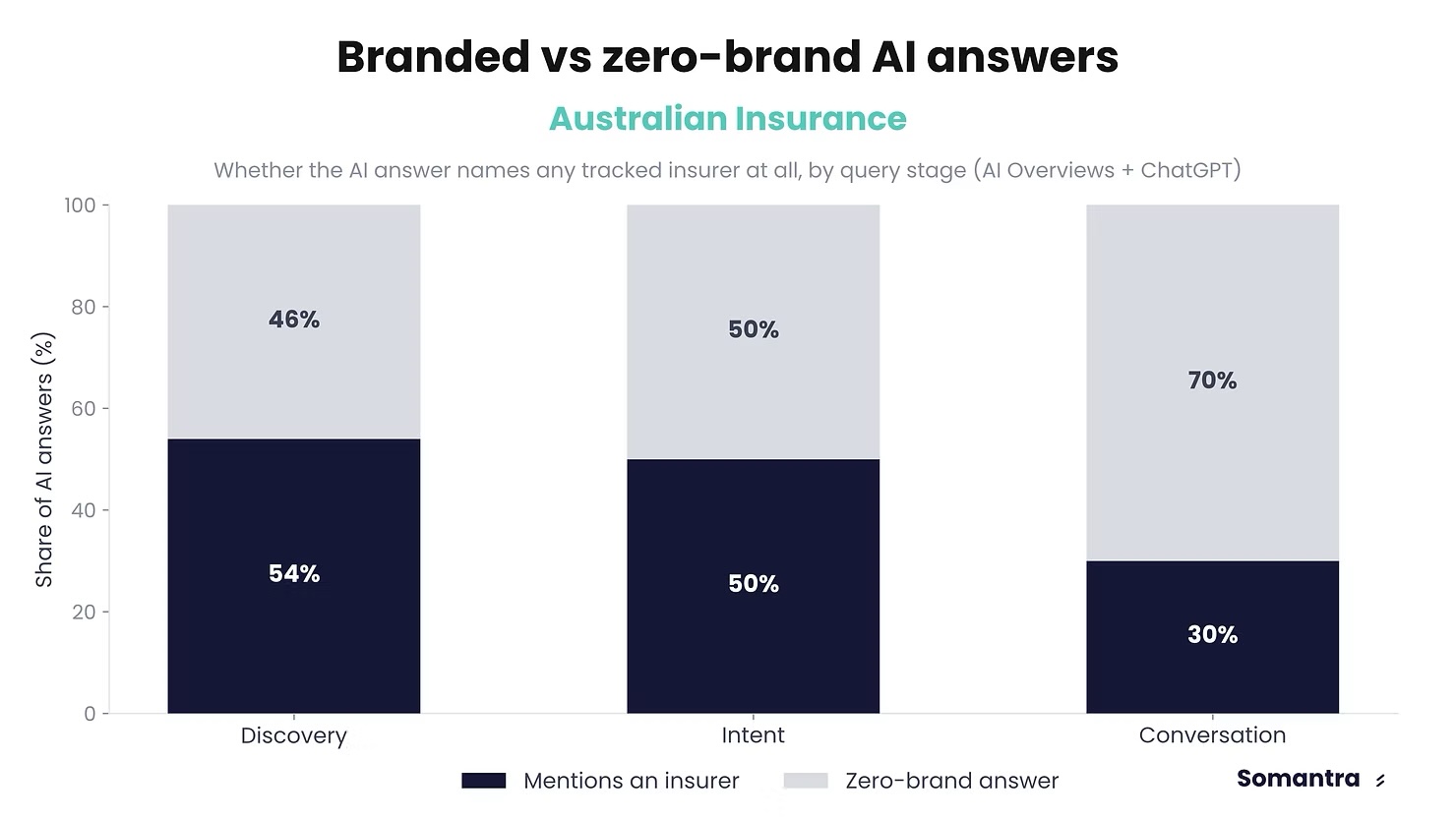

Artificial intelligence search platforms have begun concentrating Australian insurance consumer attention around a small number of brands. At the same time, seven in 10 detailed consumer queries return responses that name no insurer at all – a gap that represents an uncontested stretch of the consumer research journey that most insurers have yet to act on.

The findings come from Somantra, an AI search monitoring firm, which tracked 20 Australian insurance brands across 34,278 real consumer conversations on Google AI Overviews and ChatGPT throughout May 2026. The study covers 20 tracked brands rather than the full Australian insurance market. The data arrives as a separate GlobalData poll finds the broader insurance industry still cautious about AI’s maturity – a posture that may be costing mid-tier and specialty insurers ground that will prove difficult to recover.

The most consequential finding in Somantra’s data is not which brands are winning. It is how much of the market remains unclaimed. Across the detailed, intent-driven queries consumers pose to AI platforms – questions about specific coverage scenarios, eligibility conditions, and product comparisons – 70% of responses named no insurance brand. Across 34,278 tracked conversations, that represents approximately 24,000 consumer research interactions in a single month in which no Australian insurer received a mention on either platform. The pool of domains cited by AI engines contracted 21% between March and May 2026, falling from 10,777 to 8,488 unique domains. As that pool narrows, the barrier to entering AI-generated recommendations rises.

