Best Insurance Companies in Australia |

Brokers on Insurers

Jump to winners | Jump to methodology

Brokers crown the best insurance companies in Australia

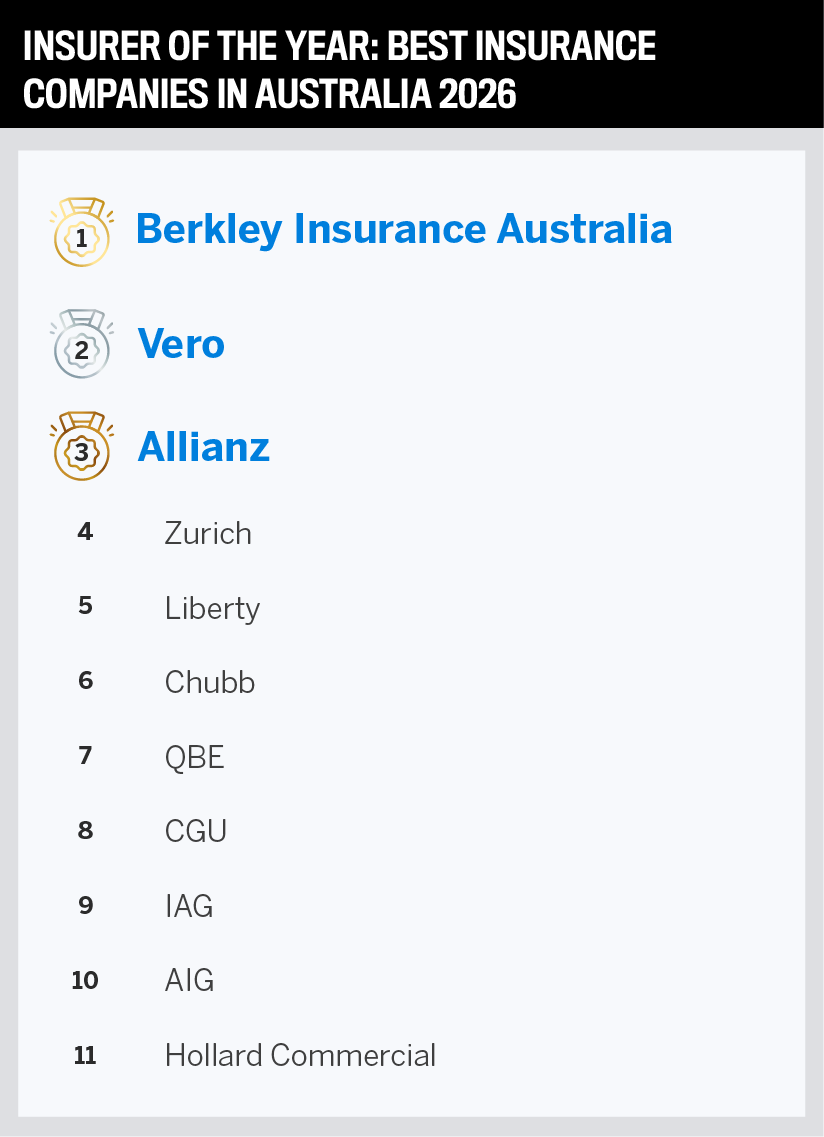

Berkley Insurance Australia edges out Vero and Allianz and closes a three-way finish, all earning their places among the best insurance companies in Australia

Introduction

Brokers across Australia have once again delivered their verdict on the best insurance companies in Australia – and this year, it belongs to Berkley Insurance Australia. In the 2026 Insurance Business Brokers on Insurers, Berkley claimed the coveted Insurer of the Year title. narrowly edging out Vero and Allianz in a close three-way finish.

The result caps a standout year for the specialist commercial insurer, which collected gold medals in four individual categories: broker communication, training and development; overall service level; premium stability; and turnaround time – new business – more gold finishes than any other insurer in the 2026 survey.

Eleven insurers were assessed across 11 performance categories – from BDM support and premium stability to product innovation and turnaround times – with each rated by brokers who had dealt with the insurer in the preceding 12 months, on a scale of 1 (very poor) to 5 (very good).

