New Zealand’s framework for managing natural hazard risk is fragmented, under-resourced, and falling behind the pace at which those risks are growing – and without structural reform, the consequences will extend to insurance availability, public finances, and long-term economic stability.

That is the central finding of a report published by IAG New Zealand.

The document, titled A Long-Term Approach to Natural Hazard Risk Reduction, was developed through consultation with more than 50 practitioners and experts across engineering, infrastructure, finance, government, and academia, alongside a review of more than 80 reports from government agencies, industry bodies, and research institutions. Over the 15 years to 2026, natural hazards have cost New Zealand at least $64 billion in direct losses, which works out to more than $4.2 billion annually. The report notes that around 95% of that expenditure was absorbed by response and recovery efforts, leaving a fraction available for measures intended to reduce future harm. IAG New Zealand chief executive Phil Gibson (pictured) said the current system was not structured to change that pattern on its own. “Our country needs councils, communities, businesses, and homeowners to reduce the natural hazard risk they face. But New Zealand does not yet have a complete or coherent approach to enable this, and we want to help,” Gibson said.

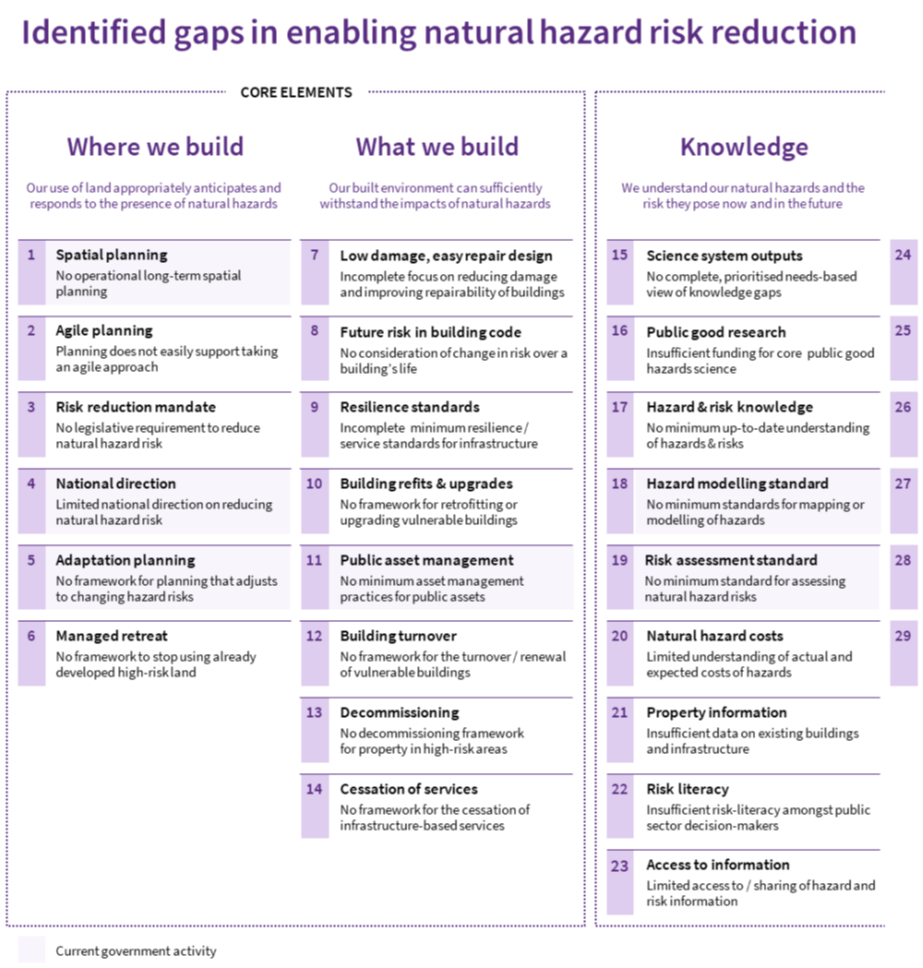

The report organises its findings around five interconnected areas where it says New Zealand’s approach falls short. The first concerns land use and construction standards. The report finds that existing planning rules do not consistently account for where development is safe or how buildings and infrastructure should be designed to withstand hazard events. It describes the planning system as lacking the thresholds and adaptive tools needed to keep pace with changing conditions.