“This is not a problem. This is an opportunity. Every one of those brandless responses is a gap in the market, which is proof that the right content, structured the right way and published on the sources AI engines trust, could put a brand into that answer instead of nobody at all. The window is closing. Every month, more of the long tail gets claimed by whichever brand shows up first with the right content on the right sources. Waiting for AI search to mature before acting just hands that ground to a competitor,” said Arun Prasad, founder of Somantra.

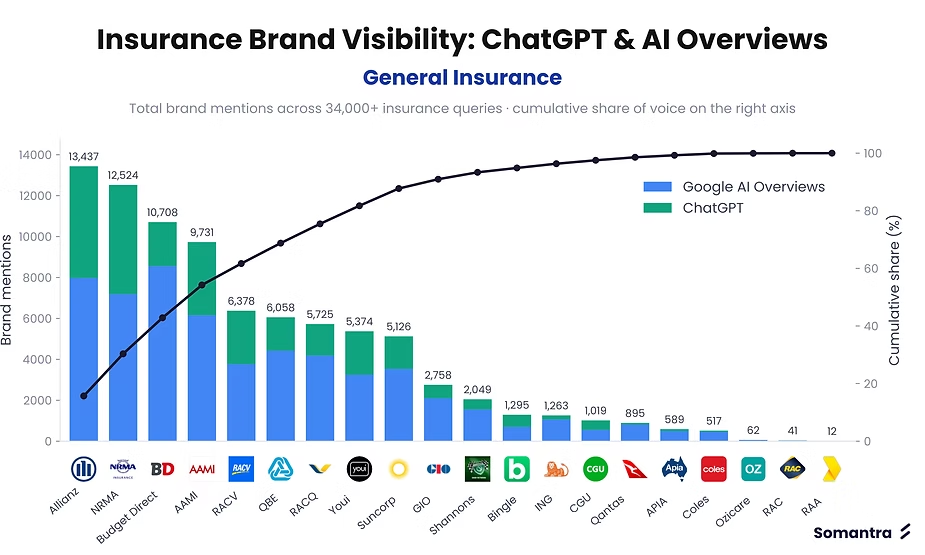

Where AI platforms do recommend brands, attention is concentrated among a handful of insurers. On ChatGPT, three brands – Allianz, NRMA, and AAMI – accounted for half of all insurance-related mentions. Nine brands collectively covered 90% of total mentions, leaving the remaining 11 tracked brands competing for a thin slice of visibility.

Google AI Overviews distributed attention more broadly, though not substantially so. Four brands reached the 50% threshold, and 11 were needed to cover 90% of mentions.

Allianz recorded the highest combined total at 13,437 mentions across both platforms, followed by NRMA at 12,524 and Budget Direct at 10,708. At the other end, Ozicare appeared in 62 conversations, Coles Insurance in 517, and Qantas Insurance in 895 – figures that suggest these brands are largely absent from AI-mediated consumer research, regardless of their standing on conventional search. “Google gives you options. ChatGPT gives you a shortlist, and the shortlist is getting shorter. If you are not already in the top tier on a given platform, you are fighting over scraps of visibility, not competing on equal terms,” Prasad said.

One of the more strategically significant findings is how rarely the two platforms agree. Google AI Overviews and ChatGPT recommended the same brand for the same query in only 27.9% of cases in May 2026, up from 23.7% in March. In roughly seven out of 10 head-to-head comparisons, a consumer asking the same question on each platform received a different brand recommendation.

Budget Direct illustrates the platform divergence risk in concrete terms. It led all brands on Google AI Overviews with 8,556 mentions, yet only 20.1% of its total AI visibility came from ChatGPT. For every five times Budget Direct appeared across both platforms, four of those appearances were on Google alone. As consumers increasingly use ChatGPT alongside Google to research financial products, a brand with that degree of platform concentration carries exposure it may not yet be measuring. For brands currently underrepresented on one platform, the divergence also creates an opening. Because Google AI Overviews and ChatGPT are forming their assessments of brand authority independently, a brand shut out of one platform’s preferred list may retain room to establish presence on the other.

“The dual combination of expanding opportunity surface area and divergence in brand recommendations between the AI search engines is the biggest opportunity for brands right now. Large brands have spent a decade optimising for a single search engine. That playbook does not transfer to a world where two major platforms disagree most of the time, and where most of the specific questions consumers ask are not being answered by anyone,” Prasad said.

