The CEO of an award-winning service provider says he’s noticed a worrying disconnect in the industry when it comes to business interruption insurance – and it could lead to serious issues for clients.

Speaking to Insurance Business, LMI Group’s CEO Steve Manning said he spotted the concerning trend after conducting a number of training sessions which focussed specifically on business interruption.

In the sessions, which were attended by brokers and insurers, one particular issue kept raising its head – that is, whether uninsured working expenses really need to be listed on the policy schedule.

“Insurers were concerned that they are often not listed, and many brokers were unaware of the need to, with many simply leaving them out,” said Manning.

While there was some uncertainty around the issue, Manning said there’s very good reason to disclose the additional information.

“The sad truth of the matter is that the oversight or decision to not include uninsured working expenses can leave a client significantly short changed,” said Manning.

“It can also create substantial cashflow issues for them at the worst possible time, often leading to the insured business failing, or leading to a professional indemnity claim for the advisor.”

This is because uninsured working expenses are used by insurers to calculate the insured gross profit in a business interruption policy.

The Industrial Special Risk ‘ISR’ policy, for example, sets out exactly how the Rate of Gross Profit is to be calculated – that is;

“GROSS PROFIT: the amount by which:

(a) The sum of the Turnover and the amount of the Closing Stock and Work in Progress shall exceed

(b) The sum of the amount of the Opening Stock and Work in Progress and the amount of the Uninsured Working Expenses as set out in the Schedule.

Looking at it as a formula, the way to calculate the Insured Gross Profit would be:

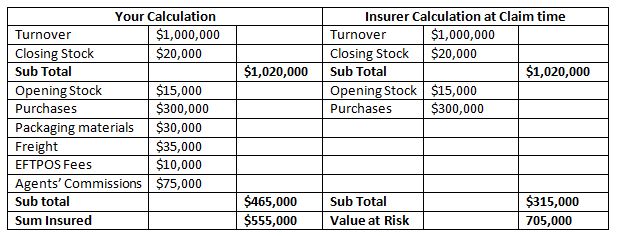

Rate of Gross Profit = (Turnover + Closing Stock) – (Opening Stock + Purchases + LISTED Uninsured working expenses)

If the uninsured working expenses are not listed, it can throw off the entire calculation. To demonstrate the risk, Manning pointed to a simple sum insured/declared value comparison calculation.

“By failing to list the uninsured working expenses, it has resulted in significantly different figures at the time of the claim, compared to the original declared value calculation,” said Manning. “This becomes concerning when the test for adequacy is brought into operation at the time a claim under the policy is made.”

While the base ISR policy has 100% co-insurance on Section 2 – Consequential Loss, Manning allowed 80% co-insurance as many ISR’s have been endorsed to this effect.

(Declared Value / 80% of the Value at Risk) X 100 = Percentage of Claim Paid.

Using the figures in the earlier example, this would calculate to be (420,000 ÷ 80% of 705,000) x 100 = 74.46%

“As a result, in the event our client suffers an interruption, any claim would be reduced proportionately,” said Manning. “The result - only 74.33% of any claim will be paid by the insurer, with the remaining 25.67% to be carried by the insured.”

Incredibly, the calculations could be skewed even more dramatically if factors such as business trend, and indemnity periods were taken into consideration.

In simple terms, Manning says including uninsured working expenses creates contract certainty – which is beneficial to everyone in the insurance value chain.

“With any contract, having contract certainty ensures the operation of the contract is much clearer when it needs to be relied on,” he said. “It’s of benefit to both the insured and insurer and, of course, makes it so much easier for the claims officer, loss adjuster and claims preparer.”

As such, Manning urged all brokers to include uninsured working expenses on their policy schedules.

“It is my strong recommendation to avoid any confusion, save time and have that contract certainty that all uninsured working expenses should be listed on the schedule,” he said.