The Top Insurance Executives and Professionals in Australia and New Zealand | Hot List

Jump to winners | Jump to methodology

Navigating the shifting tides

The insurance landscape remains as fluid as ever, but for those at the centre of the industry, the real challenge lies not in the presence of change, but in its increasing unpredictability and multiplicity.

In 2025’s opening chapters, both Australia and New Zealand witnessed early signs of a softening market, but the industry still grappled with fundamental issues such as:

-

AI adoption

-

climate resilience

-

regulatory complexity

-

evolving customer expectations

-

increased insurer competition

-

inflation

A key area is clients’ ability to search online and collate information from often unverified sources.

John Chandler, chief commercial and client officer at PIC Insurance Brokers, explains how the industry’s top performers counter this. “It is a skill to work through the pre-researched outcomes and either validate them or to develop the correct outcome based on the facts,” he says. “This means even more time spent asking questions to gather information, tailoring the conversation and building trust.”

The industry expert also underlines the need to accept technology but not to disregard the interpersonal skills which remain at the industry’s core. He says, “As uncertainty generally increases due to environmental and economic factors, insurance advisers can solidify their value-add by becoming a trusted expert, able to translate complexity on the clients’ behalf and build confidence about their decision-making.”

Director of the Australian Broker Network, Tremayne West, shares what he feels are crucial to being one of the industry’s leading professionals. “It’s experience, adaptability and authenticity, along with the ability to transfer knowledge and build the next generation of insurance experts by passing on solid and sustainable business models,” he says.

And West highlights areas that offer opportunities for the most dynamic operators. “Existing relationship patterns are shifting to social media and web-based platforms,” he says. “Emerging technology will better engage clients to create the feeling of personal contact and market efficiently, such as new-age CRM and AI platforms, but interpersonal skills are crucial to effective relationship management and the longevity of business.”

Insurance Business’ Hot List 2025 recognises the top insurance executives and professionals who are not only facing these evolving challenges but are also devising innovative ways to deal with them and lead the industry forward.

Australia insight

Underscoring the rate of change the industry is facing, Tetiana George, a member of Insurtech Australia and CEO of compliance software company Curium, referred to it as “unprecedented, both in terms of regulations and technology”.

A major driver is the July 2025 launch of the Australian Prudential Regulation Authority (APRA)’s cross-industry Prudential Standard CPS 230, designed to strengthen operational risk management and resilience across APRA-regulated entities.

KPMG Australia named the key adaptations caused by CPS 230:

-

prepared for risk events: ensure an effective process to support the management and response to risk events, effectively reducing their impact

-

customer and market impacting critical operations: understanding of critical operations and the associated resources critical to the operation to ensure appropriate mitigating controls

-

resilience: continue to operate through the ever-increasing breadth of disruption

-

protect the entity and community: business continuity planning and exercising critical to ensure that the impact of disruptions is minimised

-

effectively manage service provider risk: processes in place to identify, assess, manage and govern service providers that are critical to service delivery.