Perhaps the most striking performance away from the overall podium came from Liberty, which claimed gold in both product innovation and turnaround time – claims. Despite a more specialised market footprint, Liberty’s scores in those two categories were the highest recorded across the entire field, signalling growing broker confidence in its claims handling capability and capacity for new product thinking.

Vero, always a top perfomer, secured gold for BDM support and the silver medal for Insurer of the Year with a total of nine top three finishes across the 11 categories. Allianz rounded out the top three, claiming gold in both brand recognition and reputation and online platforms and services, reflecting continued investment in its broker-facing digital infrastructure. Zurich delivered a composed midfield showing, claiming gold in commission structure and silver for BDM support.

The state of play: Australian insurance 2025–26

Understanding what separates the best insurance companies in Australia from their peers requires understanding the market they operate in. The Australian general insurance sector enters 2026 in a state of transition. After several years of hard market conditions – characterised by steep premium increases, tightening capacity and heightened reinsurance costs – the market has shifted into a softer phase. Premiums are easing across most commercial lines, insurer appetite has broadened, and competition for quality risks has intensified. For brokers, the change represents an opportunity. For insurers, it represents a test of discipline.

The numbers tell a story of solid but softening profitability. According to KPMG’s General Insurance Insights & Analysis 2026, which draws on APRA data to 31 December 2025, the Australian general insurance industry recorded a net profit of $5.2 billion for 2025 – down from $6.1 billion in 2024. The decline was driven primarily by a sharply elevated natural hazard year: total catastrophe and significant event losses reached $4.46 billion in 2025, compared with just $566 million in 2024. Three catastrophes and three significant events generated a claims count six times higher than the prior year, with Ex-Tropical Cyclone Alfred alone contributing over $1.5 billion in insured losses across Queensland and northern New South Wales.

Compounding the hazard picture, many of the year’s catastrophe events fell below the activation thresholds of the reinsurance protections that insurers had purchased – meaning losses were absorbed on the balance sheet rather than recovered. Capital coverage for direct insurers fell slightly to 1.75 times APRA’s prescribed capital amount by December 2025, compared with 1.82 times the year prior, according to KPMG. Industry insurance revenue reached $20.1 billion in the September 2025 quarter, per APRA data, broadly tracking upward – but the tailwinds from investment markets that turbocharged 2024 profits have moderated.

The market is valued at approximately AUD $114.56 billion in 2025 and is projected to grow at a compound annual rate of 1.80% to reach AUD $136.93 billion by 2035, according to Expert Market Research. Within general insurance, gross written premiums reached $68 billion in 2024, per APRA and KPMG, with GlobalData forecasting direct written premiums of $146.9 billion by 2029. Brokers remain the dominant distribution channel: APRA’s intermediated statistics for the six months to June 2025 show 50% of GWP – $17.6 billion – placed with APRA-authorised insurers – flowing through intermediaries, with 1,740 active in the market.

The soft market now taking hold brings its own pressures. Australia’s commercial insurance market remained in soft territory through the first half of 2026, with pricing easing across property, financial lines, liability and cyber insurance, according to EBM Insurance & Risk’s Insurance Market Trends and Outlook – May 2026 report. Property rate reductions of approximately 10–20% were recorded across the Pacific region during the third quarter of 2025, according to Lion Partnership, while casualty pricing declined by around 7% and cyber insurance premiums fell by approximately 10% through the year.

But softening markets reward the disciplined and expose the careless. EBM’s report identified ongoing geopolitical tensions, energy price volatility, climate-related losses and persistent inflationary pressure as factors that continue to shape insurer sentiment – and could accelerate a market turn if conditions worsen. Agriculture and clients with material loss experience remain among the more challenging sectors. Chambers and Partners’ Insurance & Reinsurance 2026 guide for Australia describes the current environment as “the bedding down of another soft market, with increased competition and capacity forcing downward pressure on rates.”

