The most consequential pattern in IAG’s Resilient Futures Report, published June 17, 2026, is not that Australians are unaware of risk – it is that awareness is failing to convert into action. Survey data from more than 2,400 consumers and small businesses show that 67% of consumers and 64% of SMEs experienced at least one significant disruption in the past 12 months, yet many of those same respondents report that financial pressure, competing demands, and uncertainty about which steps matter most are preventing them from responding substantively.

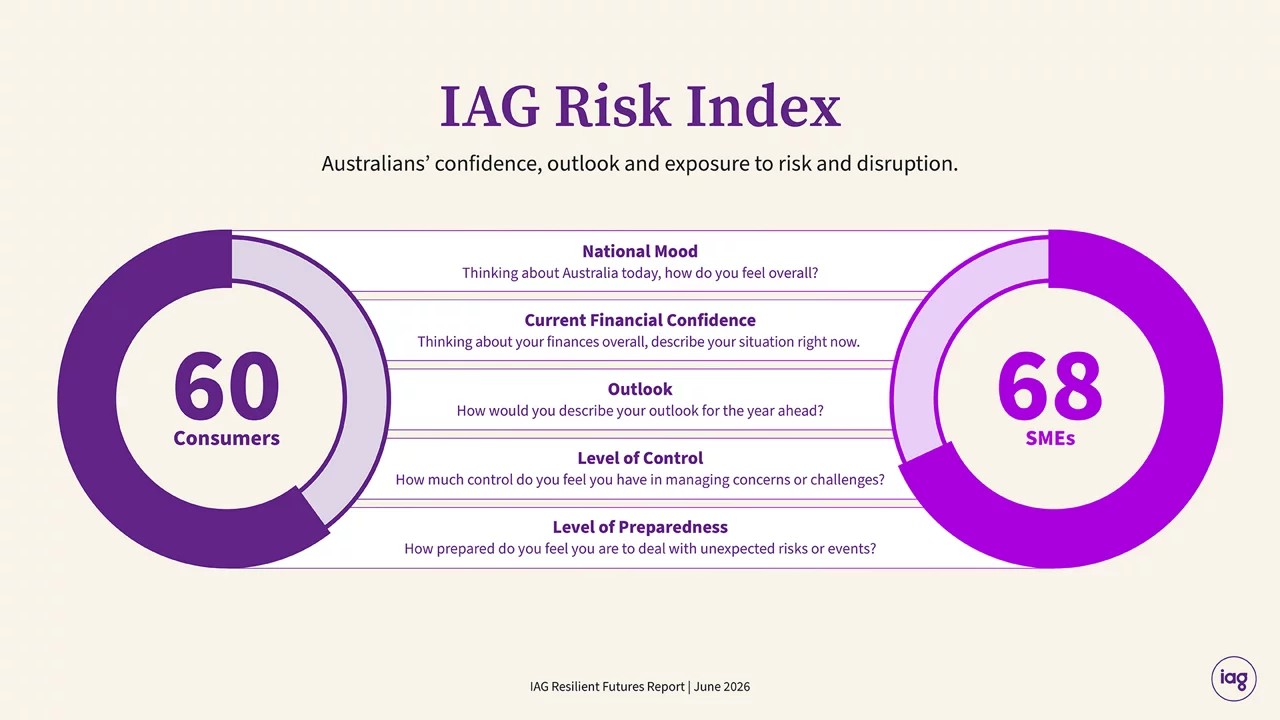

That combination – high exposure, constrained capacity to respond – describes the conditions under which coverage lapses, sums insured go unreviewed, and claims costs exceed what policyholders anticipated. It is the thread that runs through every finding in the report, from the generational data to the regional breakdown to the SME climate exposure numbers. The report introduces the IAG Risk Index alongside these findings: a composite measure scored out of 100 that will track sentiment and readiness over time across five dimensions: national mood, financial confidence, future outlook, level of control, and level of preparedness.

IAG managing director and CEO Nick Hawkins framed the gap as something requiring a structural response. “Risk is no longer something Australians think about hypothetically, it is something many are experiencing in real time. The IAG Risk Index shows that while awareness of risk is high, confidence and preparedness are not always keeping pace. Strengthening Australia’s resilience means helping people better anticipate disruption, take practical steps to prepare, and recover more quickly when setbacks occur,” he said.

Cost-of-living pressure is the primary mechanism driving that inaction. It ranked as the dominant concern across both consumer and SME cohorts, directly constraining the capacity to maintain adequate protection. Hawkins noted that global macroeconomic conditions – particularly those linked to the conflict in the Middle East – are compounding pressure that was already acute for younger households and smaller businesses.

