Top Insurance Claims Carriers in Australia and

New Zealand | 5-Star Claims

Jump to winners | Jump to methodology

The art of showing up

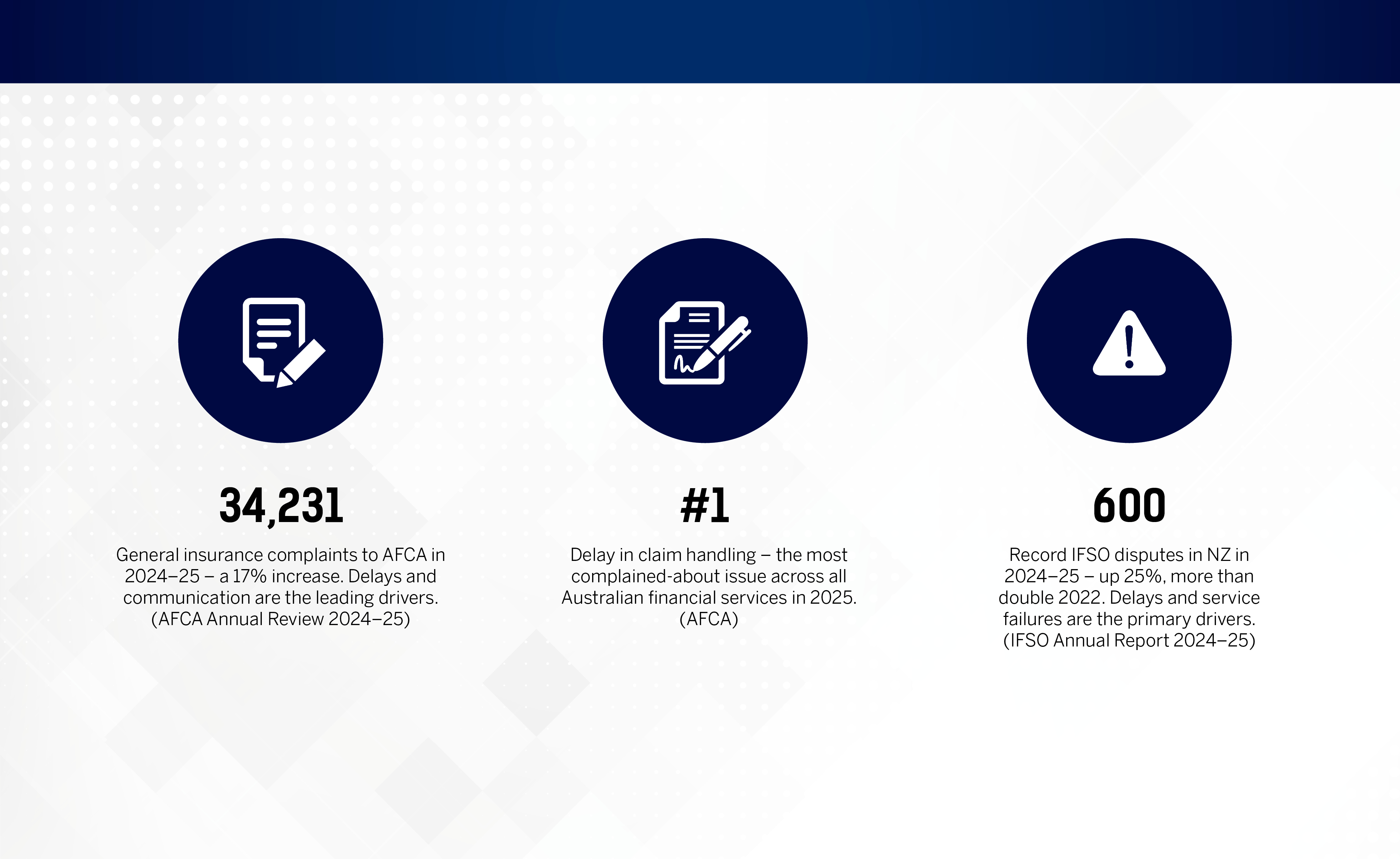

AFCA recorded 34,231 complaints in 2024–25. The number one issue was not coverage or price. It was communication. This report examines why the industry still calls that basic – and why the insurers that truly master it are pulling away from the rest.

The top insurance claims carriers in Australia and New Zealand are not being judged on product breadth or premium competitiveness. They are being judged on something far more fundamental – and far harder to sustain. The Australian Financial Complaints Authority (AFCA) recorded 34,231 general insurance complaints in 2024–25, a 17% increase on the prior year. The number one issue, year after year, was not disputed coverage, not premium shock, not bad faith. There were delays and poor communication.

