The Top Insurance Claims Carriers in Australia and New Zealand | 5-Star Claims

Jump to winners | Jump to methodology

Claims class

For brokers on the frontlines, the value of insurance is measured not in premiums or policies, but in how an insurer responds when things go wrong.

One experienced broker notes that the best insurance claims carriers understand their policy, the broker and the client. “Above all, understanding the client, their circumstances, their expectations and the impact a claim has on their life or livelihood transforms a claims experience from transactional to truly service-driven,” says National Insurance Brokers owner Abbie Wilson. “A little empathy and communication can go a long way in building trust and achieving timely and fair outcomes.”

Yet Wilson says the claims process often falls short, not for lack of systems or scale, but because of a disconnect in mindset. “As brokers, we pride ourselves on delivering a high standard of service that is both qualified and client-focused,” she explains. “The disconnect arises when claims teams do not appear to share these same core values. While brokers are working proactively and with urgency to support clients through what is often a highly stressful period, we are frequently met with delays, a lack of accountability and a reactive approach from insurers.”

“Brokers are not demanding perfection,” Wilson asserts. “They’re calling for a consistent, dependable standard of claims service that acknowledges the critical role insurers play during pivotal, and often distressing, moments in their clients’ lives.”

Across the Tasman, brokers in New Zealand are voicing similar priorities. “The most important thing a claims insurer can do to make a broker’s life easier is to communicate in a timely and informed manner,” explains PIC Insurance Brokers CEO Kristen Garner. “Our clients typically submit claims following stressful events, so it’s our responsibility to guide and support them through the process as efficiently as possible.”

While most insurer relationships are strong, Garner notes, one common friction point still lingers. “There can be too many layers of approval on the insurer’s side, even for relatively straightforward claims, which can slow down the claims process,” she says.

Vikki Langley, national claims manager at Abbott Insurance Brokers in New Zealand, agrees delays on smaller claims are a frequent point of friction and believes brokers could help speed things up if they were trusted with more authority.

“If we had delegated authority for certain claim amounts, we could give clients immediate reassurance,” she says. “Especially for smaller domestic claims, it would make a huge difference to be able to say, ‘Yes, this will be paid, and it will be paid within 24 hours.’ That level of responsiveness would lift the experience for everyone involved.”

Langley also sees a broader disconnect between broker expectations and the way claims processes actually unfold in practice. She believes that giving experienced brokers more flexibility, particularly in urgent situations like water damage, could prevent delays and protect clients from further loss. In her view, trusted brokers should be able to appoint assessors or organise make-safe repairs without waiting for formal claim numbers or approval layers.

Langley says there are signs of progress. She has been working directly with relationship managers at several insurers to improve how claims are handled for larger clients.

In some cases, she’s helped establish preferred assessors and builders in advance, so urgent work like make-safe repairs can be approved and paid without unnecessary delays. “They are working better,” she notes. “And it’s encouraging to see insurers becoming more open to these kinds of practical solutions.”

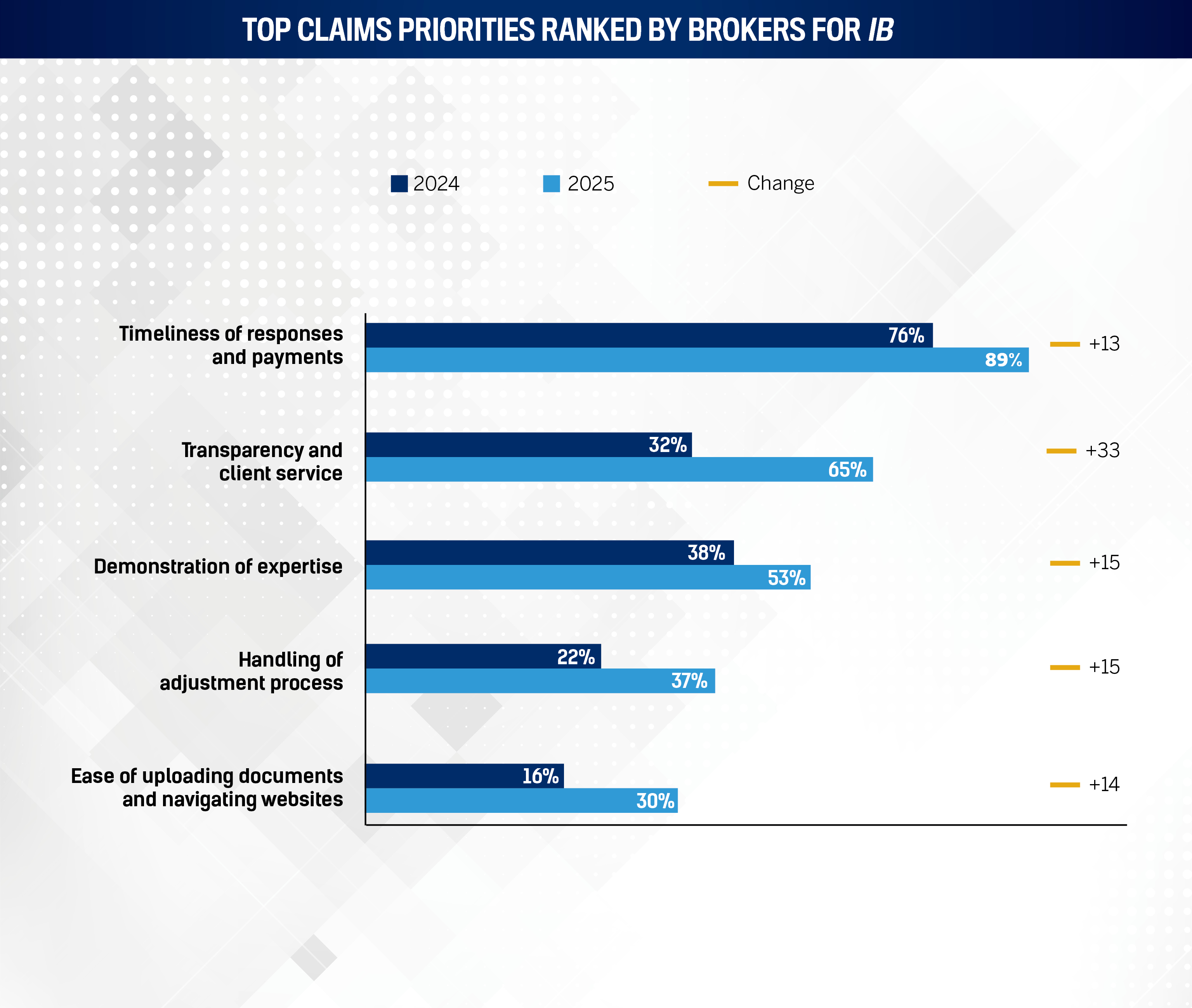

Overall trend between 2024 and 2025: rising expectations across all categories

Across every category listed, broker expectations and preferences increased from 2024 to 2025, indicating a heightened focus on claims service quality. This reflects a broader industry shift towards enhanced client service, speed and digital efficiency.

