Rising fuel costs and weaker business sentiment are highlighting ongoing cost pressures for Australian households and companies, with potential implications for insurers’ pricing, coverage decisions, and claims experience.

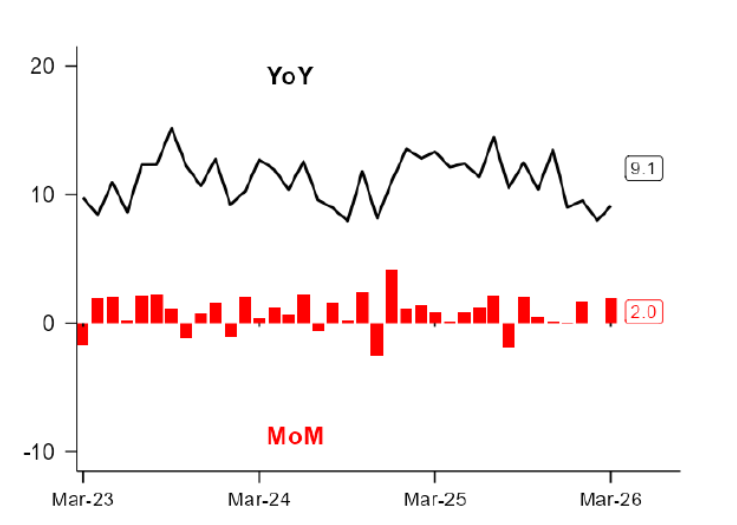

Australian consumer spending increased in March, with most of the month’s rise concentrated in essential categories, especially fuel. NAB’s latest Consumer Spend Trend report shows total consumer spending was up 2.1% month on month, with fuel the main contributor to the increase. NAB chief economist Dr Sally Auld said the figures show how higher living costs are influencing household spending patterns. “Consumer spending rose 2.1% in March, driven by a sharp 33.5% increase in fuel spending following the fuel price surge,” Auld said.

Excluding fuel, spending rose 0.7% over the month, supported by higher food spending and increased construction-related outlays. Fuel spending was 25.7% higher over the year. NAB said fuel price growth exceeded growth in spend per transaction, indicating an increase in the number of fuel transactions. This is consistent with more frequent smaller refuelling and precautionary purchases as prices moved higher. “For now, consumers have absorbed higher fuel expenses with only a small impact on their broader spending. However, there is clear underperformance among discretionary categories, particularly hospitality, travel, and personal services,” Auld said. Spending rose across all states and territories in March, with South Australia and Queensland recording the largest monthly gains. Over the past year, national spending growth has been led by essential categories, particularly utilities and fuel, pointing to a shift in budgets toward non-discretionary items.

NAB’s special analysis on fuel reported a 34% month-on-month rise in fuel spending and 25.7% growth over the year, with New South Wales and Victoria recording the strongest monthly increases. Fuel spending growth was higher in older age groups, which NAB said may reflect either greater capacity to manage higher costs or more cautious purchasing behaviour. According to NAB, household budgets in March shifted toward non-discretionary items, led by fuel, while discretionary spending declined, particularly in hospitality, hotels, travel, and personal goods. Excluding fuel, the share of spending across other non-discretionary categories changed little, suggesting limited flexibility to reduce essential purchases. Food spending was supported in part by stockpiling of non-perishable items by some households.

Within “other services,” NAB reported that spending growth over the year was driven by construction and maintenance activities, with higher construction material costs and expectations of further price increases linked to the conflict in the Middle East. Spending on general insurance, including motor and home insurance, also increased over the year, while spending on religious and professional services declined. The data indicate that many households are maintaining key insurance covers despite cost-of-living pressures, which may be relevant for monitoring lapse rates, underinsurance, and shifts to higher excesses or reduced benefits.

Personal goods spending rose 0.7% in March, the third consecutive monthly increase. Over the year, the strongest growth was in toys and game retailing, pharmaceuticals, cosmetics, department stores, and clothing. Spending on footwear and entertainment media fell over the same period. Spending on household goods increased 0.8% in March and 6.7% over the year. Motor vehicle parts, tyres and motor vehicle retailing were key contributors. NAB said year-on-year growth in motor vehicle retailing accelerated from February, potentially reflecting an increase in electric vehicle purchases following the fuel price rise. A gradual shift in the vehicle fleet toward electric models may affect motor insurance portfolios, repair costs, and claims severity. Continued spending on construction and maintenance services also points to ongoing work in the property and trades sectors, with implications for sums insured, construction-related liability, and claims activity across personal and commercial lines.

NAB’s separate Monthly Business Survey for March reported a marked fall in business confidence, while business conditions remained positive overall. The survey showed business confidence declining 29 points to –29 index points. Business conditions eased by one point to +6 index points, slightly below their long-run average. NAB head of Australian economics Gareth Spence said the gap between confidence and conditions shows how quickly sentiment can adjust in response to global events. “The outbreak of the conflict in the Middle East saw business confidence fall 29 points to minus 29 index points, the second largest monthly fall in the survey’s history, with falls of this magnitude previously only seen in the GFC and the onset of COVID,” Spence said.

Spence added: “Business conditions fell only one point to six index points in March, reflecting that while the global news backdrop has impacted sentiment, it is still early days in terms of the flow through to activity. Resilience in business conditions also highlights that the economy had carried a healthy level of momentum heading into the unfolding shock.” Forward orders fell six points to –1 index point, reversing gains made earlier in 2026 and indicating increased caution among firms. Capacity utilisation rose to 83.1% and remained above its long-run average, suggesting that many businesses continue to operate at relatively high levels of resource use.

NAB reported that cost and price indicators moved higher in response to the global backdrop. On a quarterly basis, purchase cost growth more than doubled to 3%, while product price growth rose to 1.1%. “The forward orders measure fell six points to minus one index point, erasing the gains made so far through 2026 and possibly reflecting rising uncertainty. The impact on measures of costs and prices has been immediately obvious, with purchase cost growth in quarterly terms more than doubling to 3% and product price growth rising to 1.1%,” Spence said.

Business confidence is now negative across all states. Business conditions remain positive in most regions, with Western Australia and South Australia reporting improvements in March, while Victoria recorded the largest decline. The combination of higher input costs, weaker business confidence, and elevated capacity utilisation may affect premium affordability, demand for cover, and corporate risk management decisions. If cost-of-living and geopolitical pressures persist, insurers may face a more cautious environment among households and businesses, with potential effects on policy retention, coverage levels, and claims frequency and severity through the remainder of 2026.