In a sector managing billions of dollars in claims across two countries, dealing with natural disasters and rising complexity, the thing that drives people to a regulator most often is being left in the dark. Not hearing back. Not knowing who owns their claim. Not understanding what happens next.

At the 2026 Claims Leaders Summit in Sydney, AFCA’s chief executive put it plainly: the fundamentals that prevent complaints are timeliness, communication, transparency and closing the loop. She called it “doing the basics brilliantly.”

And yet the industry still refers to communication as “table stakes.” – something you do as a minimum. A baseline, not a differentiator.

This report argues that framing is wrong – and the data proves it. The insurers that brokers across Australia and New Zealand nominate year after year as their best claims partners are not always the largest. They are not necessarily the most technologically advanced. What they have in common is that they communicate, they own the claim and they do both things consistently – at scale, under pressure, claim after claim. That is genuinely hard. And the gap between those who do it and those who don’t is wider than anyone in the industry is comfortable admitting.

In New Zealand, the pattern is identical. The Insurance and Financial Services Ombudsman Scheme (IFSO) accepted a record 600 disputes for investigation in 2024–25 – a 25% increase on the prior year and more than double the total from 2022. Delays and customer service failures were, again, the primary drivers. The IFSO’s own guidance is explicit: even during catastrophe events, insurers are required to update customers at least every 20 business days and to identify and respond to customers experiencing vulnerability. That obligation reflects how seriously regulators view the communication gap – not as a soft-skills issue, but as a compliance one. From 31 March 2025, insurers operating in New Zealand have also been required to hold a financial institution licence and publish a fair conduct program, making transparency a condition of market operation, not a cultural aspiration.

Ask brokers what they want from a claims insurer, and you won’t hear a long list. The answer is almost always the same: someone who picks up the claim, knows what they’re doing and keeps moving.

Katherine Wilson, chief executive of IBANZ in Auckland, is unambiguous about where the pressure point sits.

Wilson is not describing a luxury. She is describing the minimum that brokers need to do their own jobs properly. When an insurer goes quiet, the broker fills the vacuum – chasing updates, managing anxious clients and doing work that should not be theirs to do. The claim doesn’t just become a burden for the insured; it becomes a burden for the broker.

Laura Meyer, director of MeyerInsure in Australia, works across property, professional indemnity and cyber claims. Her view of the market is candid: “The technology side has definitely improved. The service side, if I’m being honest, feels a bit mixed. Some insurers I used to consider the gold standard on claims don’t feel like they’re where they once were, which is disappointing.” Her gut assessment – that claims teams are being asked to do more with less – is one that the AFCA data appears to support.

The pattern Meyer describes – paper commitments that don’t survive contact with caseload reality – is the single biggest source of erosion in broker-insurer relationships. It is not that insurers don’t know communication matters. It is that they underestimate how hard it is to sustain at scale when the claims queue is long, staff are under pressure and complexity is rising.

What good actually looks like

Meyer deals in specifics. When a client recently faced a significant cyber claim – the kind of event where the first 48 hours define whether the business survives intact – what made the difference was not the policy wording. It was the insurer’s incident response team and panel lawyers engaging immediately, giving the client a clear point of contact within hours and a defined strategy before the end of day one. The claims team was UK-based, which created some communication friction across time zones, but the specialist expertise on the ground was unambiguous. The client felt held. The broker felt informed. That confidence in the early stages set the tone for the entire claim.

“Most brokers don’t expect perfection,” Meyer says, “but we do want to know someone is genuinely owning the claim and keeping it moving. The insurers that stand out are the ones where the process feels connected, and nobody is left wondering who’s actually driving things.”

Wilson identifies exactly where the system most commonly breaks down: “A common disconnection is around transparency and responsiveness. Brokers and clients expect clarity, accessibility and timely progress updates, while insurers are often balancing internal processes, resourcing pressures and increasing claim complexity. The gap usually comes down to communication.”

Insurance Business asked this year’s 5-Star Claims entrants to describe in detail how they handle claims – their philosophy, their processes, their tools and what they have changed in the past 12–24 months. The submissions were substantive. When you read them together, a consistent picture of operational excellence emerges. These are not aspirational statements. They are the mechanics behind what brokers experience.