Category-by-category analysis

1. Timeliness of responses and payments

-

2024: 76%

-

2025: 89 (+13 percentage points)

Insight: This remains the top priority, and its importance grew significantly. With claims being the most critical customer touchpoint, brokers clearly value faster resolutions and communication more than ever.

2. Transparency and client service

-

2024: 32%

-

2025: 65% (+33 percentage points)

Insight: This category saw the largest relative increase. Brokers are increasingly emphasising clear, consistent communication, proactive updates, and client-centric claims handling.

3. Demonstration of expertise

-

2024: 38%

-

2025: 53% (+15 percentage points)

Insight: This reflects a growing demand for technically knowledgeable adjusters and accurate assessments. Brokers are expecting insurers to provide strategic insights, not just process transactions.

4. Handling of adjustment process

-

2024: 22%

-

2025: 37% (+15 percentage points)

Insight: There is increasing scrutiny on how well claims adjustments are executed. Efficiency, fairness, and clarity in this process have become more influential in broker satisfaction.

5. Ease of uploading documents and navigating websites

-

2024: 16%

-

2025: 30% (+14 percentage points)

Insight: While still the lowest-ranked, digital ease of use is gaining importance, suggesting brokers want simplified, intuitive digital interfaces to streamline claims documentation and communication.

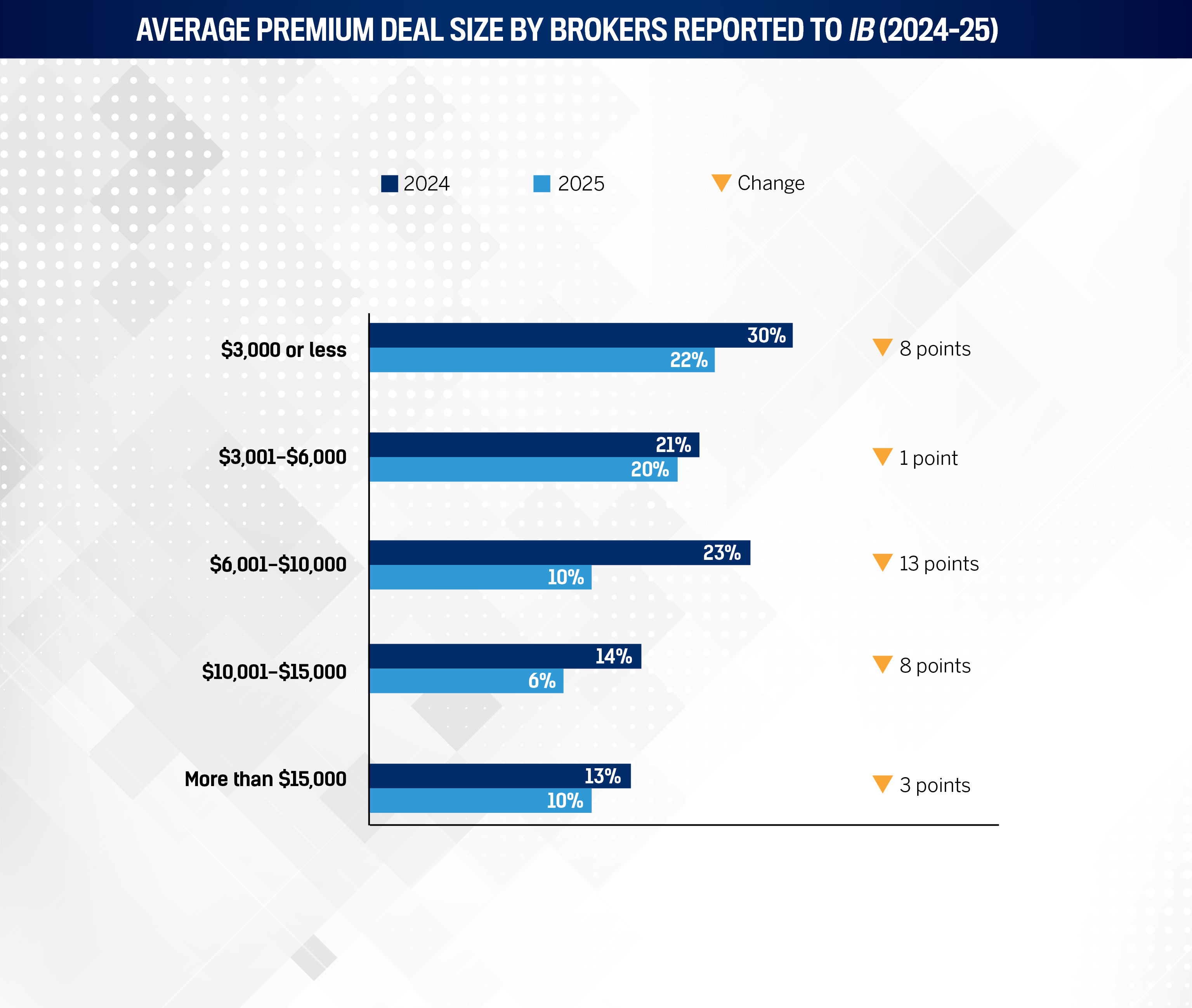

1. Clear shift towards smaller concentration of lower mid-tier deals

Across almost every premium bracket below $15,000, there’s a notable decline in percentage share in 2025 compared to 2024. This signals a consolidation of brokerage focus towards either higher-value deals or a shrinking mid-market segment.

2. Major decline in the mid-tier ($6,001–$10,000)

The largest drop occurred in the $6,001–$10,000 bracket, which fell by over 13 percentage points – from 23% in 2024 to 10% in 2025. This suggests:

-

Fewer mid-size deals are being closed

-

Brokerages may be moving clients into larger policies, or those mid-market clients may be leaving the market or consolidating coverage

3. Strategic implications for the industry

- The decline across all brackets hints at a fragmented or compressed market, possibly affected by:

- economic constraints on client budgets

- increased competition

- shifts in client risk profiles and premium pricing models

- Brokerages may need to:

