As the use of technology continues to expand through every layer of society, it’s become increasingly evident that the importance of cyber insurance simply isn’t understood well enough across Australia, particularly at a personal level.

“The truth is that most of Australia isn’t properly insured against cyber threats at the moment,” says Jeff Gonlin, Head of Product Development and Underwriting at Emergence Insurance. “Plenty of businesses still haven’t got their heads around it, so how are individuals meant to if there isn’t that broader cultural awareness?”

For Troy Filipcevic, CEO and Founder of Emergence Insurance, raising awareness of the importance of personal cyber insurance for families remains a critical day-today concern.

“I think there’s still an attitude of ‘it won’t happen to me’ extant in the community,” says Filipcevic. “People think that their antivirus program and a fi rewall will make them immune to being hacked. Fortunately, families are starting to become aware of cyber SECTOR FOCUS: CYBER INSURANCE risks in the household, but it’s still a big issue that we encounter on a daily basis.”

Gonlin agrees. “Practically every household needs cyber insurance, but there’s a perception that everyone has gotten along fi ne up to this point – so why start now?” says Gonlin. “The truth is a bit di erent – cybercrime is on the rise, and families are increasingly exposed as they have more and more devices in their homes.”

“We wanted something holistic that could cover multiple exposures that differed from ordinary business coverage” Troy Filipcevic, Emergence Insurance

Families, Gonlin notes, are not merely adopting technology – they’re actively relying on it to help run their lives. During 2016–17, the average Australian home had six smart devices1 . In 2019, this fi gure nearly tripled, rising to 172 .

“That number is expected to grow to 37 by 2023,” says Gonlin. “That’s more than some small businesses might have. Count the number of smart or connected digital devices you’ve got in your home. Who manages them?”

It’s not just down to smartphones, laptops and home computers, either, notes Filipcevic. “Pretty much every home appliance is becoming ‘smart’ – the Internet of Things has spread across devices like TVs, fridges, radios and home security systems, just to name a few,” says Filipcevic. “Their protection against hackers or malware isn’t created equal, either; the more devices you have attached to the internet in your home, the more vulnerabilities you have.”

Gonlin also points to the increased number of cybersecurity risks caused by the COVID-19 pandemic.

“The pandemic has really reinforced and expedited trends that were already established,” says Gonlin. “People are living more of their lives online – buying more, working, schooling, sharing more and, with every click, risking more.”

So how can insurance be effectively secured in the wake of all this additional exposure? The truth is that there hasn’t been a specifi c product catering for these types of exposures in Australia. Well, until now, that is – as of August 2020, Emergence have launched Australia’s fi rst stand-alone personal and family cyber insurance product.

“It’s not just about tech support when the home computer gets hacked,” says Filipcevic. “It’s also about providing help with the emotional fallout that can occur in the wake of incidents like cyberattacks, cyberbullying or cyberstalking.”

“Delving into personal cyber is just an extension of what Emergence has been doing from the start –making cyber understandable, affordable and accessible,” says Gonlin. “When it comes to cyber risks, there’s crime, identity theft, threats to reputation and the economic costs that arise from time required to rectify any damage. We developed our personal product to respond to each and every one of these threats.”

“It’s a real game-changer,” says Filipcevic with pride. “We’d looked at personal coverage products in other markets, and frankly we weren’t very impressed. We wanted something holistic that could cover multiple exposures that differed from ordinary business coverage.” “The limits needed to be meaningful,” agrees Gonlin. “In other markets, we were seeing simple cash payment solutions, but that doesn’t necessarily provide affected families with all of the tools they need. We also wanted to make sure that there was a risk management component in order to help ward off events before they occur.”