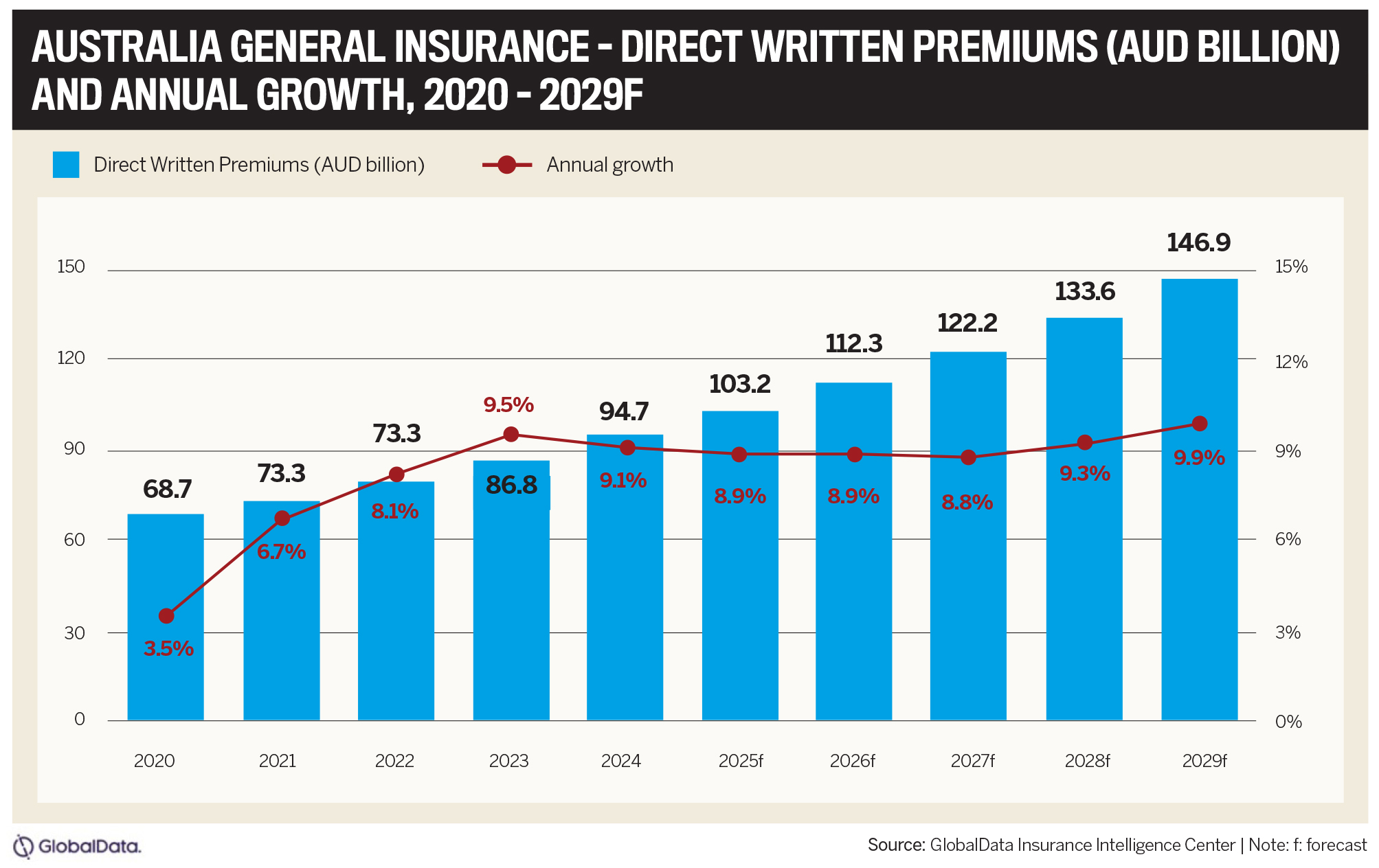

Australia’s insurance sector is bracing for a slowdown in premium growth in 2025, following years of steep increases driven by inflationary pressures, natural disasters and rising costs.

The Insurance Council of Australia’s (ICA) 2025 data showed that the total insured cost of extreme weather events over the past five years is $22.5 billion. That’s an average of $4.5 billion a year and an increase of 67% on the previous five years. Moreover, around 1.4 million properties face the risk of flooding, including almost 300,000 properties that face a severe to extreme annual flooding risk, largely in NSW, Qld and Vic.

For example, industry losses from February’s Tropical Cyclone and North Queensland floods exceeded $1.2 billion.

Andrew Hall, CEO of ICA, says, “The insurance industry is the financial shock absorber of the impacts of extreme weather events, which is expected to cost Australia $35.2 billion a year by 2050.”

With relation to motor claims, the average increased by 42% between 2019 and 2024 due to the higher cost of new cars, the increasing prices of parts and labour and the prevalence of vehicle technology.

There are also expectations that the commercial insurance market will grow as a result of greater awareness of cyberattacks, climate-related disasters and regulatory challenges. However, high reinsurance costs and ongoing claims inflation in sectors like property and liability may dampen profitability.

Sneha Verma, senior insurance analyst at GlobalData, says, “The Australian general insurance industry is set to experience consistently high growth over the next five years. However, increasing claim payouts due to rising inflation and an increase in losses due to frequent nat cat events will remain a significant challenge for general insurers.”