- reassess value propositions for mid-market clients

- evaluate cost-to-serve for smaller deals

- reassess value propositions for mid-market clients

A year that tested the top insurance claims carrier teams

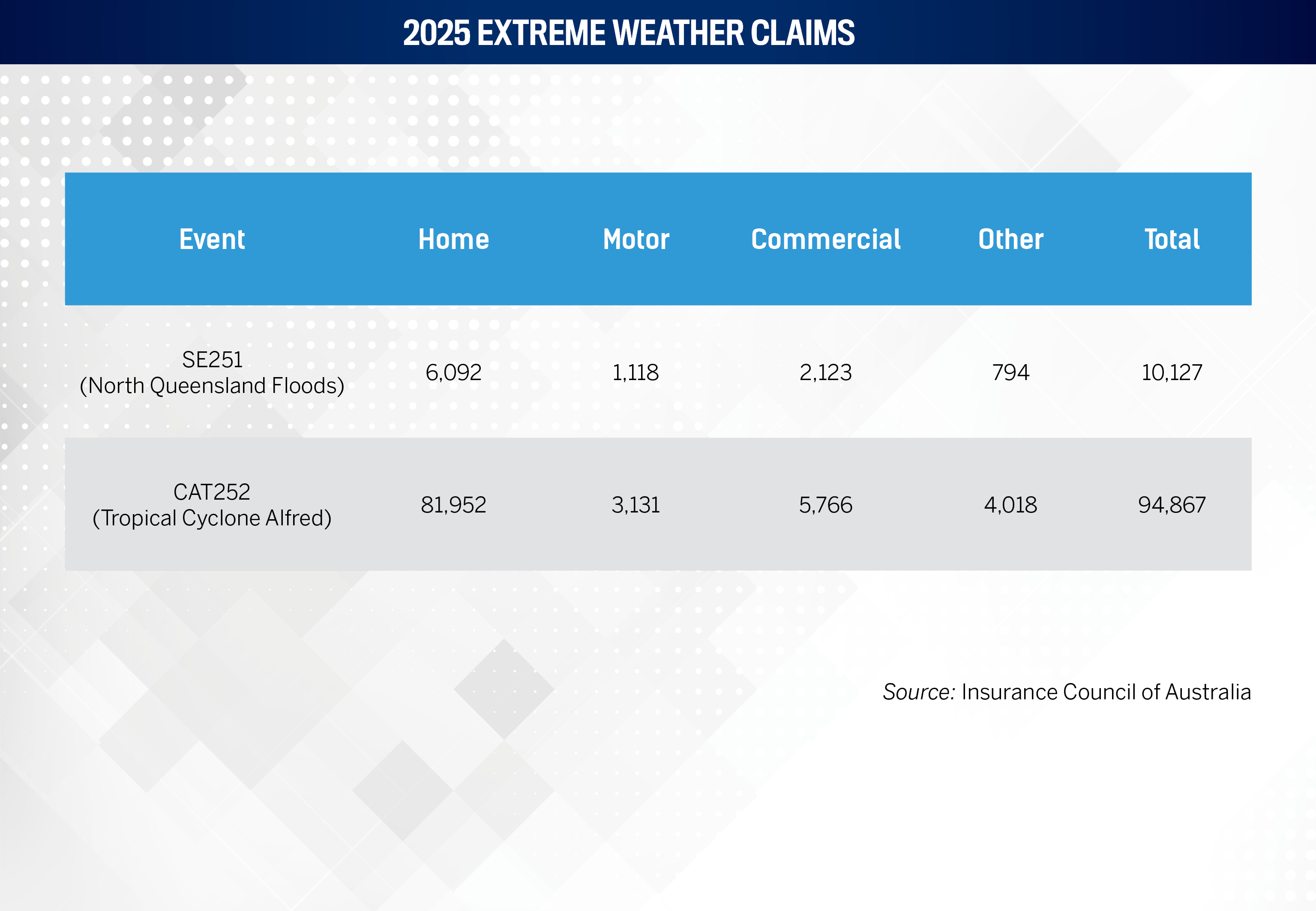

For insurance claims carriers across Australia and New Zealand, the past year has brought no shortage of challenges. Data released by the Insurance Council of Australia (ICA) in April 2025 reveals that insurance losses from ex-tropical cyclone Alfred and February’s North Queensland floods have exceeded $1.2 billion.

Insurers have received nearly 95,000 claims relating to damage following Alfred, totalling almost $1 billion, with 30% of claims settled to date. The country’s insurers have also received over 10,000 claims related to the floods, totalling $233 million.

Many of these claims are due to food spoilage and water ingress from various sources, including wind-driven rain, overflowing gutters and inundation.

