Tropical Cyclone Alfred generated $1.335 billion in net incurred losses within Australia’s government-backed cyclone reinsurance scheme – the pool’s largest single-event loss since it commenced in July 2022 – as the Australian Reinsurance Pool Corporation’s (ARPC) March 2026 quarterly data, a concluded regulatory monitoring regime, and an ongoing statutory review collectively present the clearest picture yet of what the scheme has delivered, and what remains unresolved. The quarterly statistics report, released by the APRC on July 14, 2026, covers the period ending March 31, 2026, and records $1.53 billion in cumulative net incurred claims across all events since the pool’s inception.

Alfred accounted for 115,992 claims within the pool: home policies contributing $1.108 billion across 107,511 claims, strata adding $150.87 million, and SME $76.49 million. The Insurance Council of Australia (ICA) recorded more than $1.5 billion in total industry insured losses from the event across 132,000 claims, making it the costliest weather event in Australia in 2025. Insured losses from the rare storm were estimated at $2.25 billion Australian dollars, with the majority absorbed by the Cyclone Reinsurance Pool, which is now fully integrated alongside insurers’ reinsurance catastrophe programs. Aon’s April 2025 reinsurance market dynamics report noted that the majority of insured losses would fall to the pool and consequently Alfred will not be a market-changing event for commercial reinsurers – a direct consequence of the pool absorbing concentration risk that would otherwise sit with the global market.

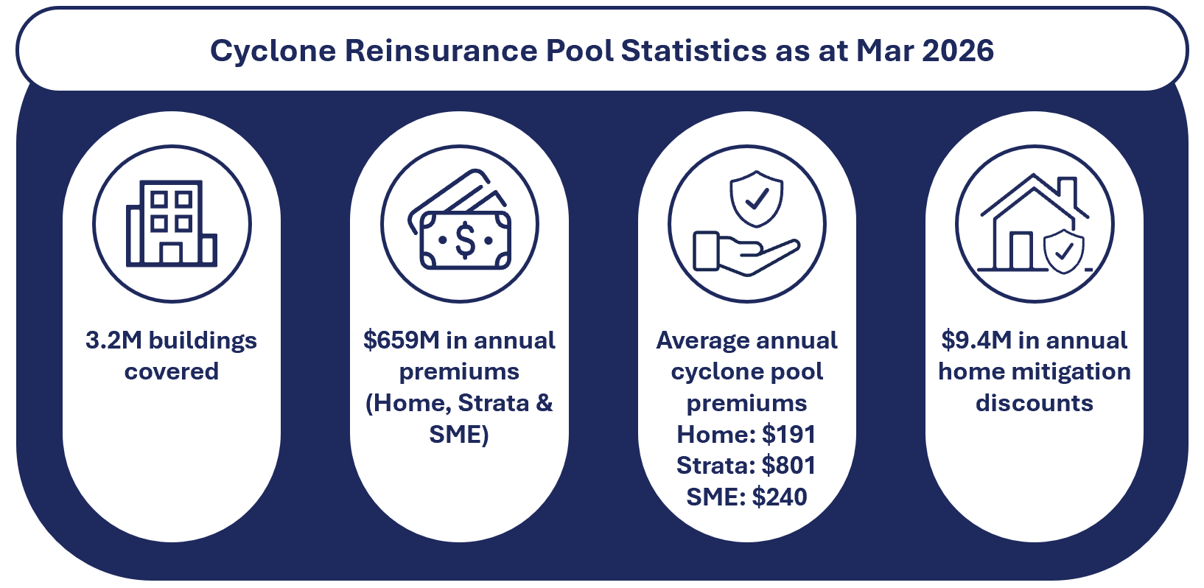

The pool’s cumulative net incurred claims of $1.53 billion against annual premium income of approximately $659 million represent more than two years of premium revenue. The pool is designed to move between accumulated surplus and deficit positions, and ARPC’s 2025 Financial Outlook Report recorded net liabilities of $734 million as of June 30, 2025, with cash and investments at $1.23 billion. ARPC’s actuarial adviser Finity Consulting determined at its September 2025 pricing review that revisions to premium rates were not appropriate to address the deficit. The cyclone pool’s estimated claim and operating costs for 2026-27 are estimated at $636 million, with $637 million in premium estimated to be collected – a margin Finity assessed as adequate.