The generational data contains the report’s most counterintuitive finding, and the one with the most direct implications for underwriting and distribution. Younger Australians – particularly Gen Z and Millennials – are the most optimistic cohort in the survey. They are also the most financially stretched and, by extension, the most likely to be making coverage decisions driven by short-term cost rather than long-term risk exposure.

This is the same awareness-action gap that defines the report’s headline finding, expressed at the cohort level where it has the sharpest commercial consequence. Close to half of Millennials are servicing debt to cover current living costs. Nearly half have deferred medical appointments due to financial pressure. Nearly two-thirds of Gen Z respondents have taken on additional paid work to supplement income. These are households managing cash flow week to week, where the cost of maintaining coverage, reviewing sums insured, or increasing policy limits is competing directly with immediate expenses.

Baby Boomers sit at the other end of both measures. Their optimism is the lowest of any generation – 46.1% against a national average of 56.7% – yet they are the cohort most likely to have savings buffers in place, to have put money aside for unexpected costs, and to have kept insurance coverage under active review. The preparedness behaviours most associated with adequate protection are concentrated precisely where financial pressure is lowest.

For brokers and insurers, the implication is direct: the customers least likely to proactively engage with their coverage are those whose financial circumstances most warrant it. Reaching younger policyholders at renewal, and making the case for coverage adequacy in a cost-constrained environment, is the distribution challenge this data surfaces most clearly – and one that is likely to intensify if cost-of-living pressure persists.

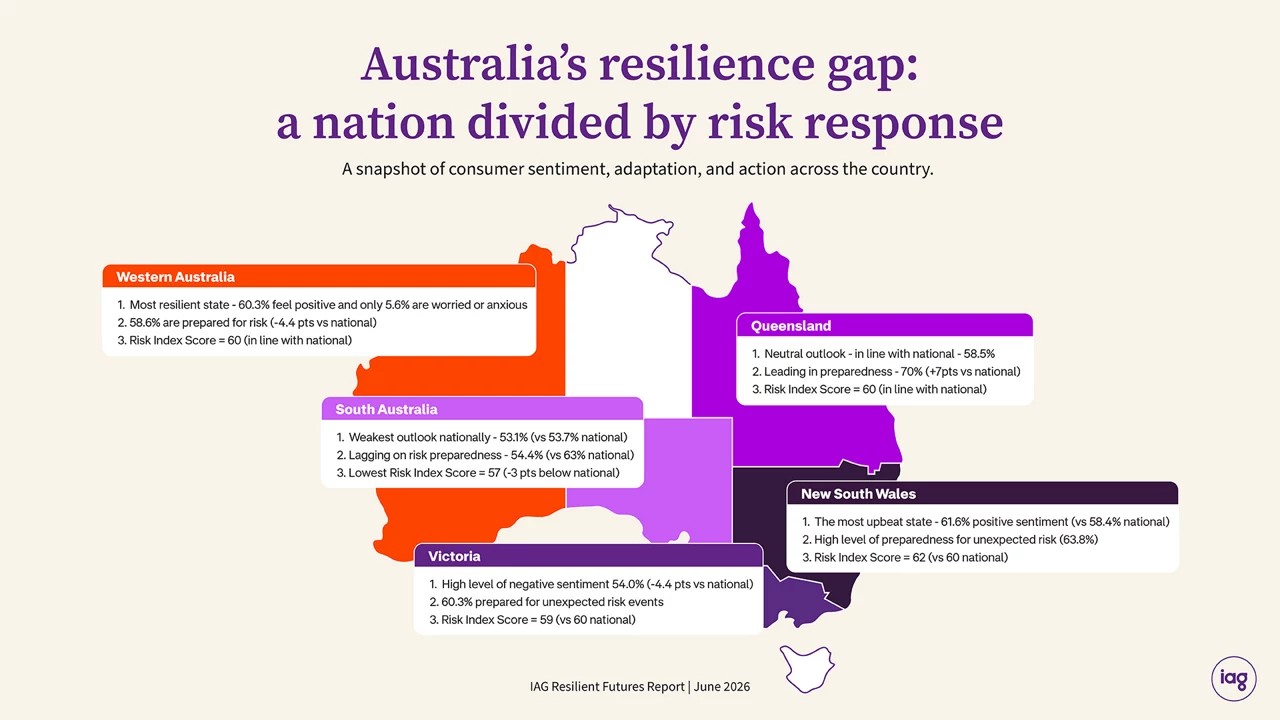

The state-level data extends the same pattern into geography, with some states presenting combinations of elevated peril exposure and below-average preparedness that carry specific relevance for underwriters and claims teams. Victoria is the most strained market in the survey. Just 54% of Victorian consumers reported a positive outlook, well below the national figure of 58.4%, and anxiety levels are running at nearly 1.5 times the national average. Nearly one in four Victorians reported bushfire impact in the past 12 months against 20.6% nationally, more than one in eight reported a crime or vandalism incident, and just 60.3% feel prepared for unexpected risks – below the national rate of 62.8%. Elevated peril frequency combined with below-average preparedness is a profile with direct implications for claims provisioning.