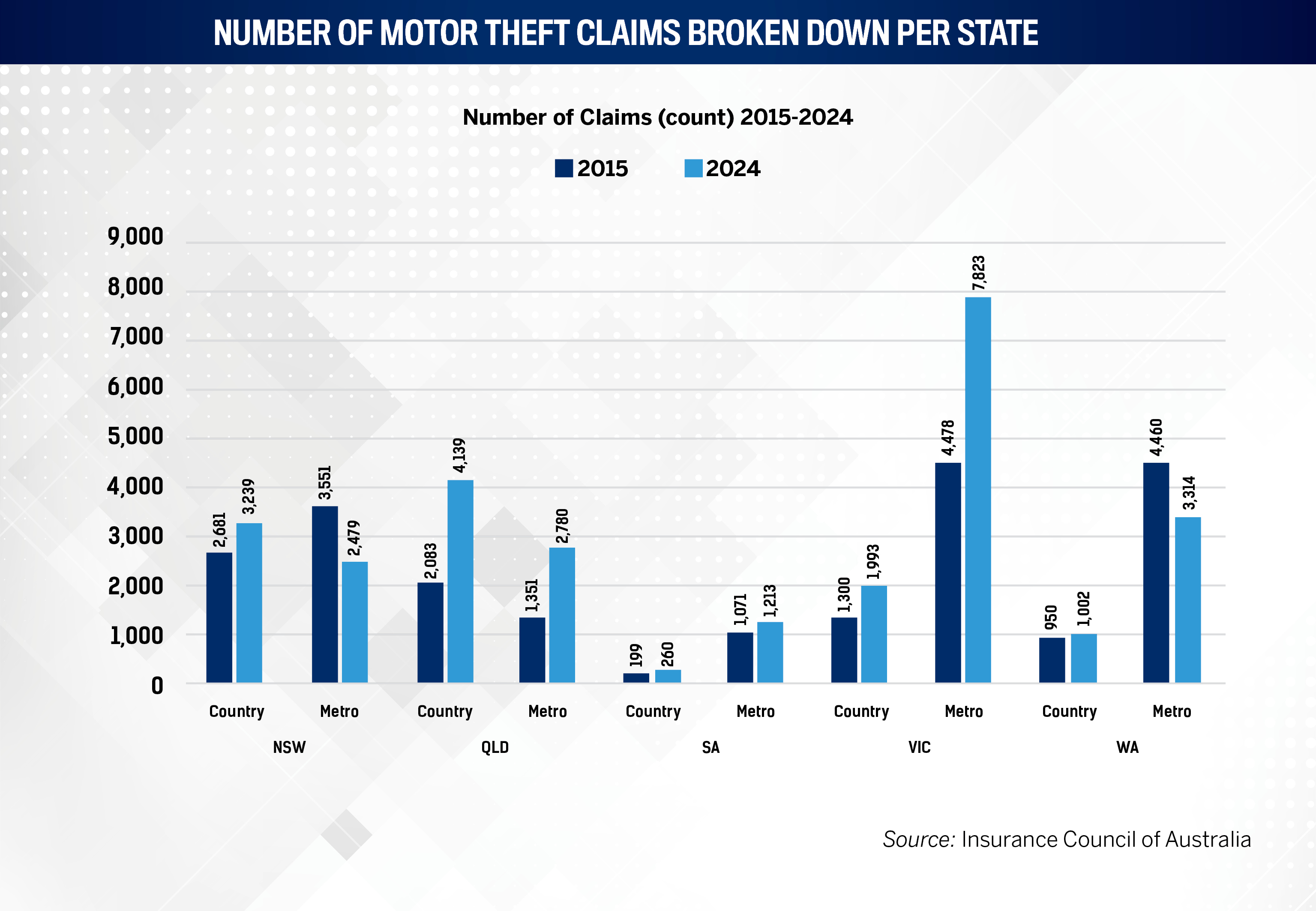

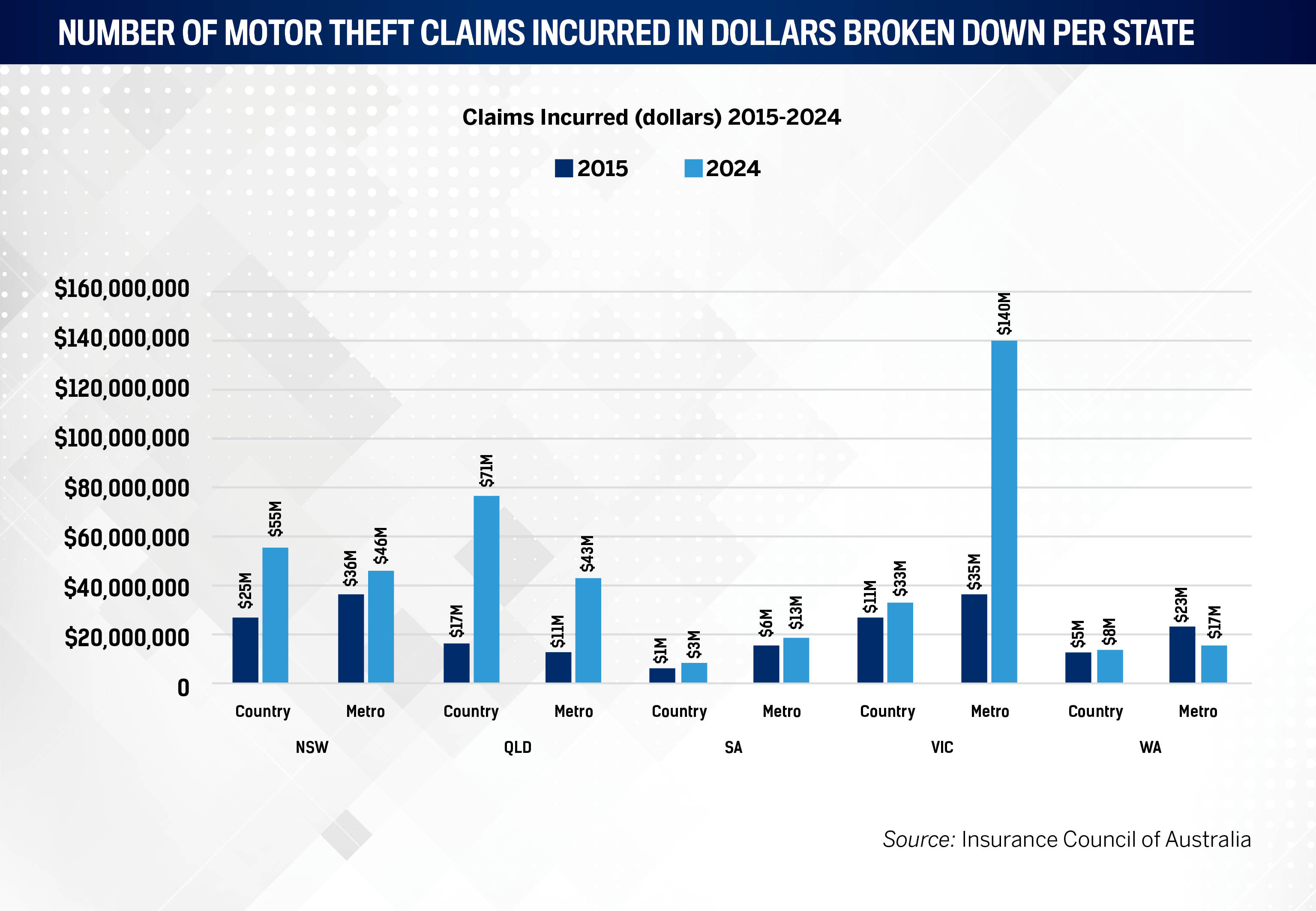

Ongoing climate risk wasn’t the only factor keeping insurers and top claims carriers at the top of their game. ICA reported in March 2025 that motor vehicle theft claims are increasing significantly in some parts of the country.

Across the same period, the number of motor vehicle theft claims rose from 22,000 in 2015 to 28,000 in 2024, up 27%, with Queensland and Victoria experiencing the highest increases.

Claims in Queensland rose 101%, and the value of those claims increased from $28 million to $113 million, or a 214% increase in real terms.

