India’s life and general insurers are preparing for a more moderate growth phase in FY27, as regulatory changes, digitalisation, and a shifting risk environment influence business strategies and earnings expectations.

Following a rebound in FY26, life insurers are projecting a slower expansion in the current planning cycle. Sector estimates indicate life premium growth in the range of 8% to 11% for FY27. This comes after new business premium increased 15.7% year on year in FY26 to ₹4.59 lakh crore, compared with 5.1% growth in FY25. Industry participants attribute the FY26 performance partly to base effects and regulatory moves, including the market’s adjustment to revised surrender value norms and the removal of GST on individual life policies, which affected pricing, distribution economics, and customer take‑up.

With those factors now embedded in portfolios, insurers are shifting attention to product mix, persistency metrics, and protection-oriented offerings rather than purely chasing top-line volume. “FY27 is likely to mark a transition towards more sustainable, quality-driven expansion. Protection and retirement planning will become central as India continues to face a large protection gap and rising life expectancy,” said Satishwar B, managing director and chief executive officer of Bandhan Life, as reported by The Telegraph.

Satishwar said technology is becoming more important across the life insurance value chain, from risk selection to policy servicing. He pointed to AI-enabled underwriting, digital onboarding, and quicker claims handling as areas where insurers are investing. “The move to allow 100% FDI is expected to attract long-term capital, accelerate technology adoption, and bring global best practices,” he said, while cautioning that insurers must still address challenges around customer trust, product suitability, and persistency.

From a credit perspective, ratings agencies see the sector as having largely absorbed recent regulatory adjustments. “The industry now appears to have largely adjusted to the revised surrender value framework, and growth is expected to be stable at 8% to 11% over the medium term, supported by product diversification, regulatory support, and continued expansion of digital distribution channels,” said Sanjay Agarwal, senior director, CareEdge Ratings.

In non-life, the general insurance industry recorded 9.3% growth in FY26, with gross direct premium written of ₹3.36 lakh crore. Companies and analysts anticipate similar high single‑digit growth at the industry level in FY27, but with tighter profitability as competitive and cost pressures build. “We expect a higher single-digit growth at the industry level,” Sanjeev Mantri, MD and CEO, ICICI Lombard General Insurance, told analysts at the company’s Q4 FY26 earnings call.