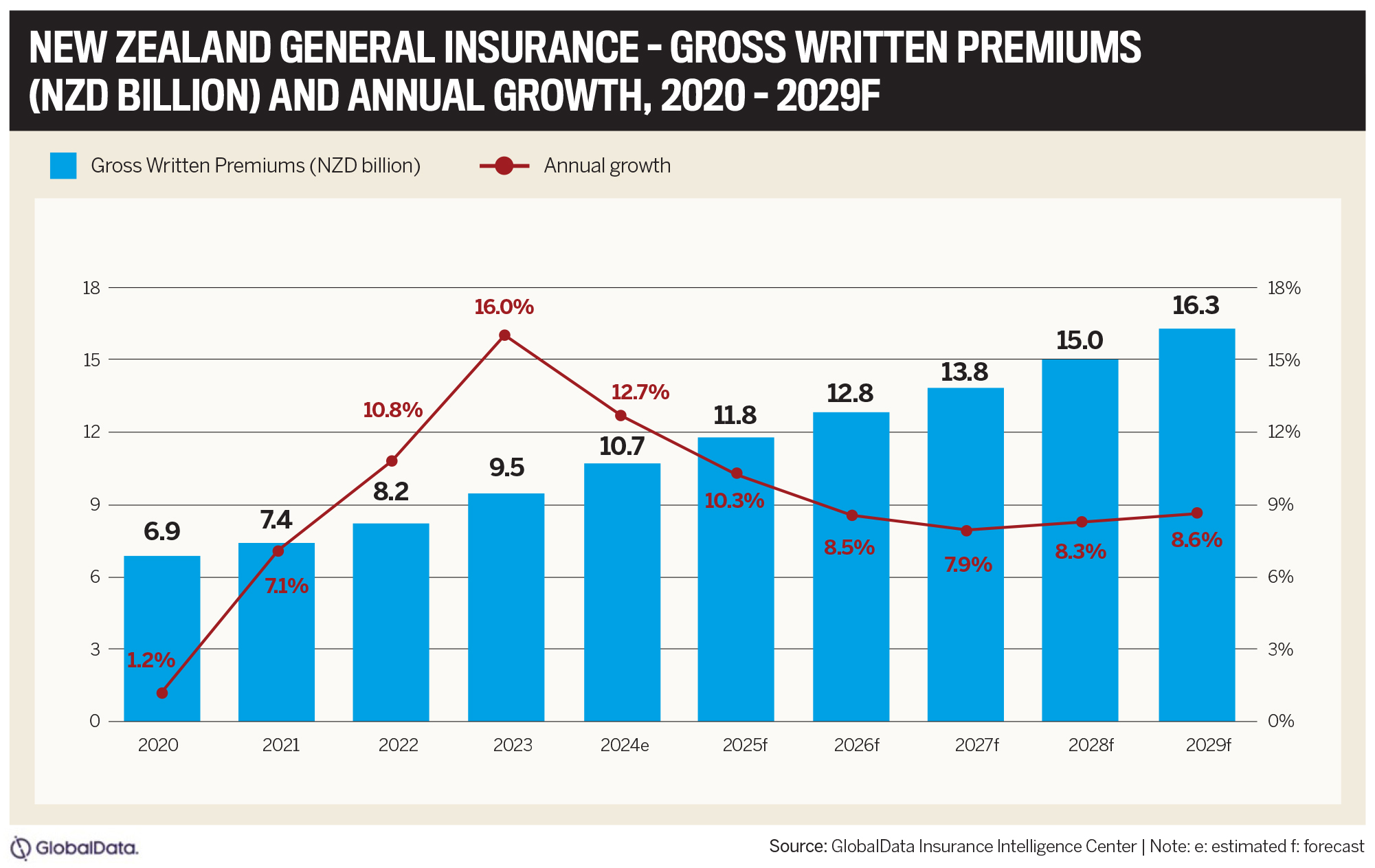

New Zealand insight

The national general insurance industry is projected to grow at a compound annual growth rate of 8.3% from NZD11.8 billion ($7.1 billion) in 2024 to NZD16.3 billion ($9.6 billion) in 2029, in terms of gross written premiums (GWP), according to research by Global Data.

Swarup Kumar Sahoo, senior insurance analyst at GlobalData, comments, “The growth of general insurance will be supported by a stable economic environment and regulatory reforms. The easing of inflation and growing private investment are expected to boost domestic demand and household consumption.”

Similar to Australia, natural disasters and related incidents are having an impact. In particular, there has been an uptick in demand for earthquake and natural disaster coverage due to high seismic activity.

Sahoo adds, “The trend towards risk-based pricing has further increased premiums for consumers. As climate-related claims surge, insurers face the challenge of balancing affordability with adequate protection while adapting to regulatory changes and evolving risk profiles.”

