Best Insurance Companies in Australia |

Brokers on Insurers

Jump to winners | Jump to methodology

Insurers show true grit

Speed, service and consistency stand out as the defining broker priorities in 2025, reshaping how the best insurance companies in Australia have climbed to the top of industry rankings.

In IB’s annual Brokers on Insurers survey, brokers across the country shared their invaluable insights and rated the performance of 10 insurers they had worked with over the past 12 months.

Insurers were evaluated across 11 key metrics, including turnaround times on new business and claims, overall service level and premium stability. They were then ranked based on average scores from broker ratings.

The top three performers in each category received gold, silver or bronze medals, while Insurer of the Year medals were awarded based on combined average scores across all categories.

The insurers setting the benchmark for excellence in Australia have earned a vote of confidence from brokers and a competitive edge by delivering what the third-party channel says matters most:

-

“Underwriters that want to work with us, help us and actually try to get something over the line”

-

“Better management of claims, fast response time and granting indemnity quickly”

Liberty Specialty Markets Australia – Insurer of the Year

Being rewarded with a silver medal is a vote of confidence as a result of a deliberate long-term strategy.

Liberty Specialty Markets also earned gold in BDM support, turnaround times for new business and claims and silver in brand recognition and reputation and broker communication, training and development.

Liberty Australia president John McCabe explains that the leading insurer continues to focus on stability as markets shift and capacity returns to some of the more complex commercial insurance portfolios.

“Many of our portfolios are long tail, so when you choose an insurer, you have to consider their value proposition as a multi-year commitment,” he says. “Choosing an insurer you know will be around to pay claims and manage that process locally is important.”

John McCabeLiberty Specialty Markets Australia

The top insurer, which earned gold for product innovation, silver for commission structure, bronze in overall service level and sixth place overall, believes keeping ahead of client and broker needs is paramount.

Over the past year, AXA XL has made significant strides in evolving its service model to enhance consistency in client service. Informed by feedback from brokers and clients, it recently launched a new client management framework tailored to their needs.

“This initiative has led to the implementation of standardised procedures and a substantial investment in training our teams, ensuring a unified approach to service delivery,” says Stephen Nguyen, head of distribution, marketing and communications, for Australia.

Stephen NguyenAXA XL

The key to this evolution was a dedicated client service team comprised of client managers, underwriters, claims specialists and risk engineers. This cross-functional collaboration fosters communication among its commercial teams, enabling them to provide timely responses and a cohesive customer experience.

“As a result of these enhancements, we have observed a notable increase in our Net Promoter Score from our broking partners,” Nguyen adds. “Our commitment to continuous improvement and client-centric service remains a top priority for the team.”

