The Australian Prudential Regulation Authority’s (APRA) first stress test of links between banks and superannuation didn’t model insurance at all. But default death and disability cover delivered through superannuation accounts is regulated under a framework that assumes a degree of stability in member balances and contributions, and the liquidity behaviour APRA’s stress test modelled in those same funds runs directly through that assumption.

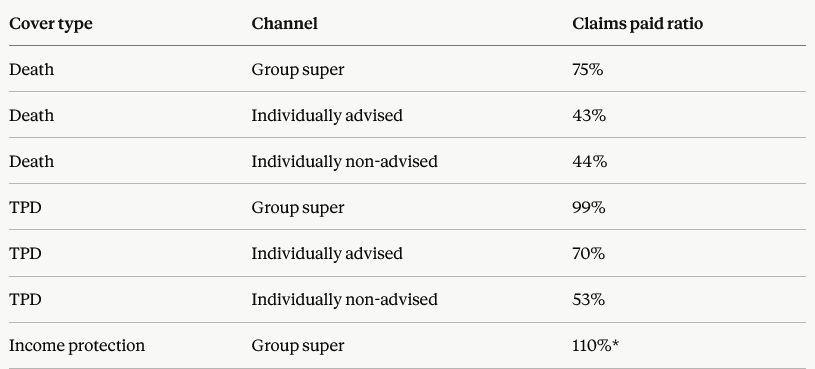

The Life Insurance Claims and Disputes Statistics released jointly by APRA and the Australian Securities and Investments Commission (ASIC), covering the 12 months to Dec. 31, 2025, show claims behaviour diverging sharply between distribution channels. Group super death cover recorded a 75% claims paid ratio and a 98% admittance rate, against 43% to 44% claims paid ratios for individually advised and non-advised retail death cover. Group super total and permanent disability (TPD) cover reached a 99% claims paid ratio, compared with 70% for individually advised TPD and 53% for non-advised. Group super income protection recorded 110%, a figure the data attributes to the ongoing nature of income benefit payments rather than a single claim event.

*Reflects ongoing benefit payments rather than a single lump-sum event.

This is not unregulated territory. APRA’s Prudential Standard SPS 250 Insurance in Superannuation, supported by Prudential Practice Guide SPG 250, requires superannuation trustees to maintain a sound insurance management framework and to act in members’ best financial interests when selecting and monitoring insurance arrangements. Prudential Practice Guide LPG 270 Group Insurance Arrangements sets out parallel expectations for insurers writing group business through super funds, covering risk identification, tender processes, and data management. Both remain current; SPG 250 was finalised in 2021, and LPG 270 has not since been replaced. The question worth asking is not whether a framework exists, but whether it was built with an assumption like the one the SRST just tested.

APRA’s “System Risk Stress Test” information paper, published June 30, 2026, modelled four major banks and six large superannuation funds against a scenario requiring $174 billion in cumulative liquidity, equal to just under 16% of net assets, met largely through sales of offshore listed shares. The exercise also modelled a sharp increase in member switching into cash and a marked rise in lump-sum withdrawals among members past preservation age.

Insurance arrangements within those funds sat outside the SRST’s scope, and APRA did not measure any effect on group cover. What the test does establish is that the funds responsible for collecting group insurance premiums from member contributions and account balances, under the SPS 250 framework, are the same funds modelled under that liquidity pressure. Group insurance premiums are typically deducted from those balances and contributions, which means a scenario severe enough to require $174 billion in fund-level liquidity is also a scenario that would test the funding mechanism the existing insurance-in-super framework assumes will keep working.

A primary group life writer should check whether its pricing and lapse assumptions, and the data-quality and risk-identification practices LPG 270 already expects of it, account for the kind of contribution slowdown and balance erosion the SRST modelled. A reinsurer sitting behind concentrated group books carries a sharper version of the same question: with TAL, AIA Australia, and MetLife together writing the large majority of group super death cover premium, a liquidity event severe enough to disrupt fund administration at scale would hit a treaty book concentrated in three writers harder than one spread across many. A fund’s risk committee has an obligation under SPS 250 to keep its insurance management framework current, which raises the question of whether that framework has been tested against simultaneous liquidity stress and member switching at the severity the SRST modelled, rather than against each in isolation.

None of this means APRA’s existing framework has failed, or that insurers are non-compliant. SPS 250 and LPG 270 were not designed with a scenario like the SRST’s in mind, because that scenario did not exist as a tested benchmark until June 30, 2026. The practical question for anyone managing group insurance risk through superannuation is whether premium-funding arrangements between insurers and trustees, built under that existing framework, would hold up if member balances fell sharply and switching activity accelerated at the same time, the precise combination the SRST modelled for the funds themselves. That is worth testing now, while it remains a hypothetical exercise rather than a live one.