.jpg)

A maelstrom of social media, high stakeholder expectations and public discontent is driving the frequency and severity of reputational crises – and the insurance industry itself is not exempt

Due in no small part to the power of social media, both individuals annd organisations are increasingly held to account for their actions by the public in today's world.

Now that the average consumer has a smartphone in their pocket, they also have a platform with which to share their grievances with the world – which can be bad news when it comes to companies’ public relations. In an age when an incident can quickly become a viral sensation, organisations are finally waking up to the reality that a reputational crisis is always just a tweet away.

Alongside traditional operational risks such as mis-selling, poor product design and failure to protect customer rights or data, businesses today face wider-reaching cultural and societal challenges, too.

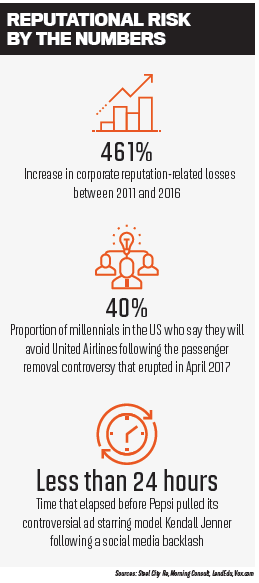

This was driven home in 2017, during which time a number of major brand names encountered significant reputational crises. Pepsi was forced to pull a commercial starring model Kendall Jenner after it was accused of trivialising the Black Lives Matter movement. United Airlines went viral for all the wrong reasons after a video emerged of a passenger being dragged off an overbooked flight. Perhaps most notably, Hollywood heavyweight film studio The Weinstein Company became embroiled in what has since become a major social movement when dozens of sexual assault and misconduct accusations emerged against its now-disgraced co-founder, Harvey Weinstein.

The prospect of a reputational crisis today means more than just bad PR, though – it is likely to impact a company’s bottom line. In the five years leading up to 2016, reputational insurer Steel City Re found a 461% increase in corporate reputation-related losses.

The growth in the overall frequency and severity of reputational losses has been driven by three factors, according to Steel City Re CEO Dr Nir Kossovsky. The increasingly high expectations of stakeholders (resulting in a progressively low tolerance of failure), the rise in the use and ability of social media to spread both true and false stories, and a growing sense of anger and disappointment among the general populace are all creating a breeding ground for reputational disasters.

The growth in the overall frequency and severity of reputational losses has been driven by three factors, according to Steel City Re CEO Dr Nir Kossovsky. The increasingly high expectations of stakeholders (resulting in a progressively low tolerance of failure), the rise in the use and ability of social media to spread both true and false stories, and a growing sense of anger and disappointment among the general populace are all creating a breeding ground for reputational disasters.

Social media in particular has the power to greatly accelerate change, and it’s being used as a “powerful weapon against companies, industries and individuals when they become targets,” Kossovsky says.

Insurance companies themselves have not been exempt from being drawn into controversy. Following the February school shooting in the US that left 17 people dead, a number of corporations cut ties with the gun lobbying group the National Rifle Association [NRA], including insurance giants Chubb and Lockton.

Chubb revealed it would stop underwriting NRA Carry Guard, a branded insurance policy for NRA gun owners, though it said the decision was made months before the Parkland shooting. Lockton followed with an announcement that it would no longer sell products with an NRA endorsement.

"Lockton Affinity has notified the NRA that it will discontinue providing brokerage services for NRA-endorsed insurance programs under the terms of its contract," the broker said in a tweet.

According to Kossovsky, companies are acting now because “the fear of economic harm by angry or disappointed stakeholders – what we call reputational risk – is much greater.

“Earlier this year, the top reputation risk was allegations of unethical and inappropriate executive behaviour that gained prominence through #MeToo," Kossovsky says. “At this particular moment, it is the NRA. For corporate leaders responsible for protecting the assets of a firm, the lesson is that reputational risk – because it is linked to expectations and is triggered by disappointment – can emerge suddenly with shifts in culture.”

As technology continues to advance at rapid speed, cyberattacks and cybercrime can also present reputational risks for organisations. As a result, some insurance carriers now offer coverage for financial losses suffered as a result of cybercrime. Responding to a cyberattack can be costly and time-consuming, which can result in a serious knock-on effect on a business’s bottom line.

“Reputation harm insurance not only helps cover the cost of a breach, but also provides funds to cover the temporary loss of income while an organisation recovers,” says Jeremy Barnett, senior vice president of marketing at NAS Insurance Services.

The message to businesses is clear: In today’s world, a reputational crisis can mean more than just some bad publicity. According to Kossovsky, economic damage from a reputational crisis “can be as great as the damage from a sudden tornado.”