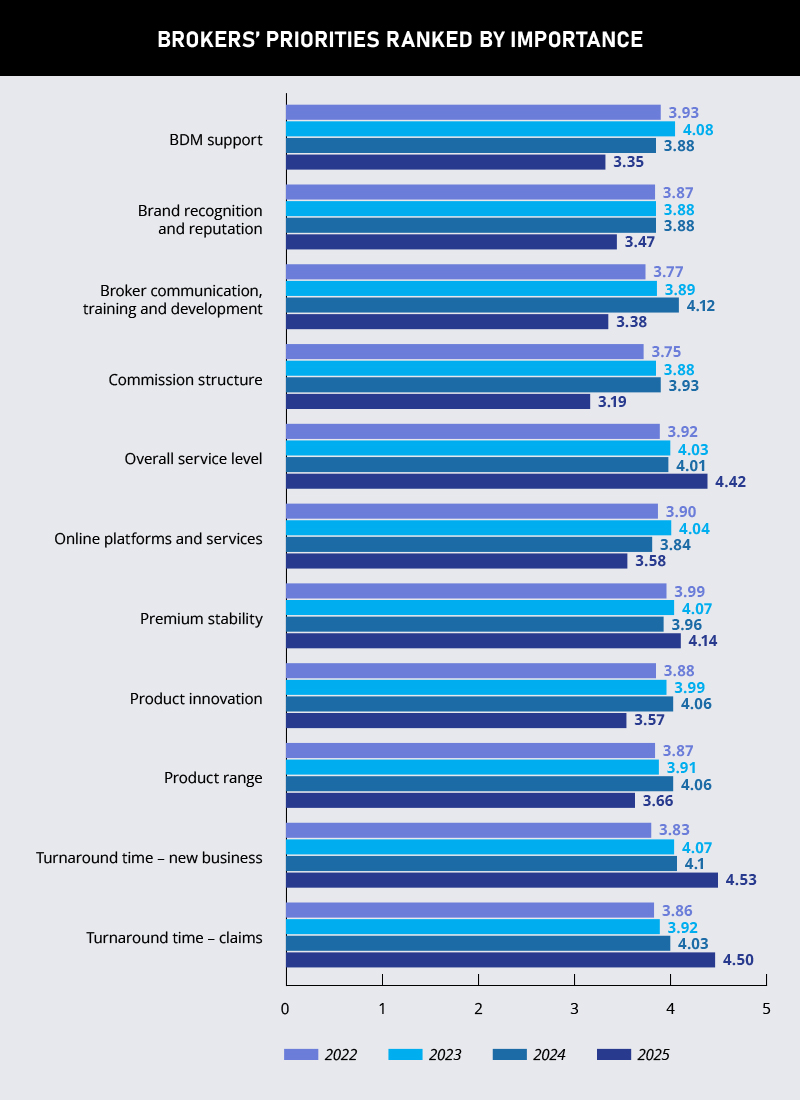

How broker priorities have shifted: a four-year trend

An analysis of IB’s survey data from 2022 to 2025 shows the most significant shift in broker sentiment is a move towards choosing insurers who deliver quickly, support brokers effectively and perform reliably over time.

Key takeaways:

