to draw additional capital, enable wider product development, and reinforce policyholder safeguards, with the stated goal of narrowing the country’s protection gap. Sahoo said reforms to strengthen insurance’s role as “invisible infrastructure,” with a focus on inclusion and climate resilience, are expected to bolster market penetration in Tier II and Tier III cities and among micro, small, and medium enterprises.

Personal accident & health (PA&H) has become the largest general insurance line by premium, accounting for 40.9% of non-life GWP in 2025, up from 35.7% in 2021. The segment is projected to increase by 8.8% in 2026. Affordability measures, such as the removal of GST on retail health policies from September 2025, have lowered the cost of cover for households and coincided with higher new business. In the fourth quarter of 2025, standalone health insurance premiums rose 13.2% quarter on quarter.

However, GlobalData notes that growth has been accompanied by operational and service challenges. Policyholder grievances have increased, and recent regulatory penalties over claims handling and governance have drawn attention to execution risks for carriers. “New product launches with extensive OPD and wellness coverage signal aggressive product innovation aimed at reducing out-of-pocket costs. However, rising grievances and recent regulatory penalties over claims and governance lapses highlight service gaps and the regulator’s resolve to protect policyholders and enforce standards,” Sahoo said.

Motor insurance remains the second-largest general line, contributing 31.7% of GWP in 2025. The line is undergoing change as electric vehicles (EVs) account for a larger share of new sales, adding higher vehicle values and technology-based components to claims and underwriting considerations. Usage-based and telematics-linked products are seeing broader adoption, offering mileage- and behaviour-related pricing and more granular segmentation.

Digital brokers are also expanding their involvement in the claims process by assigning dedicated claims managers, coordinating with garages and surveyors, and managing dispute escalation. These intermediaries are placing more emphasis on electronic documentation instead of paper-based processes to streamline handling and reduce processing times. At the same time, primary insurers are facing upward pressure on motor rates as reinsurers revisit catastrophe assumptions and as repair-cost inflation remains elevated. Strong auto sales in 2025 have continued to support motor premium volumes despite these pressures.

On the property side, state governments have begun to formalize disaster risk transfer mechanisms. A disaster home insurance program has been approved that combines parametric triggers for faster payouts with indemnity cover of up to INR1 million for families below the poverty line. The program is intended to reduce reliance on ad hoc fiscal relief and address protection gaps for climate-exposed households, contributing to the development of disaster and catastrophe pools that may attract regional and global reinsurance interest. Property insurance accounted for 20.2% of general insurance GWP in 2025. Planned infrastructure spending of about US$128.6 billion in 2026-27 – together with ongoing investment in housing, transport, and urban projects in Tier II and Tier III cities – is expected to sustain demand for engineering, construction, and property covers over the medium term.

Sahoo concludes: “India’s general insurance industry is expected to grow on the back of strengthening policyholder protection, product innovation in motor and health, the expansion of parametric and disaster pools to manage climate risk, and a step-up in digital claims and distribution. Reforms such as tax exemption, GST reliefs, and stronger grievance redressal – paired with robust digital platforms and disciplined natural catastrophe (Nat-Cat) pricing – position the market for sustained premium growth. However, insurers need to remain watchful about the impact of the West Asia crisis, which has already increased risk premiums for marine, aviation, and transit (MAT) business, and construction costs in the country, with an expected wider impact on the economy.”

Alongside non-life expansion, GlobalData expects India’s life and standalone health segments to continue growing over the medium term. The life insurance market is projected to increase from INR9.2 trillion (US$110.2 billion) in GWP in 2024 to INR14.6 trillion (US$170.0 billion) in 2029, representing a compound annual growth rate of 9.6%. By 2025, life premiums are estimated to reach INR10.1 trillion (US$120.5 billion), or 9.9% growth year on year, supported by rising financial literacy, broader digital distribution, and greater demand for tailored protection products.

The standalone health insurance market is forecast to grow at a faster pace, with GWP expected to rise from INR1.3 trillion (US$15.1 billion) in 2024 to INR2.0 trillion (US$23.8 billion) in 2028, a compound annual growth rate of 12.8%. Health insurance’s share of total Indian insurance premiums has increased from 6.9% in 2019 to 9.5% in 2023 and is projected to reach 11% by 2028. GlobalData anticipates health premiums will grow by about 15% in 2024, coinciding with regulatory adjustments, sustained medical inflation, and heightened awareness of healthcare financing needs.