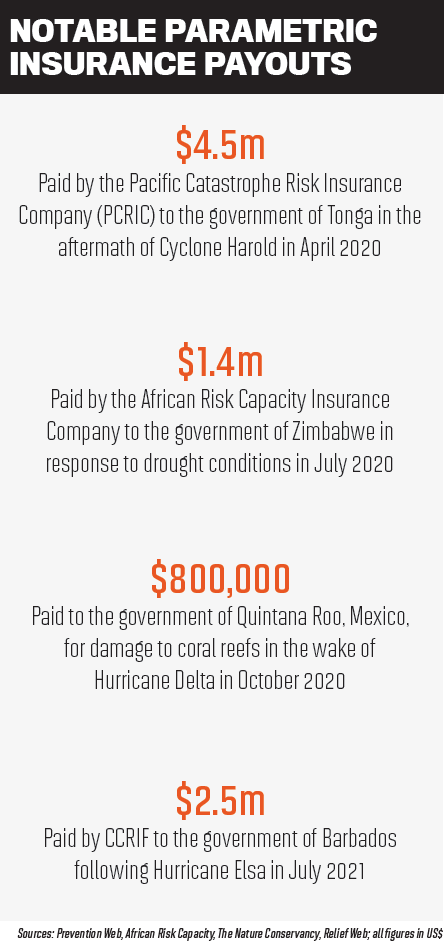

In August, a parametric insurance policy written by the Caribbean Catastrophe Risk Insurance Facility (CCRIF) was triggered by the 7.2-magnitude quake in Haiti, delivering a record payment of $40m. Within a week of the disaster, CCRIF had paid $15m of the claim to the Haiti government, shining a spotlight on how quickly and efficiently parametric insurance can support devastated communities.

“Parametric insurance ensures that a payout is triggered automatically once a pre-defined threshold of an index is reached or exceeded, meaning policyholders get paid without having to go through a relatively lengthy insurance claim and loss adjustment process,” explains David Mäder, head of sales and delivery for P&S solutions at Swiss Re.

The growing frequency of natural catastrophes around the world has resulted in substantial economic losses and adverse social impacts, and Mäder says this frequency is likely to continue to increase in many parts of the world. Weather-related catastrophes remain massively uninsured in many countries, particularly in emerging and developing markets, presenting a strong need to offer broader insurance coverage that can increase the financial resilience of vulnerable communities. Parametric insurance offers one suitable option for bridging this protection gap.

Parametric solutions started as weather derivatives in the energy markets during the 1980s, but have since evolved across the insurance space. Unlike traditional insurance solutions, parametric insurance allows for the use of insurance and risk transfer tools to address very short-term needs, says Simon Young, senior director of Willis Towers Watson’s Climate and Resilience Hub.

“Both public and private entities have trouble financing emergency response within annual or multi-annual budgeting cycles,” he says. “You can put aside a rainy day fund, which is the current, traditional way that we think about dealing with disasters, but there’s usually a limit to how much money you can set aside which isn’t being put to work.”

“By insuring against a catastrophic weather event, parametric insurance can round out a customer’s insurance coverage by purchasing additional cover against a specific peril,” adds Jonathan Charak, emerging solutions director for Zurich North America. “Further, the purely objective nature of para-metric insurance provides clear pricing and discussion of the chance an event occurs.”

Young and Charak both emphasise that a key point of difference between traditional insurance and parametric insurance is the speed at which a claim can be paid. These faster payouts support vulnerable communities affected by climate change and natural catastrophes with immediate cash relief, Mäder says. Therefore, promoting alternative channels of insurance in regions of the world with large protection gaps could have a major impact in reducing the overall losses from natural catastrophes.

Parametric insurance allows insureds faster, unrestricted access to payouts, Charak says, which in turn enables them to use the money in the most efficient way possible to recover from a catastrophe. From a claims perspective, he says, the quick payout potential of parametric insurance offers value to customers beyond just being able to insure something that wasn’t covered in the past. The trigger in the insurance contract provides certainty that when conditions are met, a payment will be made.

“Parametric insurance is a viable proposition providing a way to secure protection against precisely the conditions that affect or threaten your businesses,” he says. “Once this is designed, an insurance company can offer a quick and clear claims process, as the claims process is streamlined. Further, putting clear pricing on a specific CAT event helps the insured understand the cost of the risk, and they can decide how to mitigate future risk.”

Parametric insurance lets government agencies, for example, take advantage of much more streamlined pre-, during- and post-event management, Mäder says, enabling a faster recovery and rebuilding of critical infrastructure and services. Young adds that the research points to compelling recovery and economic benefits of having money quickly available in the wake of natural disasters.

Parametric insurance lets government agencies, for example, take advantage of much more streamlined pre-, during- and post-event management, Mäder says, enabling a faster recovery and rebuilding of critical infrastructure and services. Young adds that the research points to compelling recovery and economic benefits of having money quickly available in the wake of natural disasters.

“One of the things we have seen is that if you know you’re going to get some money, then that really incentivises making a plan for how you’re going spend that … and we see that across the full spectrum of the clients that we’re working with,” Young says. “The value of insurance for incentivising better risk behavior is very real. And we think that parametric insurance is a way to bring that to countries and to settings where traditional insurance either has low penetration or hasn’t been thought about in the context of being useful.”

Mäder notes that the increasing global interest in parametric insurance solutions also brings opportunities for insurers to access new distribution channels. “There is still a lot of room to fully leverage the benefits of parametric covers,” he says. “Insurers and regulators, as well as reinsurers such as Swiss Re, have important roles to play to grow the adoption of parametric products.”