-

refocus on speed and execution

-

shift from training to turnaround

-

decline in prioritising innovation

-

increased emphasis on stability

O

O

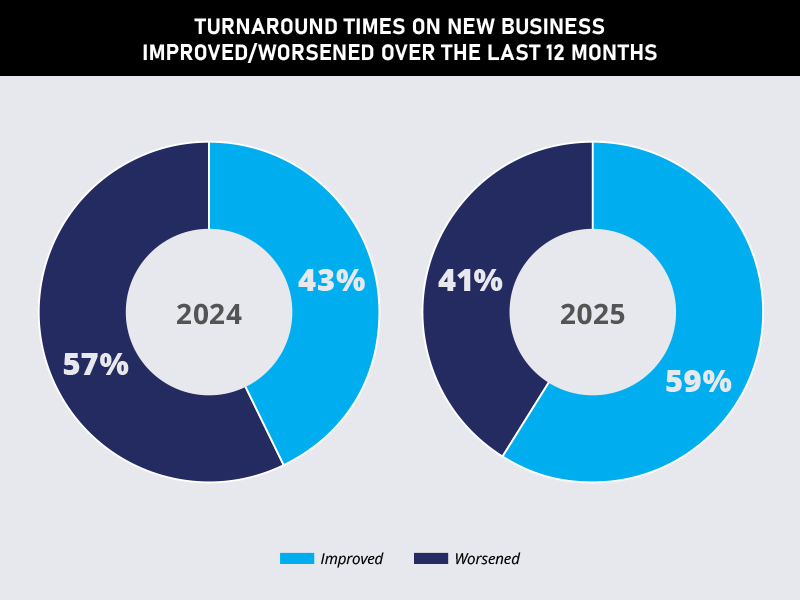

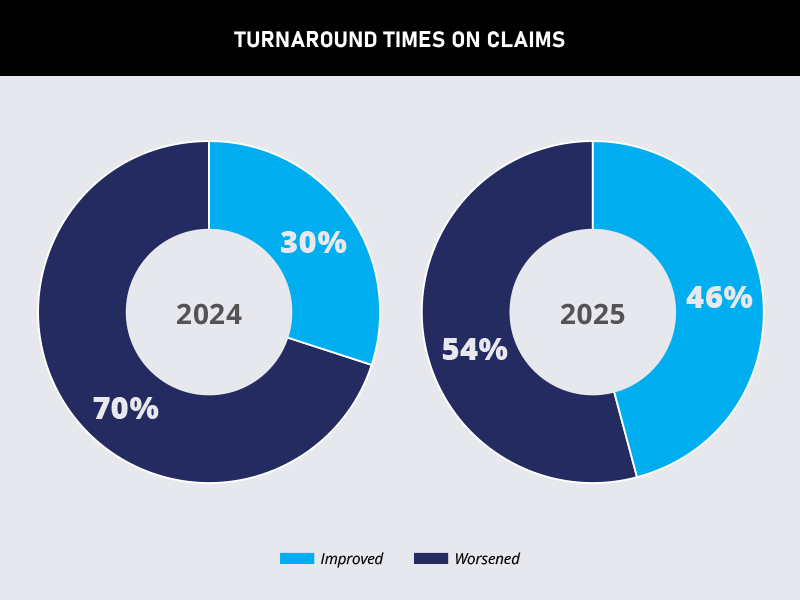

In 2025, turnaround time for new business and claims holds the top two spots in broker rankings, rising from second and fifth place in 2024 and from fourth and seventh in 2022, respectively.

This shift signals a change in how brokers prioritise insurer relationships.

The average score for new business turnaround surged from 3.83 in 2022 to 4.53 in 2025, making it the single most important factor this year. Claims turnaround followed closely, rising from 3.86 to 4.50 over the same period.

These jumps indicate growing pressure on brokers to move faster for their clients, coupled with diminishing tolerance for delays, and were echoed in this year’s broker comments:

-

“Slow response times and difficult risk requirements, particularly with property and the number of surveys every year”

-

“Trying to contact underwriters and get responses – service levels are at the worst I’ve seen in over 40 years”

Meanwhile, overall service level has climbed steadily from 3.92 in 2022 to 4.42 in 2025, confirming that consistent, accessible and competent service remains a mainstay of broker satisfaction, especially when paired with speed.

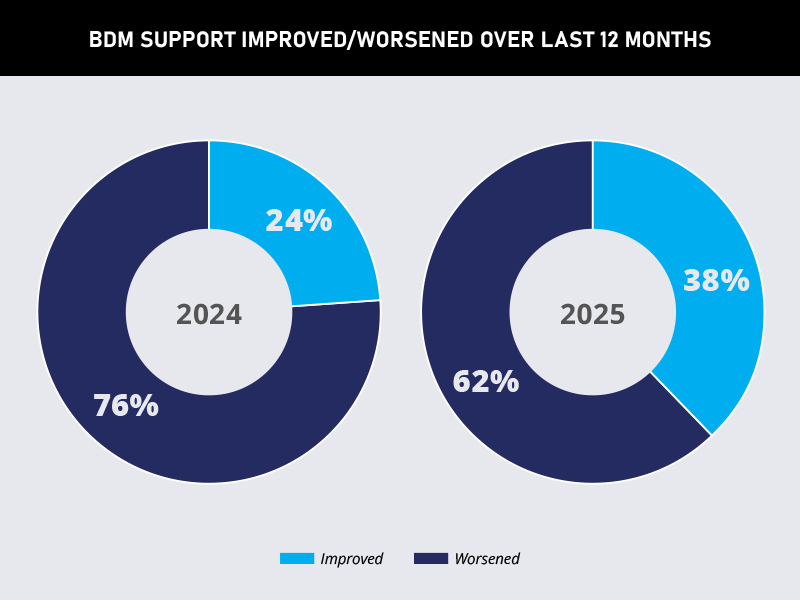

By contrast, broker communication, training and development, which ranked first in 2024, dropped sharply to ninth in 2025. Its score fell from 4.12 to 3.38. BDM support and commission structure also saw significant declines.