Against that backdrop, the challenges facing insurers heading into 2026 have sharpened. Gallagher Bassett’s Carrier Perspective: 2026 Claims Insights identifies premium affordability and insurability as the top industry concern for 2026 – a remarkable jump from sixth place in 2025. The shift is attributed to rising inflation, increased climate-related losses and intensifying regulatory pressure. Cyber and data security risks retain their position as the second most pressing challenge for the second consecutive year.

Workforce challenges have risen sharply, moving from seventh to third on the list of insurer concerns between 2025 and 2026. Skills shortages and changing workforce expectations – particularly as the industry accelerates its digital transformation – are creating competitive pressure at the talent level. KPMG notes that 83% of global insurance CEOs now identify cybercrime as a top concern, while the pace of regulatory change remains elevated: APRA’s Prudential Standard CPS 230 on Operational Risk Management and the Financial Accountability Regime are reshaping governance and accountability expectations across the sector.

It is within this context – softening premiums, elevated natural hazard risk, digital disruption, regulatory reform and intensifying competition – that this year’s IB Brokers on Insurers takes on particular significance. When brokers vote, they are not simply awarding points for good customer service. They are signalling which insurers have built models capable of delivering consistent value across market cycles. The results that follow reflect those judgements.

What brokers value most: criteria importance 2023–26

Each year, brokers are asked to rank the importance of 11 criteria when choosing and working with an insurer on a scale of 1 to 5. The results over the past four years reveal how broker priorities have shifted – and which attributes have consistently mattered most.

In 2026, turnaround times dominate the top two positions in the survey’s four-year history, with claims turnaround (4.49) and new business turnaround (4.45) edging ahead of overall service level (4.44) for the first time in the available data. Premium stability holds firm in fourth. Meanwhile, commission structure remains the lowest-ranked criterion for the third consecutive year, reflecting brokers’ views that service and reliability outweigh price incentives when evaluating insurer partners.

Broker sentiment: in their own words

Beyond scores and medal tallies, the IB survey asked brokers a direct question across four critical service areas: has performance improved or worsened over the past 12 months? Their answers – and the comments behind them – reveal a market in which progress is real but uneven and where the gap between the best and the rest remains wide.

Firm profile

Berkley Insurance Australia’s 2026 wins did not arrive by accident. The specialist commercial insurer has spent more than 15 years building a model defined by proximity to brokers, disciplined underwriting and a single-minded focus on service delivery. Brokers rated it highest overall and across four of the survey’s 11 categories – a result the business describes as validation of a strategy that has been consistent since inception.

At the heart of Berkley’s approach is what it calls a single point of entry system: a platform built entirely in-house that allows brokers to quote, bind and receive accurate policy documents without switching between systems or waiting on manual processes. The technology, branded BindIT, has been extended substantially in recent months – adding multi-product quick-quote functionality, self-service claims, a glass extension to general liability policies, and an increase in maximum premium thresholds. Crucially, Berkley is clear that the technology is supplementary, not a replacement for relationships.

Premium stability is another pillar of the Berkley proposition. While acknowledging it is subject to the same market forces as its peers, the business maintains that granular, multi-year pricing data allows it to manage premium volatility more effectively than most, avoiding the sharp increases that have frustrated brokers and clients alike during hard market cycles.

On broker communication, Berkley’s webinar programme has become one of the more significant broker-engagement touchpoints in the Australian market. With an average of 1,800 sign-ups per session and a feedback loop built into every event, the business has structured its communication as a genuinely two-way exercise. Many of its senior team and underwriters have worked as brokers themselves – an intentional hiring philosophy that shapes how the business thinks about broker pain points.

The firm’s turnaround time on new business reflects an internal philosophy of same-day or within-24-hour responses. The business does not, by its own account, spend significant time measuring and analysing turnaround statistics – it relies on broker feedback to confirm performance. That feedback, it says, consistently affirms it is getting the balance right.

Q&A: Berkley Insurance Australia

Brokers rated you highly on service levels and premium stability. What do you do operationally to deliver in these areas?