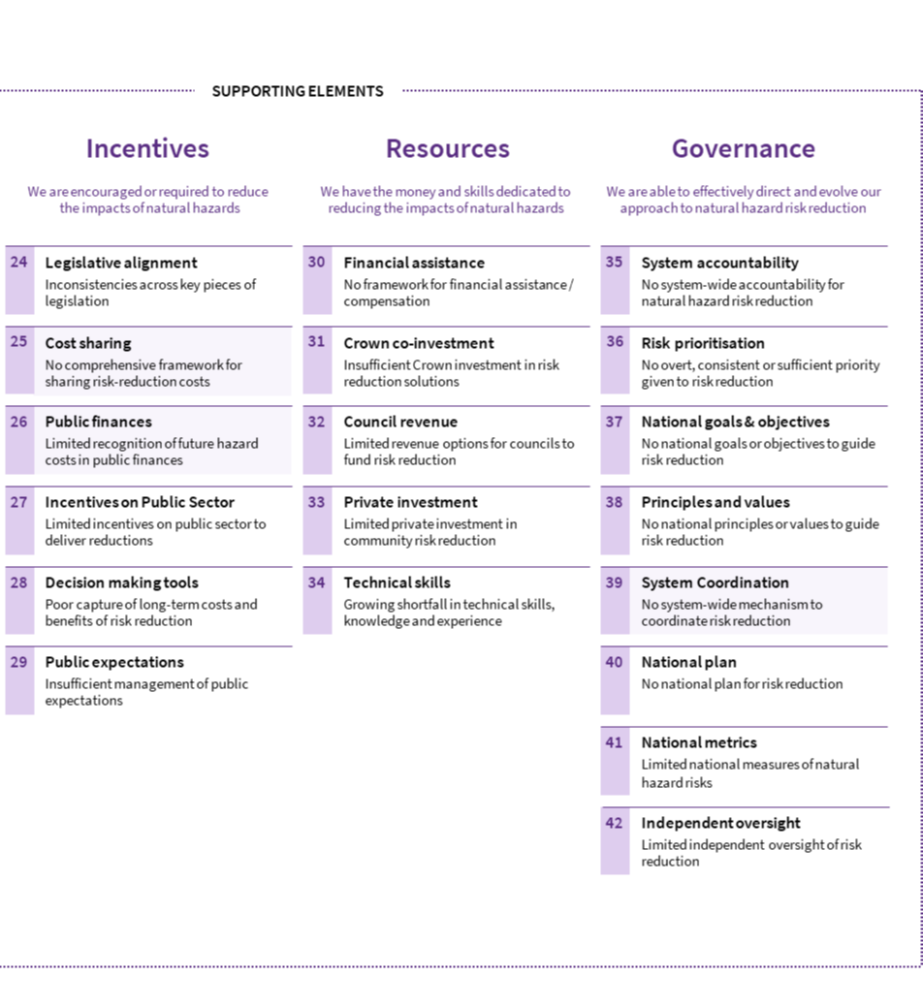

The second area is information. Hazard modelling is inconsistent across regions, data on physical exposure and vulnerability is patchy, and the report finds that many decision-makers lack the risk literacy needed to apply available information effectively. Third, the report examines financial incentives. It finds there is no overarching framework that determines who bears the cost of risk reduction, and that public finances do not adequately account for the future liabilities that natural hazards represent. At the same time, mechanisms to reward proactive investment in resilience remain limited.

Fourth, the report looks at capacity – both financial and human. Local councils face constrained revenue options and there is no scalable model for cost-sharing with central government or the private sector. The report also identifies a shortage of technical specialists needed to support risk reduction work. The fifth area is governance. The report concludes that no single body holds clear system-wide responsibility for natural hazard risk reduction, there are no nationally agreed objectives, and progress is not consistently tracked or reported. Gibson said the aggregate effect of these weaknesses was significant. “This problem is solvable, but there are pieces of the puzzle that must be added to our current approach if we are to do a better job of reducing risk. This report distils the insights of over fifty New Zealand experts and practitioners to put those pieces on the table,” Gibson said.

The report draws a direct line between the state of New Zealand’s risk management framework and the long-term functioning of the insurance market. The report argues that without structural improvement, the frequency and severity of disaster events will increase pressure on insurance availability and affordability. Gibson framed this as central to IAG’s rationale for publishing the research. “Our aim is to ensure that growing natural hazard risk does not become a chronic problem for New Zealand. If risk is well managed, the cost and harm it can create will be kept in check, with flow-on benefits for the cost and availability of insurance,” Gibson said. The report also references international evidence suggesting that well-structured risk reduction investment can generate returns of four to six dollars for every dollar spent.

Rather than outlining a single policy prescription, the report sets out a possible 15-year pathway organised into four phases. The immediate phase centres on putting governance in place to develop and oversee a national plan. The following four years would focus on foundational work: clearer planning rules, investment in protective infrastructure, improved hazard data, and more defined expectations around cost-sharing between central government, local government, and property owners. The middle phase, spanning years five to 10, would extend into legislative alignment, stronger financial incentives, broader funding mechanisms, and workforce development. The final phase, beyond the 10-year mark, addresses large-scale adaptation – including frameworks that could support the eventual withdrawal of development from areas where risk becomes unmanageable.

The report nominates several steps as immediate priorities, among them establishing political ownership of risk reduction at a senior government level, developing a national strategy with defined objectives and independent oversight, and updating the National Policy Statement on Natural Hazards to give councils clearer guidance ahead of broader resource management reforms. Gibson said the case for acting sooner rather than later was straightforward. “New Zealand has choices in how we fill the gaps and needs identified in this report. But delay, half-measures, and political caution will cost us in the long run. IAG is committed to working alongside government, councils, iwi, business, and communities to shift New Zealand from a place of reaction to one of resilience,” Gibson said.