This suggests that while personal relationships remain important, brokers are placing greater emphasis on insurer responsiveness, operational efficiency and consistent execution, factors that directly impact client outcomes.

Even previously high-profile categories such as product innovation and online platforms have lost ground.

Innovation dropped from 4.06 in 2024 to 3.57 in 2025, while platform ratings slipped from 3.84 to 3.58. Brokers have sent a strong message that new features and tech tools are only valued if they enable faster, smoother workflows.

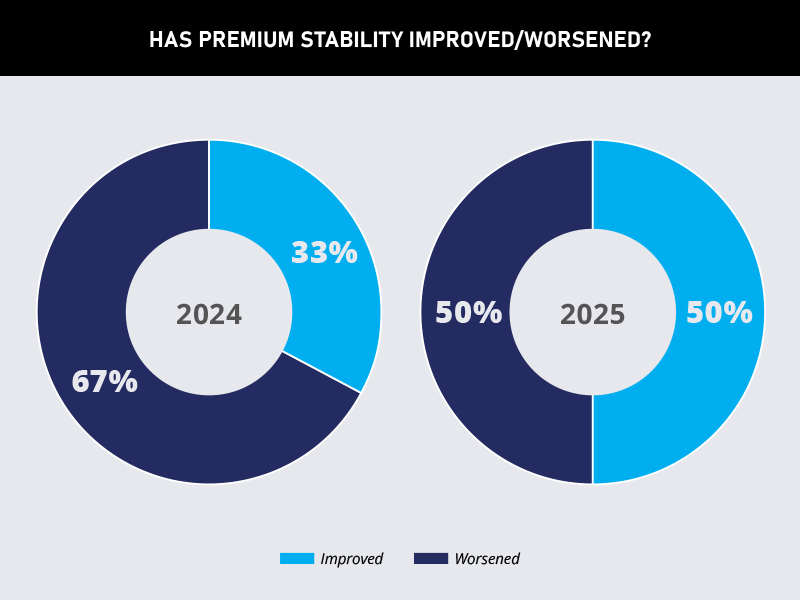

One factor that has bumped back into focus is premium stability, which now sits in fourth place with a rating of 4.14. While it lacks the urgency of turnaround time, brokers place greater weight on predictable pricing in a climate of fluctuating rates and client expectations.

What sets the top-performing insurers apart in 2025 is their ability to deliver speed and service consistently, instilling brokers with confidence to meet client expectations.

What brokers say about frustrations and expectations

IB’s data shows the biggest shifts in broker priorities stem from the pressure to work faster, deliver more certainty, and get expert answers quickly. Comments from survey respondents reveal ongoing frustration with service levels, pricing and insurer responsiveness.

Service standards have deteriorated

Many brokers say communication has worsened significantly, citing inconsistent staffing, slow responses and a lack of ownership.

-

“Lack of or incomplete responses”

-

“Not being able to deal with the decision-maker”

Some brokers tied these issues to post-pandemic operational changes, particularly remote work arrangements.

-

“If staff are going to work from home, there still needs to be consistency with their service delivery, which does not happen now, and it has been getting worse”

Underwriting too rigid and reliant on AI

Brokers are pushing back against black-and-white underwriting rules and the growing role of automation in decision-making.

-

“Bring back underwriting and replace AI on more complex risks. One size does not fit all”

-

“We need more available markets; at times, it appears like insurers and agencies don’t even assess the risk before underwriting”

Pricing is unpredictable and poorly explained

While premium stability has improved, many brokers remain frustrated by unclear risk pricing and lack of justification.