Single ownership from lodgement to close

The strongest performers have eliminated handoff-heavy models. A dedicated handler is assigned at lodgement and stays with the claim – or a named, accountable team does – through to settlement. No mystery queues. No re-explaining the circumstances to someone new. This sounds obvious until you try to maintain it under volume pressure. The leading insurance claims carriers have built it into their operating model, not left it to individual effort. Several have automated the assignment process itself so that from the moment a claim is lodged, the insured and broker have a name and a contact number.

Automation that earns back human time

The leading firms are not automating for its own sake. They are using straight-through processing, AI-assisted triage and automated workflows to clear routine, low-complexity claims at speed – freeing experienced handlers to focus where judgement actually matters: complex losses, vulnerable policyholders and contentious coverage questions. Technology used badly creates another layer between the customer and the resolution. Used well, it removes the administrative friction that buries good claims handlers in tasks that add no value. Several of this year’s entrants have redeployed staff freed by automation into senior claims management positions – moving people up the value chain, not out the door.

Claims and underwriting at the same table

A recurring feature across the top submissions is structural integration between claims and underwriting. Real claims outcomes feed back into policy wording and product design. Claims professionals sit with underwriters, join key account tenders and flag coverage ambiguities before they become disputes. The result is that when a claim arrives, the handler understands what was promised when the policy was sold – because they helped shape the product. This loop closes the gap between underwriting intent and claims reality, and brokers who work with these firms notice the difference: fewer coverage debates, faster decisions and consistent messaging from both sides of the house.

Communication built into the process, not left to personality

The best operations treat communication as a system. Automated updates go out at defined points in the claims lifecycle. Brokers have real-time visibility of where a claim sits. Customers are not left in silence between assessor visits. The firms with the strongest communication records are not simply sending more messages – they are designing the right messages, at the right moments, with clear next steps and a named owner attached. Some of the leading insurance claims carriers are now sending hundreds of automated real-time updates daily across their portfolios. That kind of consistency cannot be achieved through individual effort alone. It requires workflow design, platform investment and leadership that treats communication as a measurable operational output.

Specialist expertise matched to claim type

Generalists claim teams cannot handle complex losses well. The top performers have built specialist streams – professional lines, commercial motor, personal injury, cyber, specialty, catastrophe – staffed by people who understand the specific exposure, the policy intent, and the commercial reality the client faces. When a large cyber loss or a complex property claim comes in, the handler already knows the territory. That expertise translates directly into faster, better-calibrated decisions and fewer escalations. Knowing the claim will land with someone who genuinely understands it is itself a form of communication.

Catastrophe response that is built, not improvised

For the Australian and New Zealand markets, maintaining service standards during catastrophe events is no longer a nice-to-have – it is a minimum expectation. What separates the leaders is that their surge capability is pre-built and tested, not improvised when the event strikes. Early-warning intelligence, pre-defined activation triggers, trained surge workforces and structured governance frameworks mean that when the volume hits, the operating model holds. The firms that struggled in recent catastrophe seasons did so because they treated scale-up as a problem to solve on the fly rather than a system to have ready.

Technology has improved the front end of claims dramatically. Online lodgement is faster. Digital document upload has removed friction. AI-assisted triage is accelerating routine decisions. The insurers at the top of this year’s field are using agentic AI to cut settlement times on certain claim types from days to hours. Real-time decision support tools are allowing handlers to stay focused on the customer during calls rather than toggling between systems. The picture is genuinely more advanced than it was two years ago.

Why portals alone aren’t the answer

Meyer, who handles claims across property, professional indemnity and cyber, offers a useful corrective to the technology optimism.

A portal that accepts a claim and then falls silent behind a backlogged team is not a communications improvement – it is a communications failure with a better front door. The leading insurance claims carriers understand this distinction. Their technology investments are oriented around full life-cycle visibility, not just lodgement efficiency. They are building systems that keep brokers and clients informed throughout the claim, not just at the point of entry.

The human element remains essential

Wilson, chief executive of IBANZ, draws a clear line: “AI-assisted claims triage and smarter workflow automation are already starting to transform parts of the claims process, but the human element remains essential.” The complexity and emotional stakes of a significant claim – a home destroyed by fire, a business interrupted by a catastrophic loss – cannot be managed by a system alone. What technology can do is create the space for skilled humans to focus on exactly those moments. The top-rated insurance claims carriers have understood this from the start: automation is a lever for better human service, not a substitute for it.