-

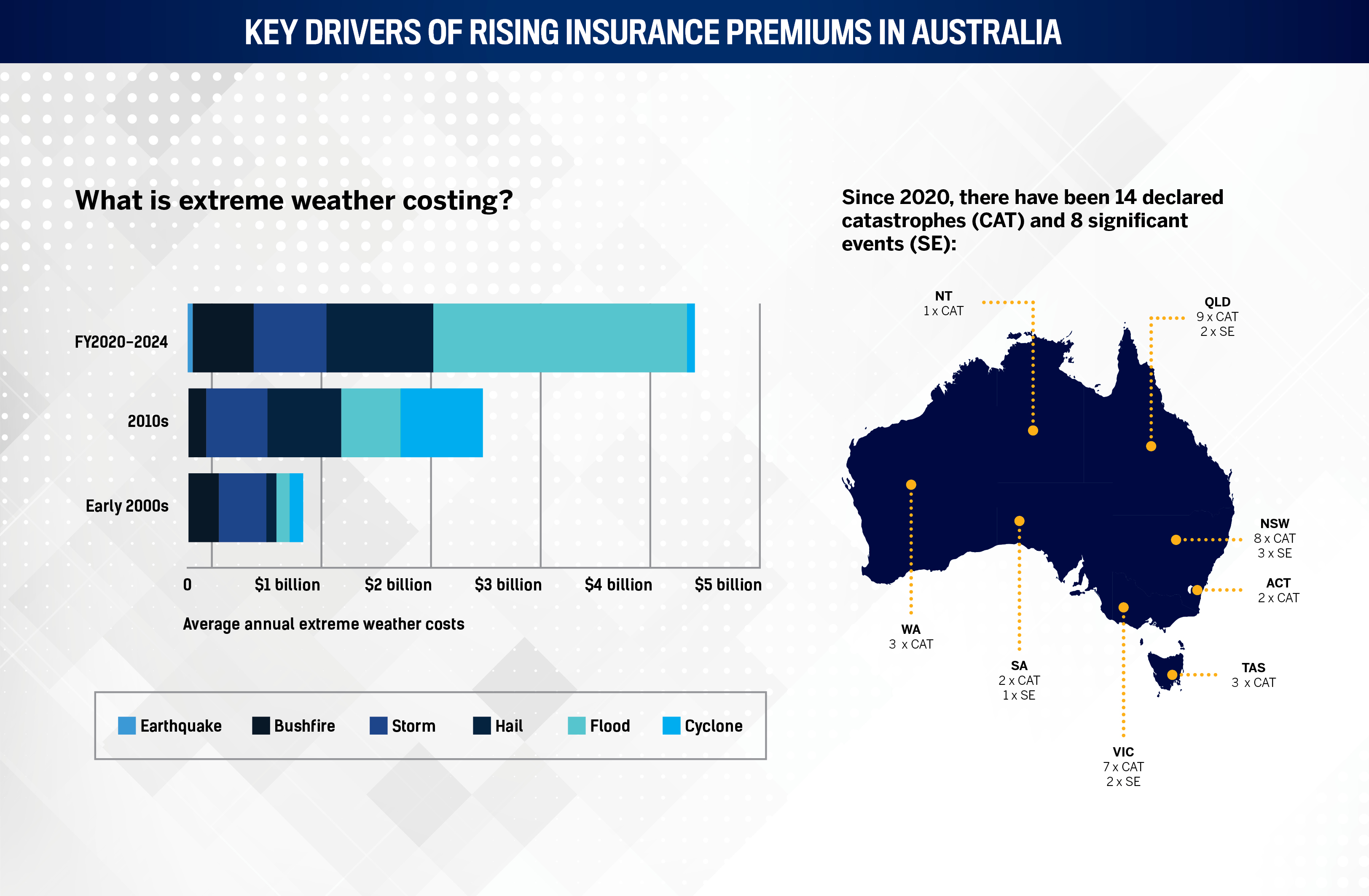

Extreme weather events: Over the past five years, insured losses from extreme weather events totalled $22.5 billion, averaging $4.5 billion annually. This represents a 67% increase compared to the previous five-year period.

-

Reinsurance cost increases: Reinsurers have raised reinsurance prices to 20-year highs globally in response to escalating extreme weather costs. Australian insurers have faced increases of up to 30%, some of which have been passed on to policyholders.

-

Development in high-risk areas: Approximately 1.4 million properties in Australia are at some risk of flooding, including nearly 300,000 properties facing severe to extreme annual flooding risk, predominantly in NSW, Qld, and Vic.

-

Rising construction costs: The average cost to build a new house in Australia has increased by 29% since 2019, from approximately $345,000 to around $444,000 in 2024. In Queensland, the increase was from $310,000 to $450,000, averaging a 10% annual rise.

-

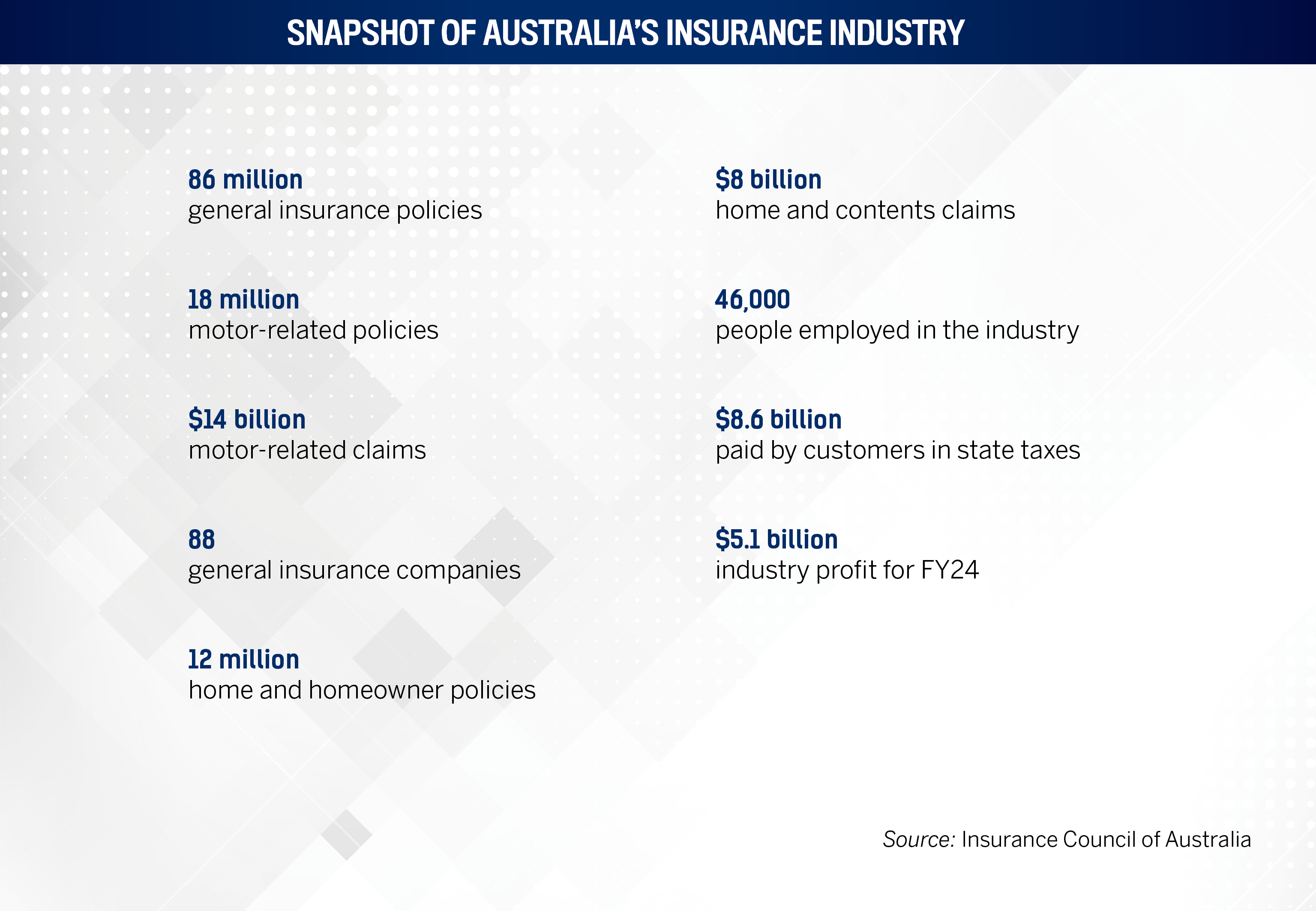

State-imposed taxes: Taxes add 20% to 40% to the price a customer pays for a premium. In the 2023–24 financial year, state governments collected nearly $8.6 billion in stamp duty and other levies from insurance customers, $3.5 billion more than the insurance industry's profit that year.