-

“Erratic pricing. There is no proper grasp of the risks they are insuring. Poor communication”

What brokers want in the year ahead

While frustrations remain high, brokers are clear-eyed about the fixes. They want insurers to:

-

rebuild service standards through faster, more reliable communication

-

reinvest in human expertise, especially in underwriting and claims

-

deliver pricing stability and better risk transparency

-

improve decision-making at the front line, not defer to external parties or automation

Respondents offered innovative suggestions on how to move past these issues:

-

“Insurers need to understand that not all quotes can be done through a portal; a human needs to manually review a submission, as not everyone fits into a box”

-

“Revisit claims structures; staff should have more authority instead of continually deferring to outside contractors”

How the top insurers are responding

Fast turnaround times become essential

Turnaround times for new business and claims ranked as brokers’ No. 1 and No. 2 priorities in 2025.

According to IB’s data, 59% of brokers said turnaround time for new business improved in the past 12 months, a 16% increase over 2024. Claims efficiency also improved, with 46% of brokers reporting better performance, up from just 30% the year before.

This reflects real improvement from insurers who have listened to broker concerns and restructured processes to deliver faster.

-

“Faster responses for claims, as this is what the client pays their premiums for”

-

“Insurers need to look at getting staff, particularly claims staff, as natural disasters are going to increase”

One of the standout performers in this year’s survey, Liberty attributes its consistency and speed to empowered teams and local decision-making.

“We rarely have to refer or seek approval offshore,” says McCabe. “Our underwriters have clear appetites and capacity and try to make it a quick ‘no’ where we can’t help.”

That autonomy extends to its claims specialists, who are spread across four states to ensure most claims are handled locally.

“Most product lines see one person manage a claim from start to finish, meaning that we understand the business needs of our brokers and customers,” McCabe notes. “We know that brokers and clients like dealing with people rather than generic mailboxes, and our teams are highly skilled and technically very strong in their product knowledge.”

AXA XL’s Nguyen highlights that the insurance sector is in flux due to technological advancements, evolving customer expectations and the emergence of new risks.

“The risks are larger, more complex and arriving rapidly,” he says. “To proactively address the needs of brokers and clients, our team embraces a collaborative and agile approach to product innovation. We prioritise active engagement with brokers and clients, gathering insights and feedback for our product development process. This ensures that our offerings remain aligned with our clients’ requirements.”

For example, the company has made significant investments in cyber insurance, an area in which it is considered a market leader. Its approach includes providing bespoke coverage options and a suite of pre-loss services designed to mitigate risks. This is complemented by dedicated cyber claims support and specialised risk engineering to assist clients effectively during incidents.

Additionally, it has established a dedicated energy transition practice group that brings together its extensive expertise to support clients navigating new and emerging technologies, such as renewable energy solutions and sustainable practices.

“By leveraging our knowledge and resources, we aim to empower clients to transition to a more sustainable future,” adds Nguyen.

Service and support are better but remain inconsistent

Many brokers still describe support as under pressure, particularly around communication, follow-up, and accessibility. While 38% noted an improvement in BDM support, a majority, or 62%, still reported it had worsened.

-

“More insurers should be focused on service to brokers”

-

“We need more BDM meetings; some insurers seem to change our BDMs every few months”

Despite not having a traditional BDM model, Liberty excelled in this category by focusing on accessibility and product knowledge.

“We don’t have BDMs, but we make our underwriters, claims team and risk engineers highly accessible, and they are all very knowledgeable,” says McCabe. “We also have state managers and key relationship leaders who help us coordinate across our products and effectively meet client needs.”

AXA XL acknowledges that feedback from brokers and clients is vital in shaping its operations and market strategy.

“We have established regular feedback loops that include broker surveys and forums designed for our customers to share their insights,” says Nguyen. “These initiatives give our clients direct access to our leadership teams, ensuring their voices are heard and valued in our decision-making processes.”

That feedback is shared widely across the company, enabling the team to celebrate their achievements while identifying and addressing areas for improvement.

Claims handling a work in progress

While brokers reported improved turnaround times for claims in 2025, many say the experience still falls short, particularly regarding decision-making authority, staff expertise and reliance on third-party contractors.

According to IB’s data, claims efficiency has improved modestly, with 46% of brokers saying it got better this year. That’s a 16% increase in positive sentiment from 2024.