Ask brokers what the best claims experiences feel like, and they use the same language consistently: connected, clear, moving. Not perfect – brokers are realistic about complexity, about weather events and about supply chains that delay repairs. What they cannot absorb is silence. What erodes trust fastest is not a slow claim – it is a slow claim with no explanation and no owner.

The 5-Star Claims winners for 2026 represent the top insurance claims carriers across Australia and New Zealand as nominated by brokers and industry professionals. The cohort spans large multinationals and specialist domestic players, personal and commercial lines, broker-focused and direct models. What they share is not size or technology budget. It is a consistent commitment to the fundamentals Wilson and Meyer describe: clear ownership, proactive communication and the operational discipline to maintain both when the pressure is highest.

Wilson puts the competitive stakes in plain terms: “Leading claims carriers should focus on consistency of decision-making to provide more certainty throughout the claims journey and empowering claims teams to make informed decisions quickly.” That empowerment point is critical. Handlers who have to escalate routine decisions cannot communicate confidently. The insurance claims carriers that score highest with brokers tend to be the ones that have given their people the authority to move – and the training to do so correctly.

From in-house electricians to AI-powered lodgement, NZI’s Meg Warner explains how a culture of empowerment, proactive broker education and a commitment to loss prevention are setting a new standard for insurance claims carriers across New Zealand.

For NZI, New Zealand’s leading commercial insurer, winning a 5-Star Claims designation is not the result of a single initiative – it is the outcome of deliberate, structural investment in people, technology and broker relationships, compounded over years. At the centre of that investment is Meg Warner, executive manager of broker and specialist claims at NZI, who has built an insurance claims handling culture as focused on preventing losses as it is on resolving them.

Warner’s approach is grounded in a direct principle: keep brokers informed, and better client outcomes follow. That framing shapes everything NZI does in its claims operation – from delegations designed to enable same-day resolution to the broker education programs that sit at the heart of its competitive advantage.

How NZI’s claims culture drives better outcomes for brokers

Warner is emphatic that NZI’s claims performance ultimately comes down to culture. The environment she has built is client-focused, collaborative and deliberately empowering – designed so that handlers feel trusted to make decisions, confident to escalate early and equipped to work across teams when complexity demands it. That empowerment is backed by genuine career pathways within the claims function and into the broader NZI and Insurance Australia Group (IAG) business, retaining experienced talent while continuously refreshing perspectives at every level.

That principle is not left to individual effort. Between April and June 2026, NZI’s liability claims team delivered a series of continuing professional development-accredited training sessions across Auckland, Wellington and Christchurch, reaching hundreds of brokers. Each session was built around real claims case studies covering general liability, legal liability and statutory liability – giving brokers a working understanding of how the claims process functions and how to set clients up for success from the point of placement. Feedback from brokers and NZI’s own internal teams was, by Warner’s account, exceptional.

Responding to New Zealand’s escalating weather risk

The pressure on NZI’s insurance claims handling operation has intensified markedly in the 12–18 months to mid-2026. According to IAG’s 8th NZ Wild Weather Tracker, released in April 2026, the frequency of storms affecting New Zealand more than doubled – from a 15-year historical average of once every 19 days to once every eight days in the 12 months to April 2026 – making severe weather a near-weekly operational reality. Claims volume between autumn 2025 and summer 2026 rose 256% year on year.

NZI’s response was structural. The insurer established a dedicated Major Events team to manage home, contents and vehicle claims arising from weather events – allowing its standard claims operation to maintain service levels for non-event work simultaneously. The claims strategy continues to evolve with each event type – wind, flood and storm – rather than relying on a single approach.

Technology in the claims process: AI that earns its place

NZI is deploying AI in two targeted ways on the frontline of its claims process. First, an in-house tool that helps claims handlers navigate the multiple policy wordings in the New Zealand market – enabling faster, more confident decisions without manual cross-referencing. Second, a recently rolled-out AI-powered motor claims lodgement system that converts broker-supplied information – whether a formal claim form, an email, or a photograph of handwritten notes – into a lodged claim automatically, removing what was previously a manual administrative task entirely.

Both applications reflect NZI’s broader philosophy on technology: automation that removes friction from routine tasks so that skilled handlers can focus on complex losses, vulnerable policyholders and coverage judgements that require genuine human expertise.

Loss prevention as a claims strategy: NZI’s industry-first initiatives

What distinguishes NZI most sharply from its peers is its commitment to preventing the insurance claims it would otherwise have to resolve. After identifying a higher-than-usual volume of fire losses attributable to electrical malfunction – a finding corroborated by Fire and Emergency New Zealand, NZI introduced the NZI Electrical Review service, which it describes as an industry first in New Zealand.