There was also a major regulatory update as the largest overhaul of insurance law in over 100 years came with the Contracts of Insurance Bill being passed in November 2024. It’s intended to make insurance legislation more modern and rebalance duties between insurers and insureds.

Law firm DLA Piper described the new position as “generally favourable to policyholders, and there will be increased pre-contractual obligations on insurers”.

The Insurance Council of New Zealand’s chief executive, Kris Faafoi, says, “The new law strikes a balance of consumers having much clearer rights at critical times and allows the fundamentals of insurers to be maintained.”

Hot List 2025

Four of the names featured on IB’s prestigious list share what’s enabled them to succeed and make their mark in the industry.

Michael Wood – Woodina Underwriting Agency

CEO Michael Wood has changed the face of the Australian industry in the last 12 months. Due to being a powerful mix of both underwriter and specialist PI insurance lawyer, he crafted a new way of handling claims. It has lowered defence costs and, in turn, allowed underwriters to offer terms to certain professions where insurance cover was and remains increasingly difficult to obtain, such as financial planners and solicitors.

The model’s success and three years of dedicated work saw Wood an integral part of APRA's authorisation of a new general insurer, Ivory Insurance, which commenced writing business in 2024. This has seen him deal with the regulatory demands that are so pervasive in the industry currently.

“There’s always a lot of compliance; it’s just the sign of the times,” says Wood. “It’s wonderful that the federal government was happy to authorise the new insurance company. One of the challenges is the extra compliance angle. My co-director, in particular, spends a lot of time on it.”

Wood’s unique expertise is also going further, as Ivory Insurance has been built to provide capacity to other underwriter agencies. And another piece of Wood’s empire, legal firm Martello Law, has a role to play beyond its current role as the in-house firm for Woodina Underwriting Agency.

“Martello Law will start acting on claims for other agencies that Ivory provides capacity to or where it at least leads the capacity provision,” explains Wood. “So that’s a great challenge for me, because that can then broaden the scope for Martello Law, and more insurers can benefit from that wonderful service.”

Ivory is aimed at providing specialist PI and GL capacity for Australian SMEs and has the capability to use Martello Law, providing access to the specialist PI lawyers at no cost. This is the model that Wood pioneered and is now excited to expand.

It began in 1993 in England, when he was a partner in a law firm. Wood says, “I came up with the idea of combining the law with underwriting, and in those days, you didn’t have multidisciplinary practices. You couldn’t have an insurance company being a partner. I thought, well, I’ll have to do it the other way and set up an insurance company with a law firm entwined in it.”

Michael WoodWoodina Underwriting Agency

That saw the first direct professional indemnity underwriter in England created, which went direct as well as through brokers. The crux of the model was that it had an internal law firm, initially headed by Wood.

He adds, “It would act on all the claims really efficiently at a very low cost, meaning that our loss ratios could be lower than our competitors, and hence our premiums could be low.”

With things going strong for Wood, he shares that a significant part of the success is down to instilling a positive culture. One element of this is that he advocates for internal growth and promotions. At Woodina, a lot of the underwriters began on the admin team. If they show promise and commitment, Wood pays for their insurance qualifications and provides a path forward.

Wood says, “I’m also able to incentivise a lot of my staff, particularly the middle and senior management, by allocating about 15% of the profit of the company. In Australia, what I do is I dedicate a lot of the pretax profit to bonuses, so everyone is very well rewarded.”

This type of integrity shone during the pandemic when Wood blocked any large increases in rates, unlike many competitors. “We don’t want to just reap extra profit because we can,” he says. “We’ve got to be loyal to long-standing clients, and so that’s what we did.”

This extends to Martello Law, which has a very loyal band of insurers who receive the highest standards of service. Rather than make a payment to end a claim, Martello prides itself on defending their clients.

“We tell them, ‘We’re going to defend your reputation and your claims record because you’ve got to live with that and you’ve done nothing wrong. Your reputation is really important to you, so we get in there and fight’,” says Wood.

The other enabler behind Wood having such a big impact is what he refers to as being “down to earth”. He builds connections and is committed to ensuring his teams are diverse across gender and background.

He says, “People love the fact that I have a very flat structure. My door is open to anyone.”

Battling the rise in natural disasters has been an unexpected upswing for the firm Anthony Bonanno founded, and where he is also CEO, as clients are attracted by his long-term vision.