“From inception, our full focus has been on providing a level of service that meets or exceeds broker expectations. By ‘service’ we don’t just talk about response times – it involves being available, answering the phone, calling brokers back and ensuring that underwriting decision-makers are as close to their brokers as possible. Our whole underwriting process has been built around this concept from the ground up. Premium stability is something we are proud of. We have many years of granular data that allows us to understand the variable components of pricing and how that flows through to our premiums. During both hard and soft markets, we are generally able to mitigate the need for significant premium variation.”

Broker communication, training and development was another highlight. What do you focus on and why?

“We have spent a significant amount of time gaining feedback from brokers on what they want to know from us. Part of our service culture is to listen and then respond with something meaningful. On average, we have around 1,800 people sign up for our webinars, and the response is always very positive. We have a multi-layer communication strategy – expert articles, webinars, newsletters, regional functions, and individual broker visits – all coming together with common messaging and a service focus. Communication, after all, is a two-way street.”

Tell us about BindIT – the mindset behind it and how it was built.

“BindIT was developed with brokers in mind as the demand for self-service portals increased. Our underlying philosophy is that brokers can deal with us in whichever way they choose – via BindIT, our SCTP or our state-based teams – and have the same underwriter servicing the business across all three. We built the technology ourselves, which allows us to make changes quickly and easily. In recent months alone, we have added self-service claims, multi-product quick quotes, individual broker dedicated programs, a Glass extension to our general liability policy and an expansion of PI professions. We cannot emphasise enough how important choice is.”

What is the most innovative product update you’ve made in the last 12 months?

“Two things stand out. First, the multi-product quick quote in BindIT – in practice, if you put information into the system for a PI quote, it will also provide an indication for general liability and management liability, giving three indications at once. The other is simpler but came directly from listening to brokers: we have added Glass cover to our general liability policy. We were surprised by how many brokers go through the complicated process of taking out a bus-pack policy and only using two sections. It is not going to change the world, but we hope it makes life easier.”

Overall, you were voted gold by brokers. What does that mean to the team?

“It provides enormous validation for the team that the hard work and focus they dedicate to providing the best service they can to brokers are appreciated. Appreciation is not always expressed on a day-to-day basis, so to receive recognition directly from brokers reinforces that the effort is worthwhile. From a corporate perspective, we could not be more proud of the way our teams have been delivering for brokers over a long period of time.”

Firm profile

Liberty

Gold: Product innovation and turnaround time – claims • Silver: Premium stability and turnaround time – new business

John McCabe, currently the firm’s president, has been at Liberty for nearly 27 years – longer than many of the businesses it insures have existed. That longevity is, in many ways, the story of Liberty in Australia: consistent, disciplined, and deliberately built around relationships that compound over time. In this year’s survey, brokers rewarded that approach with gold in two of the most operationally demanding categories: product innovation and turnaround time – claims.

Liberty’s mutual structure sits at the centre of how it explains itself to brokers. As part of the Liberty Mutual group – which operates as a mutual holding company – the business generates its own capital through profitable underwriting rather than raising it from public equity markets – a constraint that, paradoxically, enforces the long-term thinking that brokers say they value. The business does not need to grow at any cost. It grew threefold during COVID-19, McCabe says, not because of a growth mandate, but because it was operationally ready when many peers were not.

On claims, Liberty’s approach is notable for its philosophical simplicity: pay valid claims fast, and even borderline ones, too. McCabe’s description of the business’s claims culture – “If it’s a bit grey, we say that’s good enough, we’ll pay that as well” – reflects Liberty’s freedom from public shareholder pressure to minimise payouts, allowing it to reserve conservatively and settle quickly. Full reserves are set on day one, rather than stepped up over time.

On turnaround for new business, Liberty’s philosophy is equally direct: if the answer is “no,” say so immediately. For more homogeneous lines like corporate travel and accident health, the system is structured to surface a non-appetite determination at the point of data entry, so brokers can move to other markets without delay. For more complex risks, the business brings together underwriters across lines in broker office visits – a Lloyd’s box-style approach that shortens decision cycles and deepens relationships simultaneously.