The service deploys a national team of in-house registered electricians, each holding Electrical Inspector and Level 1 Thermographer qualifications. They visit NZI commercial clients’ premises, conduct thermal imaging inspections of switchboards against prescribed New Zealand industry standards, and provide a written report detailing any required remediation – free of charge to all NZI commercial clients. Since launch, the team has visited over 2,600 clients and identified more than 7,500 problems requiring resolution, the most common being overloaded multi-boards and poorly maintained electrical systems. Driven by broker demand, the team has grown from a two-person trial to a national operation of 10.

The Electrical Review service is the commercial property equivalent of NZI’s Fleet Fit program – a risk mitigation initiative running for more than 20 years that helps commercial fleet operators manage vehicle-related fatigue risk and the challenges of an ageing driver workforce. NZI Truckie Rest Zone events, run in partnership with New Zealand Police and Hato Hone St John, bring fleet risk managers into direct contact with commercial drivers. At the most recent event in Paengaroa, NZI’s team spoke with more than 130 drivers, while Hato Hone St John conducted blood pressure and general health testing for 32 drivers on the day.

What sets NZI apart in how it handles claims?

Q: What is the key factor in NZI's claims process standing out and delivering for clients?

A: “Be it a relatively simple claim that brokers can use their own delegations or a complex claim that sits with our technical or specialist teams, we look to understand what the immediate need is for our clients and to solve that.”

How has NZI responded to New Zealand’s growing weather challenge?

Q: What trends have you noticed in claims over the last 12–18 months, and how have you handled them?

A: “We are consistently seeing a lot of smaller weather events. We have set up a major events team dedicated to looking after our clients whose homes, contents and vehicles have been affected. With each event, our claims strategy continues to evolve and adapt to the type of event – wind, flood and storm. Having this dedicated team in place helps us continue to maintain our high level of service for non-event-related claims.”

What benchmarks does NZI set for turnaround times?

Q: In terms of turnaround times and speed, what benchmarks do you set?

A: “We’re working with our brokers to provide enough information on day one for us to open, pay and close a claim in one transaction. This is where the broker claims delegations are really valuable – it’s a great client experience to be told, ‘That’s covered, and we’ll get the quote paid today.’ Not all claims are as straightforward as that, but where they are, we really encourage our team to fast track as much as possible.”

What does AI actually do for NZI’s frontline claims teams?

Q: How big a role does AI and technology play in the frontline claims process?

A: “We’ve built an in-house tool to help our teams navigate the dozens of different policy wordings in market – it allows the team to move quickly between agreed wordings and make faster, more confident claims decisions. We’re also using AI to streamline the lodgement of private motor claims, enabling us to take information provided by a broker, whether that's in a claim form, an email or even something as informal as a photo of handwritten notes, and convert it into a lodged claim. This has been a really exciting step for us.”

How does NZI’s claims culture lead to better performance?

Q: What type of environment and culture do you create internally, and how does this lead to better claims performance?

A: “We work hard to create a culture that is client focused, collaborative and empowering. Claims can be fast moving and at times emotionally charged, so it’s important our people feel supported, trusted and clear on what good looks like. That culture leads to better claims performance because our teams are confident to make decisions, escalate early when needed and work closely across different teams to keep claims moving. When people feel connected to the purpose of what they do and are encouraged to continuously improve, it shows in the quality of decisions and ultimately the experience we deliver for brokers and clients.”

What feeling does NZI want to leave clients with after a claim?

Q: What do you want clients to feel after a claim with NZI?

A: “I’d love our clients to come away feeling that yes – they chose the right insurer with NZI. We want clients to feel informed, supported and confident that we are helping them through what is often a difficult time. Communication is a critical part of that. If clients are left with a clear sense that we were responsive, easy to deal with and genuinely focused on helping them reach a good outcome, then we've done our job well. At NZI, we believe insurance is more than just responding to events – it’s also about how we can use the information and expertise we have to help our clients prevent future losses.”

Kira Pellicano, head of commercial claims at Vero, on what drives standout claims performance in Australia and New Zealand – and why the real measure of a policy is how it delivers at claims time.

