Long-term care insurance is currently unavailable in the country, with the government mostly shouldering the responsibility of financing aged care. A recent report published by the Royal Commission, however, has revealed that this funding is not enough to provide quality care, highlighting the need for private long-term care insurance in Australia.

In this article, Insurance Business takes a deeper look at the country’s aged care system and the role long-term care insurance may play in helping the nation’s senior population access the care they require. We will also discuss how much long-term care costs and how the current system is funded.

If you’re planning for your own care or helping an older family member, this piece can give you a rundown of the different options available. Meanwhile, if you’re among the insurance professionals who frequent our website, you can use this article to educate your clients about the benefits of having long-term care insurance in Australia.

The Royal Commission’s recent report on the state of aged care in the country emphasises the need for long-term care insurance in Australia. This type of policy can help families cover the different services given to older people who lost the ability to care for themselves due to age-related impairments.

While aged care services are subsidised by the government, the Royal Commission’s report has found that the funding is not sufficient to provide the country’s older population with quality care. And with the exorbitant cost of long-term care services, these can easily drain one’s retirement savings, which makes having long-term care insurance in Australia vital in helping seniors access the best care possible.

In countries such as the US and Canada, long-term care insurance can be accessed by individuals who can no longer perform two out of the six activities for daily living or ADLs. These are:

Long-term care insurance often requires policyholders to pay for care services for a certain timeframe, called an elimination or waiting period. This usually spans between 30 and 90 days, after which the insurer starts the reimbursements. Plans also pay out a capped amount each day until the lifetime maximum is reached.

In place of long-term care insurance in Australia, the aged care system is designed to support members of the country’s older population who can no longer live in their own homes without assistance. The table below lists some of aged care services that older Aussies can access.

The government acts as the primary funder and regulator of the aged care system as set by the Aged Care Act of 1997. Figures from the Department of Health and Aged Care (DHAC) show that the government spent $24.8 billion for aged care in the last financial year, which if broken down consisted of:

Overall, an estimated 1.5 million Australians benefitted from some form of aged care coverage, with an overwhelming majority receiving home care, which comprises:

Only a fraction, or 245,719, of the beneficiaries were in permanent residential aged care or assisted living care.

Aged care services are provided by the government, non-profit organisations, and private companies. The level of care given varies depending on the person’s needs. These come in four main types, namely:

Older Aussies are given entry-level support services, while carers are provided with respite services through the Commonwealth Home Support Programme (CHSP). This scheme is designed to allow people to have some form of independence while living in their own homes through various care services, including:

To be eligible, a person must be:

But because the CHSP caters to a large number of individuals, the programme can only provide a limited amount for each, which on average was at $2,949 worth of services based on the latest DHAC figures. As a result, clients may have to pay a contribution towards the cost of services, with the amount varying between providers.

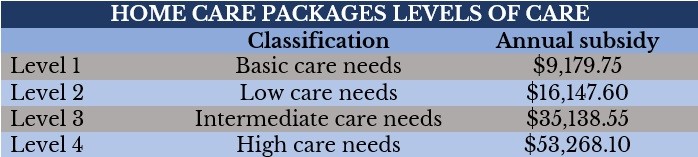

For older Aussies who need a higher level of support to continue living at home, they can access the Home Care Packages (HCP) Programme. Compared to the CHSP, the HCP provides more comprehensive care and support services for those wanting to maintain their independence and remain safely in their homes. Each package of services is also tailored to cater to a person’s unique needs.

There are four levels of care, with a corresponding government subsidy. These are detailed in the table below:

HCP clients work with their chosen providers to identify their care needs and determine the best way to spend the funding. The service provider can likewise coordinate and manage the services on their behalf. Clients are also expected to contribute to the cost of care if they can afford to do so. The amount consists of three types of fees:

Residential aged care services are designed for people who require care that cannot be adequately provided in their own homes. This type of care is given to individuals in aged care homes in a permanent or short-term, also called respite care, basis.

Funding for residential aged care services comes from government subsidies and contributions from the residents, who may be asked to pay a basic daily fee worth 85% of the single basic-age pension. Some residents may also need to cover a means-tested care fee based on their income and assets. Accommodation costs, meanwhile, may be fully or partially subsidised by the government, with those with greater means required to pay an “accommodation price” – previously called a bond – agreed upon with the aged care home.

Flexible care is designed for those whose needs cannot be adequately met by mainstream home and residential services. Older Aussies can access four main types of flexible care, namely:

For Indigenous Australians, culturally appropriate home care and residential aged care services are provided through the National Aboriginal and Torres Strait Islander Flexible Aged Care Program.

While the government subsidises aged care services to help citizens access affordable care, those who can afford to are expected to shoulder a portion of the cost. How much older people pay depends on a range of factors, including:

These are some of the fees that Australians may need to pay when accessing aged care services:

You can find updated standard rates on these fees through the DHAC website. Another important thing to take note of is that before a person can access government-sponsored care, they need to undergo an assessment to determine eligibility.

While the level of protection long-term care insurance can provide cannot be replaced by other types of coverage, there are some types of policies that currently exist in the market that can offer some form of financial support under similar situations. These include:

If you want to understand how long-term care insurance works and learn why it is an important form of coverage, you can check out our comprehensive guide to this form of coverage.

Do you think it is beneficial to have long-term care insurance in Australia? Why or why not? Feel free to share your thoughts in the comments box below.