South Australia compounds weak sentiment with specific climate exposure. The state recorded the lowest personal outlook score nationally at 53.1%, and heatwave concern is the highest of any state at 48.8%, against a national figure of 38%. Fewer than half of South Australian respondents felt confident their home was adequately protected against extreme weather. For property underwriters, that gap between perceived exposure and felt protection is a pricing and adequacy signal. Western Australia recorded the highest positivity at 60.3% and the lowest negative sentiment of any state at 22%. The report notes, however, that lower perceived climate risk in WA appears to be reducing the impetus for households to prepare – a dynamic where confidence may be generating its own form of exposure when conditions deteriorate.

New South Wales and Queensland present stronger profiles on both sentiment and preparedness, but each contains a finding worth noting. In NSW, 55.8% of residents are already factoring climate risk into property and location decisions – a behavioural shift that may be driving demand for climate-adjusted coverage in the state’s property market. In Queensland, 70% of residents reported being ready to tackle unexpected risks – the highest of any state – suggesting a market where demand for risk mitigation products and services may be more developed than elsewhere.

The commercial picture extends the report’s central argument into business lines, where the gap between disruption frequency and structural preparedness is creating conditions for underinsurance at reinstatement. Nearly half of SMEs – 48% – reported extreme weather impact in the past 12 months. Yet businesses are not consistently maintaining backup suppliers, formalizing continuity plans, or keeping insurance coverage under regular review – the three measures most directly linked to containing loss severity and reducing claims complexity when weather events do occur. For commercial lines underwriters and brokers, the consequence is specific: SMEs absorbing repeated climate shocks without those protections in place are more likely to face reinstatement costs that exceed their coverage, and less likely to recover operationally within the timeframes their policies assume.

The financial scale of weather-related underpreparedness is visible in personal lines claims data, and it reinforces the same argument on the consumer side. NRMA Insurance NSW figures covering the period since 2016, published in the NRMA Insurance Wild Weather Tracker on June 11, 2026, show the average bushfire claim runs 69% higher than flood claims – the next most costly weather category. More than 9,000 bushfire claims were lodged over the past decade, with close to 8,000 tied to the 2019-20 Black Summer fires.

Current preparedness levels suggest that exposure is not diminishing. The Wild Weather Tracker found 42% of Australians do not feel prepared for bushfires, with an emerging El Niño pattern expected to drive elevated fire conditions through winter. Just 6% of Australians said they typically think about bushfire preparation outside the traditional summer season – a behavioural gap that has a direct relationship to both property loss frequency and the scale of individual claims.

NRMA Insurance meteorologist Peter Chan said the assumption that bushfire risk is confined to summer is itself contributing to the preparedness shortfall. “Australia's bushfire season varies by region and typically runs through the hotter months in southern parts of Australia, but fires can occur at any time of the year when weather and fuel conditions allow, and this winter is a clear reminder of that,” Chan said. NRMA Insurance property assessor Judi Hindson, drawing on 37 years of post-event assessments, identified the mechanism of bushfire damage as something policyholders consistently underestimate. “Bushfires can be unpredictable and fast moving, and we often see communities caught by surprise. It’s not flames, but embers, that can cause most of the damage,” Hindson said.

The IAG Risk Index launches at a moment when cost pressure is actively working against the preparedness behaviours the index is designed to measure. Its baseline reading establishes that the awareness-action gap is wide, that it is unevenly distributed across generations and geographies, and that it is being driven by financial constraints rather than indifference to risk. Whether subsequent editions show that gap narrowing as economic conditions ease – or widening further as climate events accumulate and household budgets remain under pressure – will be directly relevant to insurers modelling future exposure, pricing personal and commercial lines risk, and identifying where product and distribution interventions are most needed. The index gives the industry a consistent measure against which to track those shifts over time. Hawkins said the index is intended to serve that broader function. “Australia's future prosperity depends on how well we anticipate and recover from disruption. The Resilient Futures Report and IAG Risk Index give us a picture of how Australians are feeling about risk and where protection gaps remain, so we can act earlier and more effectively,” he said.