For Vero, excellence in insurance claims in Australia and New Zealand begins well before a loss occurs. As one of the top insurance claims carriers in Australia and New Zealand recognised in IB’s 2026 research, the carrier has built its reputation on a model that prioritises early alignment between claims teams and the broker network – a relationship-led approach that, according to Kira Pellicano, head of commercial claims at Vero, ensures expectations are clear and shared long before a claim is triggered.

"Our striving for excellence in claims handling is driven by the strength of our relationships and the expertise and compassion of our people," says Pellicano. "Our dedicated claims relationship teams across the country work closely with brokers year-round, so expectations are clear and we’re aligned well before a claim occurs."

That emphasis on pre-claim alignment is more than a service philosophy. With AFCA receiving 34,231 general insurance complaints in 2024–25 – a 17% increase on the prior year, with claim delays consistently identified as the primary driver – the pressure on carriers to perform has never been more visible. Vero has observed the impact of major weather events compound the financial fragility of smaller commercial clients, prompting a stronger focus on tailored support: additional resourcing, access to support services and, where possible, progress payments to ease cash flow pressure during the claims process. At the same time, Pellicano flags a more structural challenge the carrier is actively working to address: inaccurate occupation coding at policy inception. "Getting that right upfront is critical, and we work closely with brokers to support good outcomes at claims time," she says.

Speed, complexity and the right-person principle

On turnaround times, Vero – named among the 5-Star Claims winners for 2026 alongside AIG and Arch Insurance Australia – has moved away from single-benchmark targets in favour of what Pellicano describes as a "dual approach": a streamlined process for simpler claims running alongside deep technical capability for complex matters. The logic is deliberate: no two claims are the same, and routing each one to the right person with the right expertise, from the outset, is what drives both speed and quality.

"We know that there's a direct correlation between speed of resolution and satisfaction," Pellicano says. The model is also designed to protect that correlation under volume pressure – ensuring complex commercial claims are not bottlenecked by processes built for simpler ones and vice versa.

Internally, the culture underpinning these outcomes is built on three principles: customer centricity, fairness and accuracy in decision-making. Pellicano is direct about what this means in practice – assessing each claim clearly and consistently, with the customer at front of mind, and delivering outcomes that are reasonable and aligned to the intent of the policy.

Technology as an enabler, not a substitute

Technology at Vero is framed not as a replacement for human judgement but as an enabler of access and speed at the lodgement stage. Across Vero Insurance’s claims process, the carrier supports multiple lodgement channels – phone, online and email – with automation and data science models in place to ingest email claims directly into its core claims platform, providing immediate confirmation and faster progression for brokers and customers.

Looking ahead, Pellicano says Vero is actively scoping the use of agentic AI to enhance lodgement and triage structures – a development she describes as "an exciting opportunity" to further reduce friction at the critical first contact point.

Ultimately, Pellicano frames the claims experience in terms of what it means for client retention and long-term trust. A claim is the moment the product is tested, and how a carrier performs in that moment defines whether a client chooses to renew. The strength of that broker relationship was reflected in Vero’s performance in the IB 2026 Brokers on Insurers survey, where the carrier secured the silver medal for Insurer of the Year and gold for BDM support across 11 performance categories.

"While no one specifically wants to call on their insurance product to lodge a claim, when they do, we want customers to feel confident in their cover and grateful for the support they receive," says Pellicano. “We want them to choose to stay with Vero because of that best-in-class claims experience.”

Vero on claims: Q&A with Kira Pellicano

Head of Commercial Claims, Vero

Q: What is the key factor in Vero’s claims process standing out and delivering for clients?

A: “Our striving for excellence in claims handling is driven by the strength of our relationships and the expertise and compassion of our people. Our dedicated claims relationship teams across the country work closely with brokers year-round, so expectations are clear and we’re aligned well before a claim occurs. At the same time, our claims professionals keep the customer front of mind, focusing on speed and clarity, helping businesses to get back up and running as soon as possible.”

Q: What trends in claims have you dealt with over the last 12–18 months, and how have you responded?

A: “We’re seeing increased vulnerability across our small business segment, particularly following major events. That’s driven a stronger focus on tailored support, including additional resourcing, support services and, where possible, progress payments to ease financial pressure. More broadly, we’re also seeing the impact of inaccurate occupation coding at the inception of a policy. Getting that right upfront is critical, and we work closely with brokers to support good outcomes at claims time.”

Q: How do you approach turnaround times and speed benchmarks?