Premium stability at Liberty flows from the same long-term discipline. Rather than tracking market cycles with sharp price movements in either direction, the business aims for consistency – never the cheapest, never the most expensive. McCabe notes that clients who paid $100,000 in a stable year and suddenly face demands for $500,000 cannot plan their businesses. Liberty’s 90-plus percent policy retention rate at the end of 2025 is, in part, a product of that philosophy.

On innovation, Liberty is building products specifically for industries being reshaped by AI – notably life sciences and drug manufacturing. At the same time, AI is being deployed internally to accelerate the analysis of complex risk engineering reports, freeing underwriters to spend more time in the market. The business is clear that this is AI as a productivity tool, not a replacement for the relationship-based model that brokers say they value.

Q&A: John McCabe, Liberty

How important is broker feedback to how you run the business?

“After 37 years of marriage, I’ve learned there’s always a better way to do something. We actively commission broker feedback – scores and written responses – and it is genuinely important that we listen. Brokers, particularly younger ones who have only operated in a hard market, are navigating significant change right now. Our job is to understand what they are dealing with and help them present solutions that are tailored to what clients really need, rather than just competing on the lowest price.”

You won gold in both turnaround time categories. What drives your performance there?

“The culture of our business has always been built around doing the right thing, whether anyone is looking or not. For claims, that means when the situation arises, people need to know the money is coming as quickly as possible – even if the position is a little grey. For new business, our philosophy is that a quick ‘no’ is better than a delayed ‘no.’ Nothing frustrates broking partners more than waiting around for an answer. If a risk doesn’t meet our appetite, we tell the broker the same day so they can move to other markets immediately.”

Your mutual structure seems central to how you explain Liberty. How does it translate to broker and client outcomes?

“As a mutual, the only way we can grow is to be profitable – we cannot raise capital externally. That drives consistent practice over time. We do not always have to grow. If the market is not in our favour, it is okay not to grow – we want to hold on to the business we like to write. When it comes to claims reserves, our attitude has always been to estimate the final cost on day one and put the full amount up immediately, rather than stepping up reserves over time. That means everyone knows we are not trying to squeeze a dollar out of a claim.”

How do you approach AI and technology while maintaining the human relationships brokers value?

“Insurance is truly a relationship business – the relationship with the broker and the relationship with the client. AI helps us free up our people’s time so that they can do that, rather than replacing them. We are using it to summarise complex risk engineering reports that might run to 600 pages, so our underwriters can spend that time out in the market. We are also using it to scan emerging industry segments – like life sciences – to build products specifically for those risks. But the front of the business remains human.”

What do you want brokers to take from Liberty’s performance in this year’s survey?

“It is great that we got recognition in categories we had not received before – overall service level, premium stability and product innovation. That gives us some comfort that what we are doing is working and that brokers are saying, ‘Yes, we appreciate that.’ At the same time, we need to take on board the feedback that we may be seen as too focused on the large international brokers. Good business is good business. We have learned over the years that you have to have a middle-market mindset as well, and that means a slightly different approach – faster, more standardised, but just as considered.”

What it takes to be among the best insurance companies in Australia

The 2026 survey results, read alongside broker commentary and the profiles of this year’s leading firms, reveal what makes the best insurance companies in Australia stand apart. Brokers are not voting on brand size or market share – they are voting on what it feels like to do business with an insurer day to day, year after year.

Responsiveness comes first. Across every category and every interview, speed of reply – on quotes, on renewals, on claims, even on declinatures – emerged as the single most consistent differentiator. Brokers do not just want fast answers; they want certainty. A prompt no is valued as much as a prompt yes.

Consistency over time matters almost as much. The insurers’ brokers rated highest were those that held their pricing discipline through both hard and soft markets, kept their people in place, and showed up with the same proposition year after year. Premium stability, retention of experienced underwriters, and long-standing client relationships all point to the same underlying quality: an insurer that brokers can rely on not to surprise them.