He feels there has been somewhat of an unfair rise in home insurance premiums for many who haven’t made a claim in the past 20 years, as insurers have sought to recoup the large sums they have paid out following disasters across Australia.

Bonnano says, “It’s made people want to ask around for more quotes, and because we’re pretty good at what we do and we’ve got a good reputation, we’re getting a lot more work because of the inflated premiums.”

The reason is that Bonnano’s strategy is to retain customers and be as fair to them as possible. He says, “When it comes to our broker fee structures and stuff like that, we keep things pretty lean, in lieu of trying to build long-term relationships. It’s not about making a big buck today; it’s about making a small amount for a long period of time.”

Part of being able to ensure customers remain with ARCHER is not only price, but also standout customer service and communication. This touches on another of Bonnano’s major achievements over the past 12 months, as recruitment has been tough.

He has been able to attract several new team members, but had to compete for them. “We’ve been really successful in onboarding strong candidates,” says Bonnano. “Patience is probably the key for me because if you rush and you’re desperate, you can pick the wrong people, which can create an unhealthy environment.”

Anthony BonannoARCHER Insurance

This is crucial for Bonnano as he focuses on ensuring ARCHER is dynamic. He guards against complacency and leads from the front, while some CEOs might play golf some afternoons or have long lunches.

He says, “I’m in the trenches with the staff, and I think we’ve gained a lot of respect from the staff because they see we’re working just as hard as them. I’m really hard on myself, and I’m scared to lose what I’ve got.”

That’s not to say Bonnano doesn’t take breaks and holidays, but he admits to still checking emails and working a few hours a day from vacation to always stay connected and up to speed.

However, ARCHER wouldn’t have grown to what it is without a strong team, as Bonanno empowers them to perform but remains on hand for support and guidance.

“Everyone is an account manager in the office, and they’ve got portfolios that they manage, but I’m there behind the scenes, building relationships,” he says. “A lot of brokers, once they receive their commissions and premiums, don’t call people back for a week. Our fingers are always on the pulse.”

Proving the point, Bonnano has a dedicated claims team, but he still does claims personally, not only to set an example but also to show clients he remains rooted in the day to day.

ARCHER looks set to continue its trajectory by possibly acquiring other books of business, along with organic growth.

“I can feel that we’re getting a lot more opportunities in this market, and people are surprised by the way we operate,” says Bonnano. “It’s normal for us, but it’s probably not normal for a lot of other brokers – that’s what I hear from customers.”

Being at the forefront of change in the industry necessitates understanding and exploring AI’s role.

This is the situation the general manager, Sara Malins, finds herself in, as technology has already provided distinct benefits for employee productivity and client services.

To maintain pace with the constant change, Malins leverages Sedwick’s global reach to deliver tailored services to the New Zealand market. This ability to regionalise global technology advances gives Sedgwick a leg up.

Malins says, “That gives us that competitive advantage and also developing local tools that meet specific market requirements here. So not just necessarily taking what’s off the shelf but taking something and then shaping it to what we need for our business needs and clients’ business needs.”

Pursuing tech further is part of Malins’ strategy, and she sees opportunities to expand. “It’s using those new tools, getting them out in the market and continuing customer-centric service, making sure that we’re looking at vulnerable customers and delivering in that area,” she says.

In addition, Malins is in touch with the human element of her leadership role. She cites her favourite part of the job as seeing team members succeed and rise to meet new challenges.

Sara MalinsSedgwick New Zealand

Her approach is to work on people’s strengths and help them identify these areas. “Sometimes you don’t know what you’ve got unless someone helps you identify, and it’s then encouraging them to step up, take on extra responsibilities and learn different things,” Malins explains. “Rather than people just coming with the problem and me giving them the solution, I like them to come with their thoughts and help them build on that.”

Since beginning her career 35 years ago, Malins has seen a huge rate of change aside from technology, as back then, only a handful of loss adjusters were female.

She says, “I would say now 50% of our loss adjusters are women, and over 50% of our management team are women. There was a pretty old-fashioned view that loss adjusting was for men, and for women it would be to take the notes or make the coffee.”

Malins has made her mark in the industry and is passionate about empowering other women to thrive in insurance. “It’s about bringing them into the industry and encouraging them that they can do as well, if not better,” she says.

Adapting to the competition is where Simone Labady, CEO, has come into her own. She studies the industry and positions the firm where it needs to be.