A: “No two claims are the same, so our focus is less on a single benchmark and more on getting the path right from the start, ensuring each claim is handled by the right person with the right expertise. We’ve built a dual approach with a more streamlined process for simpler claims and strong technical capability for more complex matters. That balance is what enables efficient and high-quality outcomes, and we know that there’s a direct correlation between speed of resolution and satisfaction.”

Q: What culture do you build internally, and how does it lead to better claims performance?

A: “We’ve built a culture around customer-centricity, fairness and accuracy in decision-making. Our role is to assess each claim clearly and consistently, with the customer front of mind, and to deliver outcomes that are reasonable and aligned to the intent of the policy.”

Q: What role does AI and technology play in the frontline claims process?

A: “Technology plays an important role in improving access and speed, particularly with the lodgement of a claim. Enabling preferred channels of choice for lodgement has always been important for us, ensuring a broker or customer can lodge with us in their preferred way. Alongside phone and online lodgement, we have automation and data science models in place for email lodgement to ingest the information into our core claims platform, so customers and brokers receive immediate confirmation and faster progression. We are now looking at enhancing our lodgement and triage structures through agentic AI, which is an exciting opportunity.”

Q: What feeling do you want clients to take away post-claim?

A: “A claim is where the real value of the product is determined. There is no point in purchasing cover that does not offer protection when you need it most. Our focus is on making that experience as smooth and supportive as possible. From a broker perspective, that means being open and transparent, responsive, clear and easy to work with. While no one specifically wants to call on their insurance product to lodge a claim, when they do, we want customers to feel confident in their cover and grateful for the support they receive. We want them to choose to stay with Vero because of that best-in-class claims experience.”

The pressure on claims operations is not easing. Climate risk is increasing the frequency and severity of weather events across both countries. Complex commercial risks – cyber, professional liability, management liability – are generating claims that require genuine expertise, not just process compliance. Cost-of-living pressure means insured clients have less tolerance for delays and less capacity to absorb uncertainty. And regulators on both sides of the Tasman are watching more closely than they have in years.

Regulatory pressure in Australia

In Australia, AFCA has updated its claim delay guidance, placing clearer expectations on how insurers document and communicate reasons for delay throughout the life of a claim. Insurers must now clearly explain what is causing a delay, what steps are being taken to resolve it, and when the customer can expect an update. The message from the regulator mirrors the message from brokers exactly: say who owns the claim, explain what is happening, and do not leave people in silence.

New regulatory obligations in New Zealand

In New Zealand, the regulatory environment has tightened materially. The Financial Markets Authority (FMA) licensing regime introduced in March 2025 has formalised fair conduct obligations that were previously voluntary. Insurers must now publish a fair conduct program and demonstrate how they will treat consumers fairly throughout the claims process – including how they communicate, how they handle delays, and how they escalate vulnerable cases. The IFSO’s record dispute volumes in 2024–25 underline exactly why the regulator acted when it did. The expectation that insurers update customers at least every 20 business days during catastrophe events – an IFSO code requirement – is no longer an aspiration. It is a minimum standard against which insurers are measured.

The compounding advantage

Against this backdrop, the gap between the insurance claims carriers that have invested in communication as an operational discipline and those that have not will become harder to close. The technology investments required to deliver full life-cycle visibility are significant. The cultural change required to empower frontline handlers is deep. The talent required to staff specialist claims teams takes years to build. None of this happens quickly. The firms that started early – and this year’s 5-Star winners represent a significant number of them – are compounding that advantage year on year.

Wilson frames the horizon clearly: the consistency of decision-making and the empowerment of claims teams to act quickly are not just operational goals. They are the foundations of trust between insurers and the broker community – and once trust is lost at the claims stage, it is very difficult to rebuild at any other point in the relationship.

The insurance industry has spent years calling communication a baseline. The AFCA complaint data, the IFSO’s record dispute figures, and the broker feedback captured in this report all say the same thing: it is not a baseline. Doing it well – consistently, at scale, under catastrophe pressure, across thousands of claims simultaneously – is operationally demanding in a way the industry has chronically underestimated.

The top insurance claims carriers in Australia and New Zealand for 2026 have not arrived at their positions by accident. They have made deliberate structural choices: single ownership models, specialist teams, integrated underwriting and claims functions, and communication designed as a system rather than a behaviour. Those choices compound. The gap between the firms that have made them and those that have not is now wide enough that it will not close quickly.

For brokers, the practical implication is straightforward: the insurers on this list have earned the trust that translates into client confidence during the worst moments. For the industry, the challenge is harder. Calling communication basic is no longer a defensible position. The data, the regulators, and the brokers have all said so. The only question left is how long it takes for everyone to act accordingly.