Accordingly, Emergence’s product includes:

• Cyber Event Cover: response costs for technical hazards such as hacking, denial of service, cyber extortion and cyber espionage

• Cyberbullying Cover: provides payment of an additional benefit, including attending critical guidance sessions and for a cybersecurity coach and forensic IT investigator

• Cyberstalking Cover: response costs for (anti-) social threats, including legal costs or a cybersecurity coach

• Personal Crime Cover: payment of a personal fi nancial loss due to cyber theft, sim-jacking and cryptojacking

• Identify Theft Cover: payment of identity theft response costs, including reporting and re-establishing identity and records

• Reputation Cover: pays costs incurred in connection with both cyber harassment and harmful publication

• Wage Replacement Benefit: covers economic fallout from time required to sort out issues that result in the wake of cybercrime, whether identity theft, cyber theft or cyberstalking

Both men believe that brokers have a critical role to play in educating families about the importance of cyber insurance – arguably more than ever before. Accordingly, they’re keen to aid with the process.

“I always like to say that we’re a company who’s big on broker education – we just happen to sell insurance,” chuckles Filipcevic. “Realistically, though, brokers need to be across so many different tools, products and industries – so we want to make them as comfortable as possible with cyber insurance products and the need for them so that they can be professionally and effectively discussed with clients.”

Considerable time has been spent on debunking cyber insurance myths for brokers and clients alike, Filipcevic notes.

“I think since Emergence was founded, the media has tended to focus on celebrities who are victims of hacks, or large-scale data breaches,” says Filipcevic. “That’s sometimes made it tricky to explain to individuals how it might affect them.”

Ultimately, though, both men feel that personal cyber insurance represents a “huge” opportunity for brokers to engage with new and existing clients alike. “Brokers are the ones equipped to engage with the market,” says Filipcevic.

“Brokers have personal books of business. This product is the perfect value-add for those clients. There’s no reason why enterprising brokers can’t be the fi rst to identify broader opportunities for individual or family accounts. We are in a position to support their endeavours.”

Of course, with new products comes pressure to deliver as well. Filipcevic and his team at Emergence are keenly aware of their need to step up during these challenging times.

“Cybercrime is on the rise, and families are increasingly exposed as they have more and more devices in their homes” Jeff Gonlin, Emergence Insurance

“There’s a lot of short-term economic pressure at the moment, but cyber spend is still critical,” says Filipcevic. “Brokers sometimes have a tough time even getting the airtime – particularly with new products – so we want to do everything we can to help them get their foot in the door with clients. In practical terms, that means the pressure is on us to ensure that we’re delivering real value for every dollar the client spends – whether that means providing brokers with pre-sale support or supporting insureds with aftercare in the event of an incident.”

As Emergence looks towards the future, Gonlin believes that the environment is going to continue to evolve rapidly, and personal cyber insurance will become increasingly important.

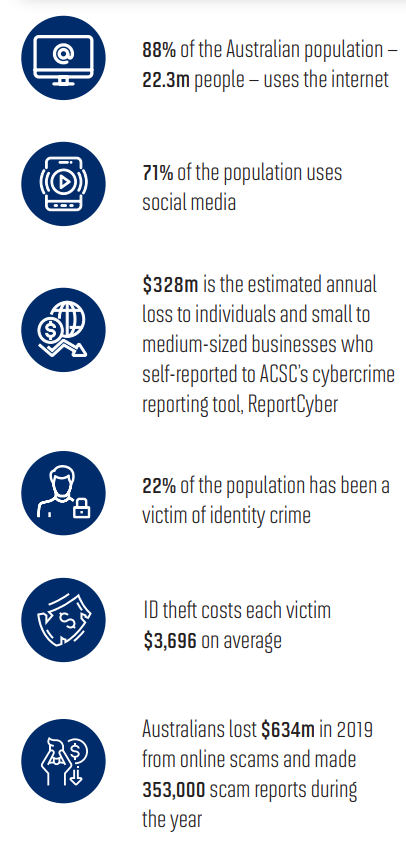

“At the moment, 22% of the Australian population has been a victim of some kind of identity theft,” says Gonlin. “It’s a far higher likelihood than experiencing a break-in or having your car stolen – so why haven’t we seen the insurance solutions until now? That’s something Emergence very much looks forward to addressing.”