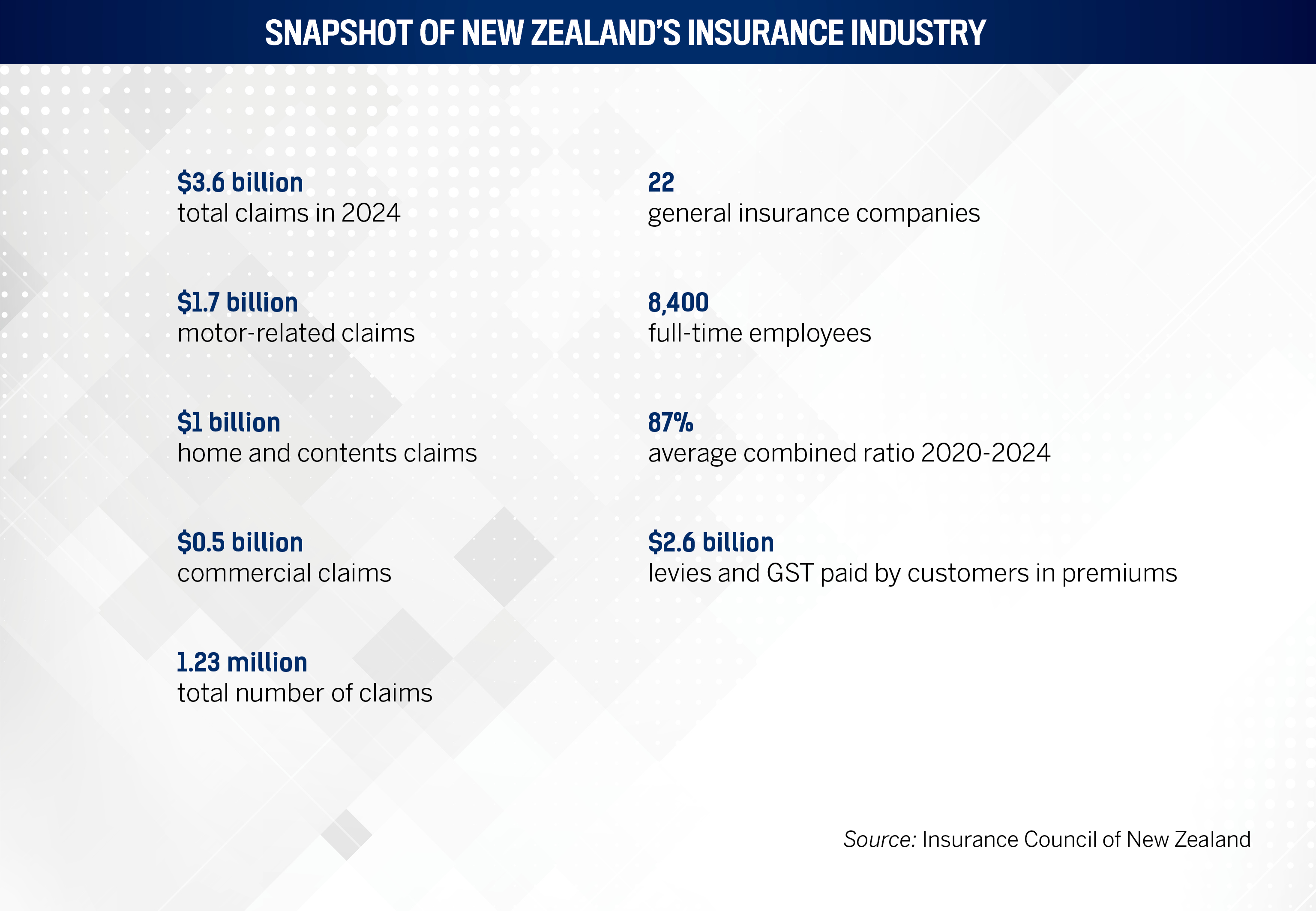

New Zealand has experienced higher premiums due to the rising cost of extreme weather events, growing value of assets, inflation in the building construction and vehicle repair sectors, rising cost to insurers of doing business, and taxes and levies, according to the Insurance Council of New Zealand.

Natural disasters have caused over $31.2 billion in insurance claims since 2010, split between earthquakes (80%) and extreme weather events (20%).

Insurance fraud also constitutes a threat to local insurance companies. In 2024, over 1.2 million searches were conducted in the Insurance Claims Register to legitimise insurance claims, an increase of 35.8% from the previous year.

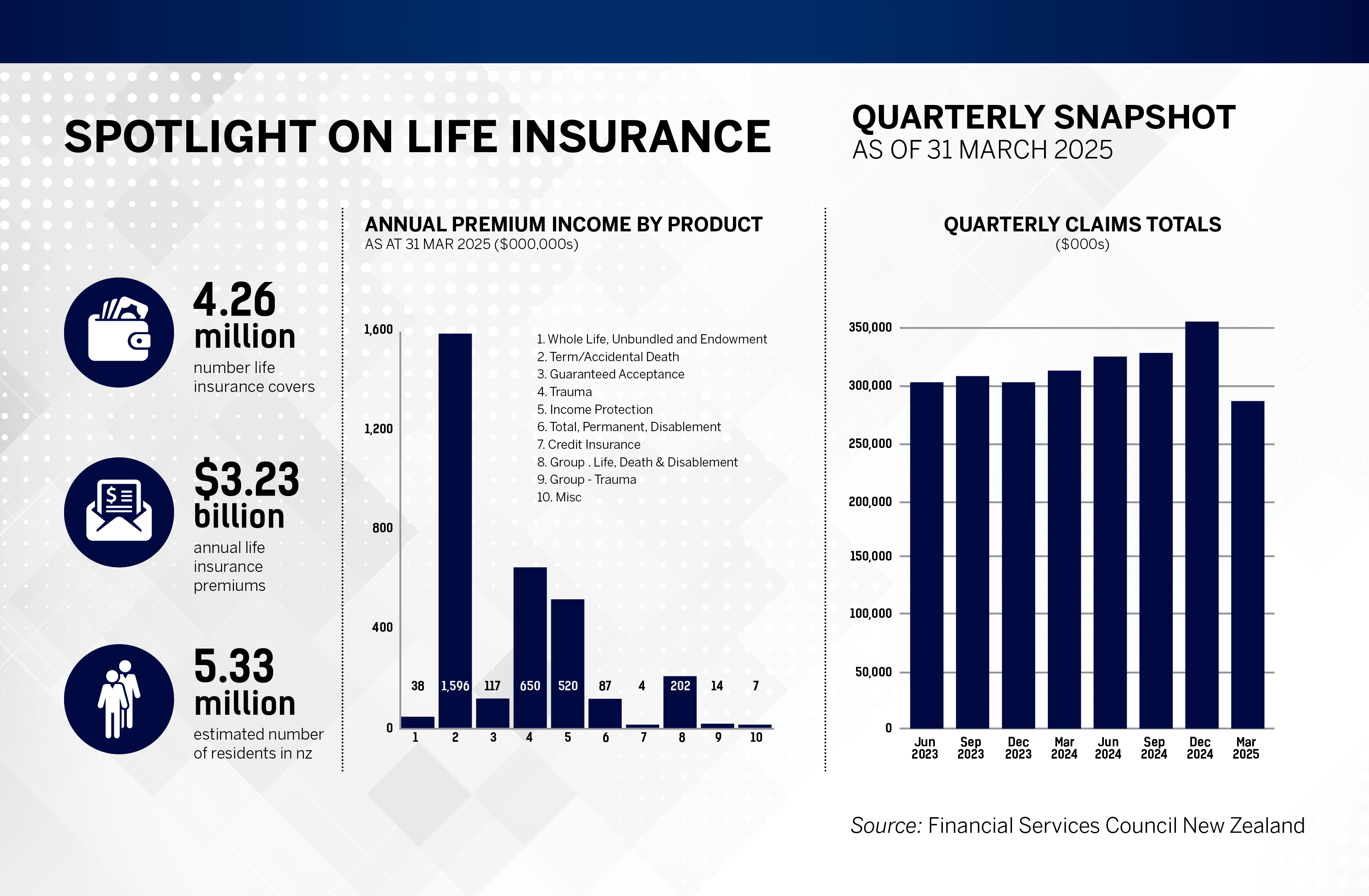

There has been good news in New Zealand’s life insurance sector. As of March 2025, the Financial Services Council of New Zealand data shows the highest number of covers in more than five years, with 1.8% growth year on year.

