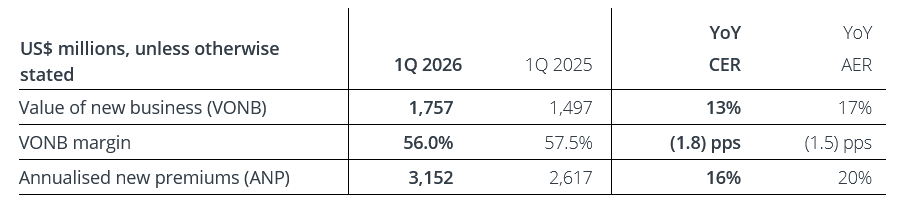

AIA Group Limited reported a 13% increase in value of new business (VONB) on a constant exchange rate basis for the first quarter of 2026 (Q1 2026), reflecting higher sales in most of its major Asian markets and across agency and partnership channels. For the three months ended March 31, 2026, VONB rose to US$1.76 billion from US$1.50 billion a year earlier. Excluding Thailand, where AIA reported an unusually high comparison base in the first quarter of 2025, VONB grew 22%. Annualised new premiums (ANP) increased 16% to US$3.15 billion, while the group VONB margin was 56.0%, compared with 57.5% in the prior-year period. On an actual exchange rate basis, VONB increased 17% year on year, and ANP rose 20%.

Group chief executive and president Lee Yuan Siong said the first-quarter outcome was consistent with the pattern seen last year and reflected contributions from multiple markets and channels. “AIA carried strong growth momentum from 2025 into the first quarter of 2026, delivering a 13% increase in group VONB, or 22% excluding Thailand which had an exceptionally high prior year base, as previously indicated. Our performance was broad-based with all reportable segments other than Thailand achieving year-on-year growth in VONB, demonstrating the breadth and diversity of our business model. Our two largest markets, Mainland China and Hong Kong, achieved excellent growth of more than 20% in the quarter,” he said.

Lee described the group’s strategy as focused on long-term demand for protection, health, savings, and retirement products in Asia. “As the leading pan-Asian life and health insurer, AIA is uniquely positioned to meet continuously rising consumer demand for protection, health, savings, and retirement products by leveraging the Group’s competitive advantages across brand, distribution, service, and technology. Our ability to consistently layer increasing amounts of high-quality, profitable new business with recurring earnings over many years drives higher earnings and cash generation for our shareholders,” he said.

In line with its capital management policy, AIA began a new US$1.7 billion share repurchase programme on March 30, 2026. As of April 29, the group had bought back 56.7 million ordinary shares, with total consideration of about HK$4.81 billion (approximately US$614 million) before expenses. Total weighted premium income for the quarter rose 13% to US$14.87 billion. On a present value of new business premium basis, the new business margin remained at 11%.

In Mainland China, AIA recorded 26% VONB growth, following the higher levels recorded in the second half of 2025. The result was attributed to its Premier Agency and selective bancassurance partnerships. The company reported increased demand for long-term savings solutions and a 17% rise in VONB from protection products in the period. Agent recruitment in China increased by more than 20%, and productivity improved among both new and existing agents compared with the first quarter of 2025.

AIA also reported VONB growth in geographies entered since 2019, which the group said is aligned with its 2030 targets for the market. In Hong Kong, VONB grew 21%, with contributions from both domestic customers and visitors from Mainland China. Agency and partnership channels both added to the result, supported by a product introduced in the second half of 2025. The independent financial adviser and broker segment reported higher VONB than a year earlier and an increase compared with the fourth quarter of 2025.

In Thailand, VONB declined 18% from the first quarter of 2025, reflecting the effect of the elevated base in that earlier period. Compared with the first quarter of 2024, first-quarter 2026 VONB was 39% higher. Traditional protection remained the largest product category. Increased sales of unit-linked products supported a 7% rise in ANP, and the VONB margin in Thailand stayed above 90%. Singapore recorded positive VONB growth against a high prior-year comparison, with contributions from both bancassurance and independent advisers and brokers, supported by demand from high-net-worth segments.

In Malaysia, AIA reported a high single-digit increase in VONB. Both agency and bancassurance channels contributed, with the agency channel posting quarter-on-quarter VONB growth alongside a higher number of active agents and increased productivity. Across AIA’s Other Markets segment, VONB was higher overall. Operations in Vietnam and the Philippines reported increased VONB, partly offset by lower contributions from Australia and Indonesia. Tata AIA Life, the group’s joint venture in India, continued to report VONB growth for the quarter.

Lee said the operating environment remains affected by geopolitical developments and market volatility, but that the underlying demand drivers for life and health insurance in Asia continue to support the business. “Despite current geopolitical tensions resulting in volatility in global capital markets, powerful structural tailwinds in the region, such as favourable demographics, rising incomes, low levels of private insurance penetration, and limited social welfare coverage, continue to create substantial demand for our insurance products. I have full confidence that the focused execution of our growth strategy and our substantial competitive advantages will continue to deliver long-term sustainable shareholder value,” he said. AIA said it receives most premiums in local currencies and generally matches assets and liabilities in the same currency to limit economic effects from exchange-rate movements. Because the group reports in US dollars, it presents growth figures on a constant exchange rate basis, which it said provides a clearer view of underlying performance.

AIA’s first-quarter update comes alongside disclosures from other insurers active in Asian life and health markets. FWD Group reported first-quarter 2026 new business sales of about US$720 million on an annualised premium equivalent basis, up around 4% year on year, and an 18% increase in new business contractual service margin to roughly US$556 million, pointing to faster growth in value than in volumes. Ping An Insurance (Group) Company of China reported a 45.5% rise in first-year life and health premiums to about RMB 66.3 billion and a 20.8% increase in new business value to around RMB 15.6 billion.

Prudential plc, which focuses on Asia and Africa, said new business profit rose 10% to approximately US$686 million, with APE new business sales up 6% to about US$1.82 billion and new business margin at 38%. In that context, AIA’s 13% VONB growth and 56.0% VONB margin place it alongside other regional and China-focused insurers that reported double-digit increases in value-based metrics – whether VONB, contractual service margin, new business value, or new business profit – against a backdrop of continued demand for life, health, and savings products across Asian markets.