El Niño has been declared in the Pacific, with conditions expected to intensify into what is being described as one of the strongest on record, according to Earth Sciences New Zealand. The development reflects sustained warming in equatorial sea surface temperatures and associated atmospheric circulation changes consistent with a defined El Niño-Southern Oscillation (ENSO) warm phase. The declaration follows a broader pattern of Pacific Ocean anomalies consistent with weakening trade winds and persistent temperature departures in the central and eastern tropical Pacific. These indicators are commonly used in seasonal risk frameworks due to their influence on Southern Hemisphere weather variability, including New Zealand rainfall distribution and storm track patterns. The declaration is treated as a confirmed entry point into an ENSO phase within existing catastrophe modelling systems, rather than a standalone loss driver or pricing trigger.

Forecasting agencies in New Zealand indicate El Niño conditions are likely to strengthen through winter, with continued ocean-atmosphere coupling supporting persistence into spring. NIWA has noted that winter 2026 may mark the early establishment phase of a more defined El Niño pattern, with increasing confidence as coupled climate signals stabilise. Earth Sciences New Zealand has also described current conditions as consistent with the development of a “formidable” El Niño event, based on observed Pacific Ocean anomalies and modelled ENSO evolution. Forecast confidence increases as ENSO conditions mature, although outcomes remain probabilistic and dependent on atmospheric feedback mechanisms.

The El Niño declaration arrives in a New Zealand insurance market that has already experienced a step-change in natural hazard loss experience. According to the Insurance Council of New Zealand (ICNZ), the 2023 Auckland Anniversary Weekend floods and Cyclone Gabrielle generated approximately $3.8 billion in insured losses and over $14 billion in total damage, marking the largest insurance-related weather events in the country’s history.

ICNZ data also shows a sustained upward trend in weather-related insured losses over recent years, with multiple record-loss years occurring in the past decade. More recent industry analysis indicates that although 2024-2025 insured losses were comparatively lower following the 2023 outlier year, storm frequency and claim volumes remain elevated relative to longer-term averages. This positions the current El Niño phase within a post-2023 structural reset in NZ nat cat risk pricing and capital allocation, rather than within a historically “normal” baseline.

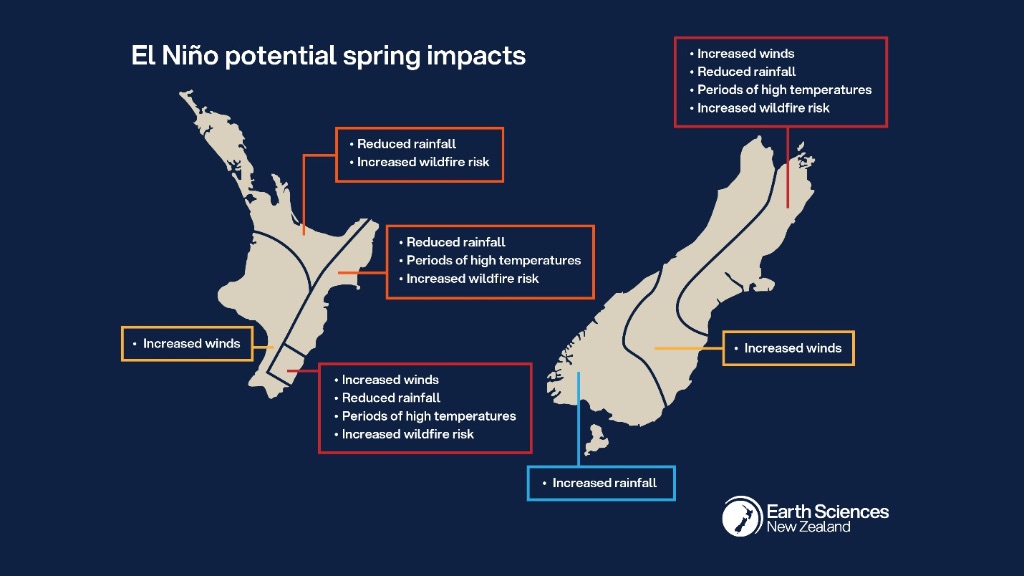

El Niño phases are typically associated with shifts in rainfall distribution, temperature variability, and storm track positioning across New Zealand. Historical patterns indicate potential for reduced rainfall tendencies in parts of eastern regions and more variable precipitation in western areas. For insurance portfolios, these shifts remain relevant where exposure is sensitive to:

However, realised loss outcomes continue to be driven primarily by event clustering, localised meteorological systems, and exposure concentration, rather than ENSO phase strength alone.

Despite heightened monitoring of ENSO conditions, there is no consistent evidence of structural change in underwriting appetite, pricing frameworks, or reinsurance attachment behaviour at the onset of El Niño phases in New Zealand markets. Instead, insurers and reinsurers continue to operate within post-2023 recalibrated catastrophe environments, where extreme weather events have already materially influenced risk assumptions and capital modelling baselines.

Industry and regulatory commentary from ICNZ highlights that global reinsurers are increasingly focused on long-term certainty, policy stability, and sustained adaptation investment as prerequisites for maintaining resilient insurance markets in high-risk regions. Within this framework, El Niño is incorporated as:

In practical terms, ENSO influences monitoring intensity and scenario calibration rather than altering core pricing structures or capacity deployment.

The El Niño phase is emerging into a New Zealand insurance market already operating under sustained natural hazard pressure, where climate-driven loss volatility is increasingly embedded within pricing frameworks, capital planning, and risk governance structures. Regulatory and climate risk assessments reinforce this structural environment. The Climate Change Commission’s 2026 National Climate Change Risk Assessment identifies elevated and compounding natural hazard risks across the economy, requiring coordinated adaptation and risk governance responses across sectors, including insurance.

ICNZ has similarly emphasised that recent large-scale weather events have shifted the industry into a higher baseline risk environment, where adaptation and resilience investment are necessary to maintain long-term insurability. Within this context, El Niño functions as a short-term variability signal layered onto an already structurally adjusted catastrophe risk baseline, rather than a driver of immediate repricing or capacity withdrawal.

Climate agencies are expected to continue monitoring ENSO evolution through winter and into spring, with forecast confidence increasing as ocean-atmosphere coupling stabilises. For insurers and reinsurers, the current El Niño phase provides a scenario-conditioning signal for potential variability in hazard clustering across property, agricultural, and infrastructure portfolios. However, current market practice indicates that:

As a result, El Niño is best understood as an operational risk signal within an already elevated catastrophe risk regime, rather than a discrete driver of market behaviour change.