However, 54% still said claims handling had worsened, making it a persistent sore spot in broker-insurer relationships.

While the overall pace of claims has increased, brokers say quality, consistency, and communication still aren’t where they need to be.

-

“More training for claim handlers”

Brokers want claims handled competently and confidently by people who understand the product and have the authority to act.

This year’s top-performing insurers have responded by investing in claims teams, improving internal workflows, and reducing reliance on external adjusters, particularly for high-volume or time-sensitive claims.

Pricing stability and transparency

Half of brokers said premium stability improved in 2025, up from just 32.84% the year before, but the other half still sees volatility.

-

“Flattening of premiums would be nice, as clients can’t take much more”

-

“If they’re going to charge $8,000, they should provide third-party data to support

Liberty stayed the course in a challenging year marked by pricing pressures, staffing strain and claims complexity.

“Above all, we strive for consistency; we don’t dip in and out of market segments, so our broker partners become very familiar with our appetite,” McCabe says. “Being a mutual helps us do this, as we aren’t subject to the constant growth pressures that many large public Australian insurers face.”

Training and expertise are differentiators

Brokers increasingly point to a gap in technical skills and underwriting knowledge. They want insurers to bring in more training, knowledgeable staff, and less reliance on automated decisions.

-

“More resources, more training and move away from reliance on AI, which is advancing incompetency”

-

“Upskill on technical matters as there is a dearth of technical knowledge in the industry”

The top-performing insurers stand out by investing in their teams and empowering staff to make better, faster, and more accurate decisions.

Liberty earned second place for broker communication, training, and development, even as many insurers saw their scores slide. McCabe says the key is focusing on practical, broker-led content.

“We run many technical workshops and webinars and share thought leadership articles with brokers throughout the year. We know that brokers particularly like hearing about our claims examples and policy coverage enhancements,” he notes. “We’re constantly working to leverage technology in how we approach this communication to make it as easy and engaging as possible.”

He points to Liberty’s new environmental insurance digital experience as an example, which consolidated content from eight PDF documents into one user-friendly, web-based format.

Best Insurance Companies in Australia |

Brokers on Insurers

Insurer of the Year

- Vero

Gold - Liberty Specialty Markets Australia

Silver - Allianz

Bronze

BDM support

- Liberty Specialty Markets Australia

Gold - Vero

Silver - Berkshire Hathaway

Bronze

Brand recognition and reputation

- Berkshire Hathaway

Gold - Liberty Specialty Markets Australia

Silver - Allianz

Bronze

Broker communication, training and development

- Vero

Gold - Liberty Specialty Markets Australia

Silver - Allianz

Bronze

Online platforms and services

- Vero

Gold - Allianz

Silver - CGU

Bronze

Product range

- Vero

Gold - Allianz

Silver - QBE

Bronze

Turnaround time – claims

- Liberty Specialty Markets Australia

Gold - Vero

Silver - Chubb

Bronze

Turnaround time – new business

- Liberty Specialty Markets Australia

Gold - Berkley Insurance Australia

Silver - Berkshire Hathaway

Bronze

Overall

- Vero

Gold - Liberty Specialty Markets Australia

Silver - Allianz

Bronze

Methodology

Brokers from across the nation were invited to rate the performance of a selection of insurers currently operating in Australia. To ensure the results were relevant and timely, respondents were asked to rate only those insurers they had dealt with in the past 12 months.

Ten insurers were rated by brokers in this year’s survey: Allianz, AXA XL, Berkley Insurance Australia, Berkshire Hathaway, CGU, Chubb, Liberty Specialty Markets, QBE, Vero and Zurich. The brokers rated each insurer’s performance on a scale of 1 (very poor) to 5 (very good) across 11 different categories.

For each category, the insurers were ranked in order of merit according to an average score calculated from a tally of their ratings. The top three companies in every category received a gold, silver or bronze medal. The insurers’ combined average score from all categories determined the medalists for Insurer of the Year.

Keep up with the latest news and events

Join our mailing list, it’s free!