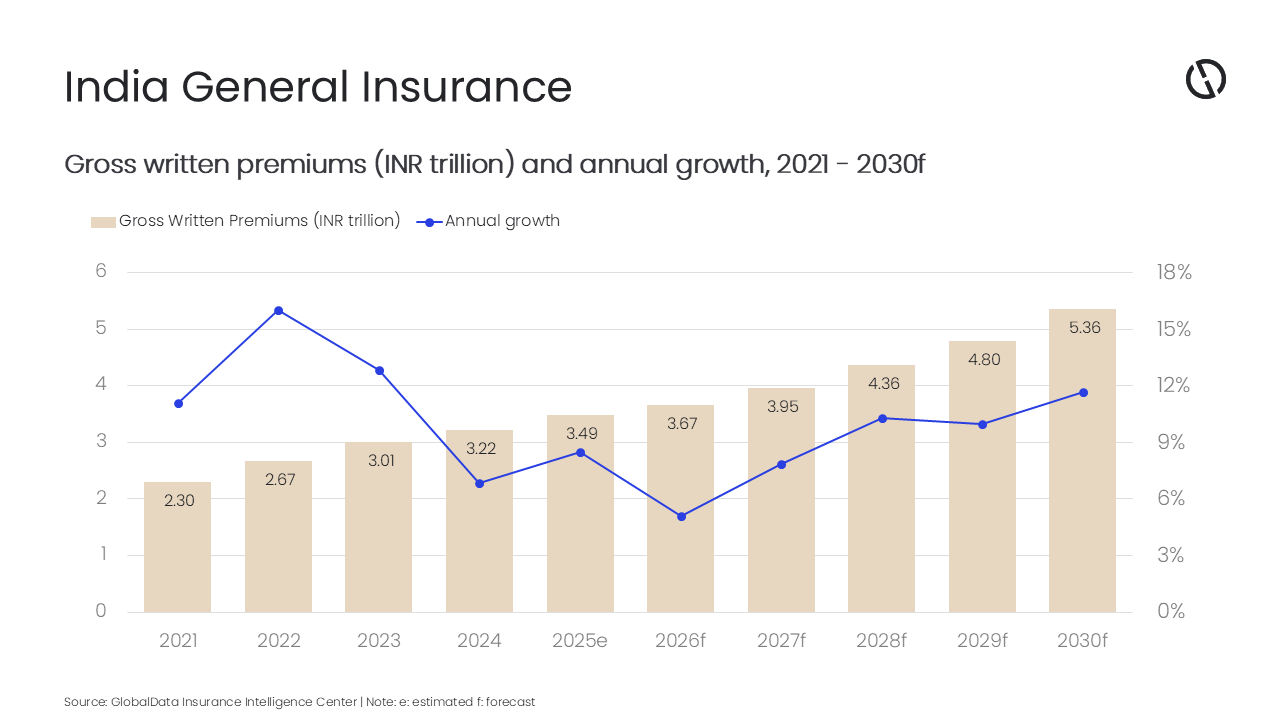

Over a longer horizon, external research indicates a larger expansion in general insurance premiums. Forecasts suggest gross written premium may rise from about ₹3.6 trillion (around US$43.4 billion) in 2026 to roughly ₹5.4 trillion (about US$62.2 billion) by 2030, implying compound annual growth of about 10%. Growth is expected to be about 8.5% in 2025 and then slow to around 5.1% in 2026 before picking up from 2027 as the effects of post‑GST adjustments and accounting changes ease.

Motor and health remain the dominant segments for general insurers. Together, they account for more than 70% of sector premiums; in 2025, personal accident and health (PA&H) business represented around 40.9% of general insurance premiums, up from 35.7% in 2021, and is projected to grow by 8.8% in 2026. Motor lines contributed 31.7% of general insurance GWP, supported by passenger vehicle sales and changing vehicle mix, including electric vehicles.

Regulatory measures and digital tools are influencing how insurers design products, manage claims, and structure distribution. “Digitalization of sales and claims processing, GST exemptions on key retail lines, and strong auto and health insurance demand have supported growth during 2021-25,” said Swarup Kumar Sahoo, senior insurance analyst at GlobalData. He added that growth during 2026-30 is expected to be driven by “stronger policyholder protection, faster claims settlement, and broader catastrophe-risk coverage.”

In health insurance, GST removal on retail health policies from September 2025 has reduced the tax component for policyholders and coincided with a pick-up in new and renewed covers. For the fourth quarter of 2025, standalone health insurance premiums rose 13.2% quarter on quarter. Insurers have introduced products with broader outpatient and wellness features, which they position as addressing out‑of‑pocket medical costs and enhancing coverage breadth.

However, an increase in policyholder grievances and recent regulatory penalties related to claims handling and governance lapses has kept supervisory focus on service standards. Regulators have emphasised policyholder protection, leading carriers to review disclosure practices, complaint resolution processes, and board‑level oversight. Motor insurance is also evolving. Higher electric vehicle penetration is influencing sums insured and repair dynamics, while usage-based and telematics-led policies are gaining ground. Digital brokers and aggregators are changing claims experiences by assigning dedicated claims managers, coordinating repairs with garages and surveyors, and using digital documentation to shorten processing times.

On the property side, infrastructure spending is a key driver. Property insurance accounted for 20.2% of general insurance GWP in 2025. Planned infrastructure investment of about $128.6 billion during 2026‑27, alongside housing and transport projects in Tier II and Tier III cities, is expected to increase demand for construction and property covers. Some state governments have also moved to formalise disaster risk transfer for vulnerable households. New disaster home insurance programmes combine parametric triggers with indemnity cover of up to ₹1 million for below‑poverty‑line families, with an objective of addressing climate-linked protection gaps and reducing reliance on ex‑post budgetary support.

Against this backdrop, insurers are operating in a more demanding risk and capital environment. Reinsurers have been revisiting catastrophe exposures, which is contributing to higher costs for reinsurance programmes. This is putting upward pressure on pricing in motor and property portfolios, particularly those exposed to natural catastrophe risk. “Competitive intensity in the general insurance space, particularly in corporate lines across domestic and international markets, increased, leading to softer pricing trends and some pressure on underwriting discipline. This environment could weigh on profitability, with the possibility of relatively weaker financial performance for (non-life) insurers from Q1FY27 onwards, especially if claims experience becomes less favourable,” said Priyesh Ruparelia, director, CareEdge Ratings, as reported by The Telegraph. Ruparelia also pointed to geopolitical developments, noting that tensions in West Asia are affecting marine, aviation, and transit (MAT) covers and construction costs. He said these tensions “remain a key overhang, with the potential to disrupt marine trade, elevate risk exposures and trigger repricing across segments, possibly leading to a broader recalibration of underwriting and risk management practices.”

Sahoo, from GlobalData, outlined a mix of regulatory and market responses: “India’s general insurance industry is expected to grow on the back of strengthening policyholder protection, product innovation in motor and health, the expansion of parametric and disaster pools to manage climate risk, and a step-up in digital claims and distribution. Reforms such as tax exemption, GST reliefs, and stronger grievance redressal – paired with robust digital platforms and disciplined natural catastrophe (Nat-Cat) pricing – position the market for sustained premium growth. However, insurers need to remain watchful about the impact of the West Asia crisis, which has already increased risk premiums for marine, aviation, and transit (MAT) business and construction costs in the country, with an expected wider impact on the economy.”