Labady says, “It’s understanding the external environment, the competitive landscape, understanding our internal metrics, and therefore knowing which levers I can pull in order to deliver a profitable outcome, as well as the growth aspiration.”

Building a collaborative environment has been Labady’s approach, where everyone knows each other on a personal level, creating the trust necessary to succeed.

“Once people are talking to each other and working closely together, that fosters that culture,” she says. “Obviously, the productivity piece will come as a result of working together, but also the ability to problem solve. You need to have people who have the skill set that can problem-solve and work through issues.”

Mindful of how big an impact AI will have on the insurance world, Ladaby is doing a master’s in the topic, studying at night and on weekends. She highlights how technology is far more than a buzzword.

“Chief execs who do not understand technology will have a real gap in their knowledge going forward,” explains Ladaby. “I’m probably at the other extreme, but I do really like the technology space, and I think it’s what’s going to set companies apart.”

While Aioi Nissay Dowa Insurance NZ was an early adopter, especially on its core platforms, it has a way to go on AI. The key for Ladaby is using more tech to lessen needs from an operational perspective. However, she does not see this as being a cost-saving, but more as a redeployment of resources and people.

“It’s all about getting better outcomes for the customer,” Ladaby says. “When people talk about the fact that they’ll become more efficient in their operational areas, that’s fair enough, but I think we’ll be spending a whole lot more on IT. I don’t think as an organisation we’re going to save money, but there is a real shift in terms of roles.”

Simone LadabyAioi Nissay Dowa Insurance NZ

Having been CEO since 2018, Labady admits there is always more to learn. She says, “Leadership for me is really around trying to drive strategy. I’ve had very good people in my career who have taught me a lot about strategy, but I haven’t ever had to necessarily deliver entirely on my own.”

As another shining example of why doors need to be open to people from all backgrounds, Labady feels lucky to have learned the ropes at a firm with an encouraging environment for ambitious female employees like herself.

Now she’s doing the same within Aioi Nissay Dowa and has started a women in leadership development program to support them in acquiring different sets of skills.

“I think the industry is quite welcoming to women; where I see more of the gap is about how we harness their careers,” Labady adds. “I do see gaps for women in STEM, so we need to be promoting more women in those roles as they are particularly male dominated. So I’m thinking about how I get more of that balance, particularly within IT, into our organisation.”

Opportunities to capitalise on

Insurance in both Australia and New Zealand is ripe for disruption is the view of industry expert Kylie Bryant, a partner at Deloitte in consulting with extensive experience across insurance and financial services.

"The environment is changing rapidly as more InsurTechs join the fold, regulations change, population mix evolving and major changes to customer expectations," she says. "All of these are great opportunities for insurance professionals to embrace a new way of thinking and changing the way they are doing things. They must strike a delicate balance between embracing technology and maintaining strong interpersonal skills."

She adds, "Insurance professionals have evolved in recent times from deep technical specialists in their respective areas to generalists and strategists, who understand the insurance business as a whole and take in the bigger picture."

The major opportunities which Bryant highlight are:

-

Adopting new technologies and sustainable practices

-

Partnering and collaborating with InsurTechs to provide great solutions to clients without necessarily reinventing the wheel over and over again

-

Developing products that support environmental and social governance (ESG) goals

-

Leveraging open data and open APIs

The Top Insurance Executives and Professionals in Australia and New Zealand |

Hot List

- Adam Squire

Head of Claims

Lockton - Angus Kench

Vice President, Asia-Pacific Casualty and Crisis Claims and Global Casualty Product Board