Claims have also been at their lowest since March 2023, with the first quarter of 2025 showing that the reduction has been driven by an overall decrease in claims accepted for most products, except for Guaranteed Acceptance.

Within the context of the ongoing industry challenges in both countries, this year’s 5-Star Claims winners showed what sets them apart, as they consistently delivered on the fundamentals:

-

speed

-

transparency

-

expertise

-

client care

They responded under pressure, adapted when needed, and didn’t lose sight of the human experience behind each claim. Many of this year’s top performers also invested in how claims are managed behind the scenes.

At repeat 5-Star Claims winner Arch Insurance Australia, for example, that included assigning dedicated staff to support claims teams with payment processing, setting a high bar for service delivery, and building flexible digital tools tailored to broker and client needs.

These practical steps, combined with strong communication and specialised claims expertise, have helped all the leading claims providers strengthen trust, even under pressure.

To determine the 5-Star Claims Service Providers for 2025, Insurance Business surveyed brokers across Australia and New Zealand, asking them to rate the providers they had worked with over the past year. The responses were weighted according to the factors brokers said mattered most, such as quality of work, specialist expertise, and client service. The firms with the highest scores earned 5-Star status for delivering standout claims support.

Based on IB’s 2025 data, brokers demand faster, clearer and more expert-led claims service. What used to be differentiators, such as timeliness, transparency and service, are now table stakes.

Wilson believes that top claims carriers must focus on delivering consistency, competence, and genuine collaboration with brokers to remain competitive. “A stable, predictable standard of claims handling is no longer a nice-to-have; it’s essential,” she says. “The carriers who lead the future of claims will be those who prioritise expertise, partnerships, and a client-first mindset every single time.”

Speed tops broker priorities in 2025

Timeliness of responses and payments surged to the top of brokers’ priorities. As claim volumes rise and clients push for faster resolutions, speed is no longer a competitive edge but a minimum expectation.

Garner agrees, noting that claims carriers must do more than just meet basic benchmarks if they want to stay ahead. “In the fast-paced world we live in today, clients expect prompt service and payment from claims providers,” she says. “Having the right systems, processes, and personnel in place to ensure a timely response to claims submissions has become a starting point to remain competitive.”

She adds, “When delays are expected due to additional approvals required or during a busy period, it’s important these are communicated with our clients as soon as possible to manage expectations and ensure transparency.”

To keep up with rising expectations around speed, Arch has set internal benchmarks for how quickly claims and payments should be handled and built systems to back it up.

With brokers naming timeliness as their top priority, the company has invested in technology that helps move claims forward. The top claims carrier has significantly invested in systems technology that enables smooth and accurate transactions.

This approach includes:

-

dedicated staff specifically assigned to support the claims team with payment processing, ensuring that customers and stakeholders receive payments promptly and efficiently

-

technology solutions that streamline workflows while maintaining accuracy checks

-

service level agreements that set clear expectations and measurable performance standards

“These systems work together to deliver on our promise of high-standard claims service while maintaining the technical accuracy that complex claims require,” explains claims manager Joe Donovan.

Joe DonovanArch Insurance Australia

Balancing tech tools and personal service

Brokers are feeling the pressure to move faster, and so are the systems they rely on. With clients expecting quick answers, brokers are turning to insurance claims carriers with digital tools that are simple, fast, and built to take the friction out of the process.

While those tools are helpful, National Insurance Brokers’ Wilson cautions that technology alone can’t carry the claims experience. “Technology and online portals certainly have a place in modern insurance; they can streamline the initial claims process, improve documentation flow, and offer convenience for both brokers and clients,” she says.

“But no portal, chatbot, or automated system can replace a qualified claims professional's reassurance, judgement, or expertise.”

She notes that too often, the process breaks down after the initial tech interaction of lodging and tracking claims on portals. “We frequently find that once a claim is submitted, there’s no timely human response or meaningful engagement on the other end, and that’s where frustration sets in,” she explains.

PIC Insurance Brokers’ Garner shares a similar view, noting that digital platforms are especially powerful when they support strong human connections. “Our ability to integrate with the claim’s insurer’s online portal is incredibly important as it allows us to track claims updates live,” she says. “This is particularly helpful when we receive queries from our clients, meaning we can provide them real-time updates on their claim’s status.”

Still, she adds, it’s people, not just platforms, who ultimately shape the claims experience. “The most important factor will always be the people-to-people relationships built between the claim’s insurers and the claims teams at brokers, as it is ultimately the people who are using these systems that make the most difference.”

For Wilson, the winning formula combines innovative systems with skilled professionals. “While we welcome the support of technology, it must work alongside experienced professionals, not in place of them,” she adds.

Abbott Insurance Brokers’ Langley says the value of insurer technology depends on how well it’s built and whether it actually helps brokers do their job. One major insurer she works with allows document uploads and instantly creates a claim number, which streamlines communication.

But with others, the process stalls. “Some portals just show basic updates,” she says. “We still have to email everything in and then wait for someone to pick it up. That slows things down.”

Langley sees digital investment as essential, but not something to rush. “Technology is where the industry’s heading, no question,” she adds. “People want instant answers. But you have to get the basics right first. Don’t just drop in a temporary system to tick a box. Build something that’s going to last and that actually works for brokers and clients.”

That balance is something leading claims carriers like Arch are working to strike. “We recognise that digital efficiency is increasingly becoming a differentiator in the claims experience,” Donovan says. “Our approach doesn't adopt a one-size-fits-all philosophy. Instead, we offer flexibility to our stakeholders, particularly brokers, regarding client-specific service expectations.”

As part of a broader commitment to improving the digital journey for brokers and clients, the company has invested in claims technology that supports faster transaction processing and adaptable service.

While maintaining a focus on personal relationships, Arch has been enhancing its digital capabilities in several ways, including:

-

implementing technology that facilitates faster transaction processing

-

creating flexible digital solutions tailored to specific broker and client needs

This approach allows Arch’s team to provide digital solutions that complement its high-touch service model while meeting the varying needs of different clients and risk profiles.

Building trust through transparency

Transparency and client service are now at the heart of what brokers expect. It’s a sign that more than ever, clients want to know what’s happening with their claim, and they’re looking for communication and status updates.

Arch’s commitment to transparency and client service is reflected in its Pursuing Better Together® ethos. The team builds trust through communication, understanding its clients' businesses and risks and collaborative relationships with stakeholders in the claims process.