Top Insurance Claims Carriers in Australia and New Zealand | 5-Star Claims

- Allianz

- Chubb Insurance

- FMG Insurance

- Insurance Australia Group (IAG)

- QBE Insurance

- Tower

Insights

What is the Insurance Business 5-Star Claims report?

The Insurance Business 5-Star Claims report identifies the top insurance claims carriers across Australia and New Zealand as nominated by brokers and industry professionals. It recognises insurers that demonstrate excellence in claims handling, communication, transparency and broker support. The report covers both the Australian and New Zealand markets and is published annually by IB, part of Key Media.

How were the 5-Star Claims winners selected?

Winners were selected through a two-phase research process. IB first surveyed its national network of brokers and industry professionals across Australia and New Zealand to identify which insurance claims carriers deliver the best service. Insurers that received a sufficient volume of nominations were then invited to complete a detailed submission evidencing their claims capabilities – including service standards, turnaround times, dispute resolution processes, technology and broker support frameworks. The research team analysed both quantitative survey results and qualitative submissions, with final scores based on broker ratings across key performance indicators.

How serious is the insurance claims complaint problem in Australia and New Zealand?

In Australia, AFCA received 34,231 general insurance complaints in 2024–25 – a 17% increase – with delay in claim handling the leading driver of escalation every year. In the 2025 calendar year, delay in claim handling became the single most complained-about issue across all of Australian financial services, with 9,274 complaints specifically about claim delays (AFCA). In New Zealand, the IFSO Scheme accepted a record 600 disputes for investigation in 2024–25, more than double the 2022 total, with delays and communication failures consistently identified as the primary drivers.

What do brokers expect from a top insurance claims carrier in 2026?

Brokers consistently identify three priorities: a named, accountable owner who sees the claim through from lodgement to settlement; proactive and timely communication at every key stage; and specialist expertise matched to the complexity of the claim. According to Katherine Wilson, chief executive of IBANZ in Auckland, the single biggest differentiator is whether an insurer communicates proactively and consistently. Brokers are realistic about complexity and delays. What they cannot absorb is silence or a claim that moves between handlers without clear ownership.

How is technology changing insurance claims handling in Australia and New Zealand?

Leading insurance claims carriers are using AI-assisted triage, straight-through processing, automated workflow tools, and digital lodgement platforms to resolve routine claims faster and free experienced handlers to focus on complex losses. Some are now using agentic AI to cut settlement times on certain claim types from days to hours. However, industry experts caution that technology improvements at the front end of the process have not yet been matched by full life-cycle claims management capability – and that digital systems are only as effective as the people and processes operating behind them.

What regulatory changes are affecting insurance claims in New Zealand in 2026?

According to New Zealand’s Financial Markets Authority, insurers have been required since 31 March 2025 to hold a financial institution licence and publish a fair conduct program outlining how they treat consumers throughout the claims process. Additionally, the IFSO’s Fair Insurance Code requires insurers to update customers at least every 20 business days during claim delays – including during catastrophe events. Together, these obligations make communication and transparency a formal regulatory requirement, not a discretionary service commitment.

What does it take to become a top-rated insurance claims carrier year after year?

Sustaining top-rated status requires consistent broker satisfaction year on year – not a single strong performance. The insurance claims carriers that appear repeatedly demonstrate embedded operational practices: dedicated case ownership, specialist expertise by claim type, proactive communication systems, disciplined surge capability for catastrophe events and a feedback loop between claims outcomes and underwriting decisions. These are structural investments that compound in value over time and cannot be replicated quickly by competitors who have not made them.

Methodology

To determine the 5-Star Claims insurers for 2026, Insurance Business conducted a comprehensive research process, leveraging its national network of brokers and industry professionals. Insurers that received a sufficient volume of broker nominations were then invited to complete a detailed submission. This submission required insurers to provide supporting evidence of their claim's capabilities, including service standards, claims turnaround times, dispute resolution processes, technological innovation and broker support frameworks.

The research team analysed both quantitative survey results and qualitative insurer submissions. Final scores were calculated based on broker ratings across key performance indicators, with additional weighting applied to consistency of service and demonstrated outcomes.

The 5-Star Claims designation was awarded to those organisations that achieved outstanding broker ratings while also demonstrating excellence in claims management, operational efficiency and broker engagement.

Keep up with the latest news and events

Join our mailing list, it’s free!