Liberty Specialty Markets - Anita Lane

Joint Managing Director, Solution Underwriting Agency

Managing Director, CFC - Ben Bessell

Chief Broking Officer

Austbrokers - Brendan Dunne

Chief Customer and Operations Officer

Allianz Australia - Brett Pearce

Owner and Director

Pearce Financial Services - Brigitte Windsor

General Manager – Partnerships and Facilities

Rothbury Insurance Brokers - Claire Burke

Senior Specialty Risk Underwriter

CHU Underwriting Agencies - Craig Buckle

Chief Executive Officer

Lockton New Zealand - Declan Moore

Chief Enterprise Operations Officer

QBE Insurance - Gary Seymour

Chairman

Edgewise Insurance Brokers - Geoff Summerhayes

Chair

Zurich Insurance - Glenn Ross

Executive General Manager - Construction

UAA Group - Graham Cassidy

Head of Network Broker

Steadfast - Heather Coutts

Authorised Representative

Capstone Insurance Brokers - Janelle Greene

Chief Customer Officer and Chief Underwriting Officer

NTI - Jarrod Hill

Chief Executive Officer, CGU and WFI

IAG - Jen Bettridge

Clear Leader and Director

Clear Insurance - Jimmy Higgins

Chief Executive Officer

Suncorp New Zealand - Jo Mason

Chief Executive Officer

NZbrokers - John Lyon

Chief Executive Officer

Ando Insurance - Justin Delaney

Chief Executive Officer

Zurich Australia - Katie Stranaghan

Portfolio Manager – Financial Lines and A&H

High Street Underwriting Agency - Katrina Shanks

Chief Executive Officer

ANZIIF - Keith Roderick

Managing Director

Roderick Insurance Brokers - Ken Dixon

Director

Dixon Insurance Services Australia - Kent Chaplin

Group Chief Executive Officer

Delta Insurance Group - Kezia David

Special Counsel

Hicksons Lawyers - Kirsty Owens

National E-Business Manager

Berkley Insurance Australia - Kris Faafoi

Chief Executive

Insurance Council of New Zealand - Lisa Carter

Chief Executive Officer, Founder and Managing Director

Clear Insurance - Luke Whenman

Executive General Manager, Motor Claims Customers

Suncorp Insurance - Lynette Walsh

Global Corporate QLD State Director and Brisbane National

Aon - Lynn Roehrig

Head of Business Development, Australia and New Zealand

Descartes Underwriting - Marc Crossman

Executive General Manager – Distribution Strategy

UAA Group - Marcello Negro

Head of Product Management and Marketing

Finity - Matt Almond

Founder and Chief Executive Officer

HubSpoke - Michelle James

Chief Executive Officer

AA Insurance NZ - Michelle Le Long

Chief Operating Officer, New Zealand

PD Insurance - Monica Maharaj

Lead – Liability Claims

NZI - Neil Cousins

Chief Executive Officer

Steadfast New Zealand - Neşe Akay

Executive General Manager, Strategy and Innovation

Community Broker Network - Nick Hawkins

Managing Director and Chief Executive Officer

IAG - Nick McLardy

Chief Growth Officer

McLardy McShane Insurance Advisors - Nigel Fellowes-Freeman

Founder and Chief Executive Officer

Kanopi - Paul Johnston

Acting Chief Executive Officer

Tower Insurance - Pete Nicholson

Chief Executive Officer

Gallagher Bassett - Peter Chamberlain

Managing Director

allinsure - Peter McKenzie

Executive General Manager – Underwriting

SLE Worldwide Australia - Richard Klipin

Chief Executive Officer

National Insurance Brokers Association (NIBA) - Richard Mullaney

Business Owner and AR for Marsh

Marsh Advantage - Ross Preston

Manager, Major Risks

Lockton Australia - Sam Ratcliff

Chief Operations Officer

InsureBuild - Satpreet Chandra

Head of Affinity, NZ

Marsh McLennan - Shane Moore

Managing Director

Trade Risk - Sherly Zulkarnaen

Chief Financial Officer

Community Broker Network - Stephen Nguyen

Head of Distribution

AXA XL - Steve Johnston

Group Chief Executive Officer and Managing Director

Suncorp Australia - Sue Houghton

Chief Executive Officer

QBE Insurance - Tanushree Arora-Sopori

Executive Manager and Broker

Fortuna Advisory Group - Tony Wheatley

Chief Executive Officer

Berkley Insurance Australia - Tracey Bryan

Head of Regulatory Affairs and Compliance – Asia Pacific

Lloyd’s - Trudi Reeves

Head of Property Energy Construction Claims, Asia–Pacific

AIG - Tryan Christos

Managing Director

Interlink Insurance Brokers

Insights

Methodology

In January 2025, the Insurance Business team surveyed the industry and conducted independent research on the Australian and New Zealand insurance sector to find the most influential leaders who had made a significant impact over the previous 12 months. The team aimed to identify individuals who had spearheaded new initiatives in the insurance space and played a key role in driving the industry forward amid evolving market dynamics and emerging challenges. The team also considered previous awards won by the candidates.

Over 500 professionals from across Australia and New Zealand were identified. By the end of the research process, 70 key figures were selected for their leadership, innovation and contributions to the industry.

Keep up with the latest news and events

Join our mailing list, it’s free!