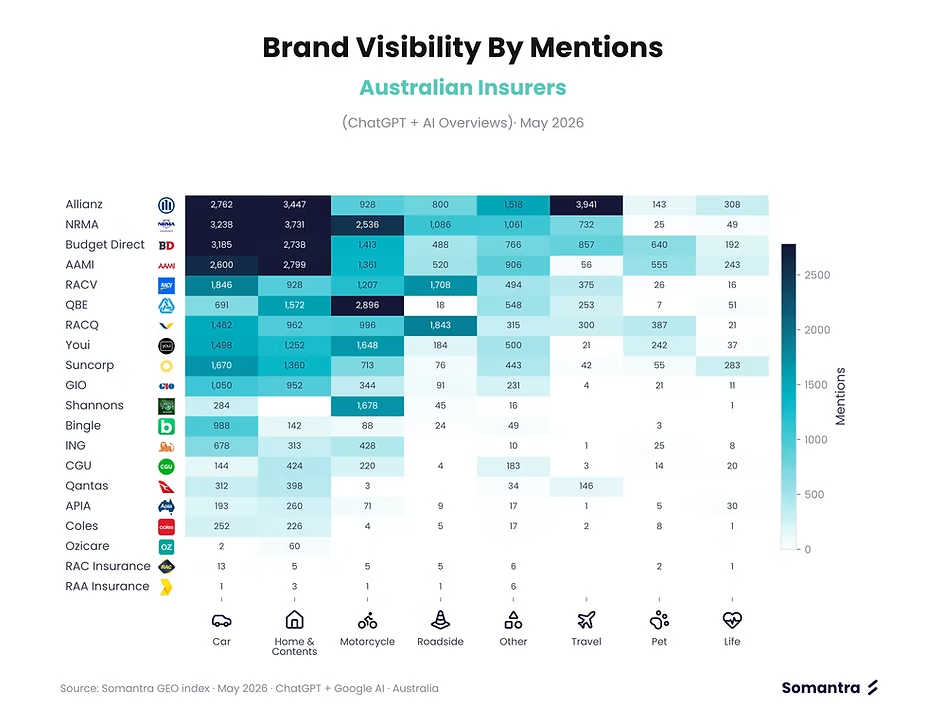

The opportunity is not evenly distributed across product lines, and the distinction matters for insurers assessing where AI search effort is most likely to yield results. Car insurance generated the highest volume of brand mentions at 22,777, followed by home and contents at 20,591 and motorcycle at 16,376. In these categories, established brands have accumulated visibility that a new entrant or smaller competitor would need sustained effort to displace.

Pet insurance and life insurance present a different picture. Pet recorded 2,457 total brand mentions across both platforms, and life insurance recorded 1,283 – categories where fewer brands currently feature in AI-generated responses. An insurer in either line that moves early to build presence on the sources AI engines cite faces less entrenched competition than one attempting to gain ground in car or home, where category leaders have already established substantial leads.

Within categories, those leads are significant. Allianz held 3,941 mentions in travel insurance, NRMA led car with 3,238, QBE led motorcycle with 2,896, and Budget Direct led pet with 940. The same brandless-query dynamic that applies across the market applies within these product lines: second and third-tier brands trail category leaders by margins that the data suggests are widening with each reporting cycle.

The two-month gap between Somantra’s March and May audits produced movement across the board. The pace of that movement is itself worth noting: AI search visibility appears responsive to recent content and citation activity in a way that shifts the competitive position of brands more quickly than conventional organic search typically does.

Allianz added 960 mentions to move past NRMA into the top overall position. Budget Direct posted the largest percentage gain among tracked brands, up 9.7%, displacing AAMI from the top three. AAMI recorded the steepest absolute decline, losing 2,147 mentions – an 18.1% drop. Bingle fell 30.8%, GIO fell 29.3%, and CGU dropped 27.8%.

Citation patterns on ChatGPT also shifted. In March, Canstar was the platform’s most-cited domain with 232 references. By May, both Finder and Canstar each exceeded 900 citations, with Finder taking the top position at 902. Reddit climbed from 147 to 387 citations, reflecting a source mix that extends well beyond traditional comparison-site ecosystems.

That ranking volatility is unfolding while much of the insurance industry is still forming a view on AI deployment altogether. A GlobalData poll of 113 insurance industry respondents, conducted across the first and second quarters of 2026, found that nearly a quarter believed AI had not yet reached a level of maturity suitable for widespread use within the industry.

Ben Carey-Evans, senior insurance analyst at GlobalData, attributed the hesitation partly to the narrow scope of current implementations and to unresolved questions about accountability. “This might be because use cases to date are largely around customer service and chatbots, rather than full-scale implementation. Regulation has not fully caught up yet and there is concern around who is liable for mistakes made by AI,” he said.

Those liability and regulatory questions are not abstract for an industry that distributes financial products to consumers. As AI platforms increasingly surface insurance brand recommendations in response to consumer queries, the question of how those recommendations are generated, and who bears responsibility when they are incomplete or inaccurate, sits unresolved across the industry.

A shortage of in-house expertise ranked as the second-most-cited concern in the GlobalData poll. The firm’s job analytics data recorded approximately 63,293 active AI-related insurance roles in 2025 – the highest on record and around 51% above 2024 levels. The hiring response reflects the scale of the gap, even as the technology continues to outpace the industry’s capacity to build expertise around it.

The tension between institutional caution and market movement is the central challenge the Somantra data poses for insurance executives. AI search is not a future consideration for Australian insurers. It is already determining which brands consumers encounter – and which they do not – before a policy is ever quoted.