Beyond responsiveness and consistency, brokers valued genuine investment in the relationship – training, communication, accessible decision-makers, and technology that supports rather than replaces human contact. The firms that scored highest did not make brokers choose between digital convenience and personal service. They offered both.

Frequently asked questions

How are the ratings calculated, and what do the scores mean?

“Each participating broker rates insurers on a scale of 1 (very poor) to 5 (very good) across 11 performance categories. An average score is calculated for each insurer per category, with the top three earning gold, silver and bronze medals. The overall Insurer of the Year title goes to the insurer with the highest combined average across all 11 categories – effectively a broker-voted ranking of the best insurance companies in Australia – and goes to the insurer with the highest combined average across all 11 categories, reflecting the collective judgement of brokers with recent, first-hand experience of each firm.”

Why are only 11 insurers included, and can others join future surveys?

“The 11 insurers in the 2026 survey were selected because they are currently active in the Australian commercial market and have sufficient broker interaction to generate statistically meaningful sample sizes. The list is reviewed each year and may change to reflect shifts in the market. Insurers interested in participating in future editions should contact IBW at ibweekly.com.au.”

Why did Berkley Insurance Australia win Insurer of the Year?

“Berkley recorded the highest combined average score of any insurance company in Australia in the 2026 survey, claiming gold in four categories: Broker Communication, Training & Development; Overall Service Level; Premium Stability; and Turnaround Time – New Business. Brokers pointed to Berkley’s responsiveness, its relationship-driven culture, and its in-house BindIT platform as key differentiators. The result reflects a long-term, consistent investment in broker relationships rather than any single-year push.”

What does the current soft market mean for brokers and their clients?

“Soft conditions favour buyers: premiums are easing, insurer appetite is broader and competition for quality risks is more intense. EBM Insurance & Risk’s May 2026 report shows property rates down approximately 10–20%, cyber pricing down around 10% and casualty down roughly 7% year-on-year. That creates real negotiating leverage for brokers – but soft markets also demand sharper scrutiny of insurer quality, since the difference between a cheap premium and a reliable claims outcome matters most when everyone is competing on price.”

What are the biggest challenges facing Australian insurers heading into the second half of 2026?

“Gallagher Bassett’s Carrier Perspective: 2026 Claims Insights identifies three front-of-mind concerns: premium affordability and shrinking insurability (which jumped from sixth to first place between 2025 and 2026), escalating cyber and data security risks, and difficulty attracting and retaining skilled staff. All three are playing out against a backdrop of softening premiums, elevated natural hazard exposure – industry losses hit 0.46 billion in 2025, up from 85 million in 2024 – and ongoing regulatory reform from APRA and ASIC.”

How should brokers use the survey results when recommending insurers to clients?

“The results provide a peer-reviewed, independent benchmark of the best insurance companies in Australia, covering the service dimensions that matter most. Use them alongside your own experience – particularly in categories most relevant to your client’s needs, such as claims turnaround for high-frequency risks or premium stability for budget-sensitive businesses. A strong overall score signals consistent broad performance; category medals highlight specific strengths that may be decisive for a particular account. The results should always be read in conjunction with policy terms, pricing and the specific nature of the risk being placed.”

Best Insurance Companies in Australia |

Brokers on Insurers

Methodology

Brokers from across the nation were invited to rate the performance of a selection of insurers currently operating in Australia, providing an independent, broker-driven ranking of the best insurance companies in Australia. To ensure the results were relevant and timely, respondents were asked to rate only those insurers they had dealt with in the past 12 months.

Eleven insurers were rated by brokers in this year’s survey: AIG, Allianz, Berkley Insurance Australia, CGU, Chubb, Hollard Commercial, IAG, Liberty, QBE, Vero and Zurich. The brokers rated each insurer’s performance on a scale of 1 (very poor) to 5 (very good) across 11 different categories.

For each category, the insurers were ranked in order of merit according to an average score calculated from a tally of their ratings. The top three companies in every category received a gold, silver or bronze medal. The insurers’ combined average score from all categories determined the medallists for Insurer of the Year.

Keep up with the latest news and events

Join our mailing list, it’s free!