ARPC chief executive Dr Christopher Wallace said of the updated premium rates: “The updated premium rates ensure the cyclone pool remains financially sustainable and responsive to evolving risks. These rates continue to meet legislative objectives, while the introduction of SME mitigation discounts recognises and rewards proactive risk reduction efforts.” The 2025-26 season added a further estimated $267 million in losses across nine declared events, according to ARPC’s May 2026 season update – a comparatively smaller increment to cumulative totals, with no single event approaching Alfred's scale.

The Australian Competition and Consumer Commission (ACCC) concluded its formal monitoring role over the pool on June 30, 2026, publishing its fifth and final mandatory insurance monitoring report. The assessment provides the most complete independent picture of the pool’s performance to date, covering five years of pricing, cost, and market data. In the first year after insurers joined the pool, average premiums in higher cyclone risk areas had fallen 11% for home insurance, 8% for strata insurance, and 24% for small business insurance. Up to two years after joining, home insurance premiums had dropped 14% and small business insurance had fallen 31% compared to pre-pool prices. Those reductions were durable and concentrated where the pool was designed to deliver.

But the ACCC’s report also confirmed structural shortfalls. No new insurers have entered northern Australian markets, and there has been limited appetite from existing insurers to expand or increase their exposure overall – an outcome at odds with one of the pool’s stated design objectives. The average premium in 2024-25 for home and contents insurance was almost $5,000 in north Western Australia, over $3,500 in the Northern Territory, and more than $3,100 in north Queensland. ACCC Commissioner Anna Brakey said: “While there are clear signs the pool has reduced premiums for policyholders living in areas with higher cyclone risk, other factors mean insurance premiums remain very high for many Australian households, including those in high-risk areas.”

The ACCC also found some insurers are yet to implement a mitigation framework, and the clarity of the information provided to consumers about private mitigation varies. With the ACCC’s oversight role now closed, the statutory review of the Terrorism and Cyclone Insurance Act 2003 is the only remaining formal accountability mechanism. The review – the first since the cyclone pool was established – had submissions close in November 2025 and its findings have not yet been published, according to Treasury’s review register. Wallace said the conclusion of the ACCC’s monitoring role marks a milestone but not an endpoint: “Their monitoring has been important in tracking how the cyclone pool is operating in practice, and in highlighting both the progress made and the areas where continued focus is needed.”

One thread running across multiple consecutive quarterly reports warrants attention from underwriters and brokers active in the strata segment. The persistent decline in reported strata risk counts had previously been attributed to delayed reporting, but ARPC’s 2025 Financial Outlook Report confirmed it reflects something more substantive: a decrease in the number of reinsured risks for Strata and SME is listed among the factors moderating premium growth, alongside improvements in data accuracy reported by insurers and increases in policyholder excesses.

The June 2025 quarterly report attributed a separate decline in SME storm surge coverage proportions to an insurer correcting previously inaccurate historical submissions – a data quality issue distinct from the strata count trend, but a further signal that data completeness and consistency is more varied in the SME and Strata portfolios. For treaty underwriters and cat modellers, the distinction between a genuine portfolio contraction and a reporting correction matters for accumulation management. ARPC has stated it is still examining the factors behind the strata trend; neither ARPC nor any external party has confirmed a definitive cause as of the date of this report.

Total mitigation discounts applied to in-force home premiums reached $9.4 million as of March 31, 2026 – up from $9.0 million at the end of December 2025. National take-up rates remain low, with only 1.7% of home buildings receiving roller door bracing discounts and 0.9% each qualifying for window protection and roof tie-down upgrades. ARPC extended discounts to strata properties from April 2025 and to SME buildings from April 2026. Since October 2022, meaningful increases in quote success rates have been observed for medium and high-risk bands, but the mitigation discount framework has not yet produced the take-up rates that would materially shift the risk profile of the portfolio.