To address the growing importance of transparency, it emphasises a four-pronged approach:

-

maintain excellent working relationships with stakeholders to understand expectations and service requirements, whether claim, portfolio, or customer specific

-

provide regular, clear updates throughout the claims process

-

offer flexibility to brokers regarding client-specific service expectations

-

take a proactive approach to regulatory compliance across the sector

“We train our claims professionals to communicate complex information clearly and empathetically, recognising that claims situations can be stressful for all involved,” Donovan says. “Keeping lines of communication open and providing timely updates ensures that brokers and their clients feel supported and informed throughout the claims journey.”

Knowledge is power

As claims grow more complex, brokers are placing a premium on technical know-how and industry-specific knowledge.

At Arch, that trend is front and centre. The company carefully selects claims professionals with relevant technical expertise in each area of risk it underwrites. “Expertise, experience and trust work together to assure clients that their claims are in the hands of professionals who understand their risks,” notes Donovan.

The company’s approach to technical excellence includes:

-

rigorous selection process for claims professionals that prioritises relevant industry and technical knowledge

-

a professional development program, which encourages claims professionals to continually develop their skills in the relevant fields they service, some of which are complex and continuously evolving

-

recent expansion of our team to include dedicated specialists, such as accident and health claims professionals, enabling it to provide enhanced serviceability across specific product lines

-

careful selection of service providers to ensure expertise across each risk exposure

Wilson views this level of expertise as non-negotiable. “Specialist expertise is absolutely vital in the claims process,” she says. “In those moments, there is simply no substitute for knowledgeable, experienced claims professionals.

“We can no longer afford a system where claims roles are filled without the necessary understanding of policy wordings, risk nuances, and client expectations. Expertise matters because it ensures fairer, faster resolutions and upholds the integrity of the entire insurance process.”

Still, Wilson has observed that the broader market has a long way to go. “Truthfully, the standard and performance of claims providers across Australia and New Zealand has diminished significantly in recent years,” she says. “While there may be isolated areas of improvement or innovation, the overall experience for brokers and clients has become increasingly frustrating and inconsistent.”

Langley says she has experienced those same frustrations firsthand. For her, the issue isn’t just about technical training; it’s about giving brokers access to people who can actually move a claim forward.

“There’s nothing more frustrating than trying to sort out a claim that’s gone wrong and getting someone on the phone who doesn’t understand what you’re talking about,” she says. “Sometimes we just need a simple answer, but if it’s not on their script or it’s outside their delegated limit, we end up going in circles. Meanwhile, the client’s still waiting.”

She points out that clients often feel the impact most, especially when delays affect when or how quickly a payout is made. “At the end of the day, people want to know when they’re getting paid. That’s the bottom line,” says Langley.

That concern is echoed by New Zealand’s Garner, who says specialist expertise from a claims provider is critical to building trust and transparency. She also notes that New Zealand claims providers have greatly improved the timeliness of responses in recent years.

“In their time of need, our clients want to know they are in good hands, so being able to showcase a deep understanding helps them navigate what can be a stressful time,” she adds.

Where claims are headed next

Capgemini Research Institute’s Insurance Top Trends 2025 report identifies three forces driving the future of Australia’s insurance sector:

-

customer-centricity

-

stronger enterprise operations

-

a broader industry push towards intelligent, tech-driven transformation

Whether in P&C, life or health, insurers are zeroing in on experience, efficiency and innovation, with claims positioned as a pressure point and growth opportunity.

Meanwhile, KPMG Australia highlights that insurers are leaning heavily on digital transformation, with AI investments already showing strong returns and set to increase. Firms are also preparing for sweeping regulatory changes and the rollout of mandatory climate disclosures, emphasising operational resilience and risk preparedness.

In New Zealand, the largest overhaul of insurance law in over a century passed in 2024. Known as the Contracts of Insurance Bill, this new legislation consolidates and modernises previous insurance laws, aligning the country with international best practices and reforms in Australia and the UK.

The key changes in claims include:

-

Payment of claims: An implied term now requires insurers to pay claims within a reasonable time, allowing flexibility based on claim complexity and investigation needs.

-

Time for making claims: The rule that insurers can’t generally decline claims based on late notification is retained, with a new 90-day notification period for “claims-made” policies.

-

Increased risk exclusions: Insurers can now exclude claims based on specific increased risks, such as driver qualifications or commercial use of personal vehicles.

-

Third-party claims against insurers: With the court’s approval, a third party can now directly claim from an insurer if the policyholder is insolvent or deceased.

KPMG New Zealand also points out the benefits that AI could bring to the insurance sector, specifically:

-

fraud detection

-

customer experience

-

managing higher volumes and event responses

In New Zealand, Langley says she’s seen improvements but worries they may not hold under pressure. “We’re definitely on the better side of it at the moment, because we’ve had no major disasters,” she says. “But I do worry that if we do get another natural disaster, whether we have the capacity to meet client expectations.”

Top-performing insurance claims carriers are responding to these changes and moving the needle forward on what it means to deliver in the current environment.

At Arch, leaders say the role of claims providers is changing quickly, driven by broker expectations, new technology, and increasingly complex risks. To stay ahead, the company is investing in its digital systems and building the skills of its people while continuing to prioritise technical expertise.

Arch has identified several key shifts that are likely to shape the future of claims service:

-

Greater integration of technology and human expertise: Smart systems help, but it’s the people and their knowledge, empathy and judgement who make the difference.

-

Increased focus on transparency and communication: Brokers want clear updates and honest conversations throughout the claims process.

-

More proactive and consultative relationships: The best claims teams help brokers and clients stay ahead of risks.

-

Enhanced specialisation: Complex claims call for professionals who know the product and the industry through and through.

-

Greater emphasis on data and analytics: Using data well means faster decisions, fewer surprises, and a more tailored service for every client.

“We’re preparing for this evolution and will continue to deliver the kind of service that turns claims providers into strategic partners,” says Donovan.

Conclusion: brokers demand more, and the best carriers are delivering

The days when speed, communication and expertise were “value-adds” are over. In today’s market, they’re expected by default. The leading claims providers are setting themselves apart through:

-

technology that supports – not replaces – human service

-

specialised expertise and accountability

-

a shared mission with brokers: putting the client first

The Top Insurance Claims Carriers in Australia and New Zealand | 5-Star Claims

- AFA Insurance

- AIA

- Allianz

- Ando

- CGU

- Chubb

- NZI

- QBE

- Vero

Insights

-

-

Kristen Garner

Kristen Garner

Chief Executive Officer

PIC Insurance Brokers -

Vikki Langley

Vikki Langley

National Claims Manager

Abbott Insurance Brokers

Methodology

To select the best claims service providers for 2025, Insurance Business sourced feedback from insurance brokers. IB’s research team began by surveying a wide range of brokerages to determine what brokers value in a claims service providers. The team also spoke to hundreds of brokers across the country, asking them to rate the claims service providers they had worked with over the past 12 months.

The in-depth information gathered enabled the research team to assign weighted values to each of the criteria being rated by brokers. At the end of the research period, service providers that received the highest rankings in terms of work quality, specialist expertise and client service were named 5-Star award winners in claims service providers.

Keep up with the latest news and events

Join our mailing list, it’s free!