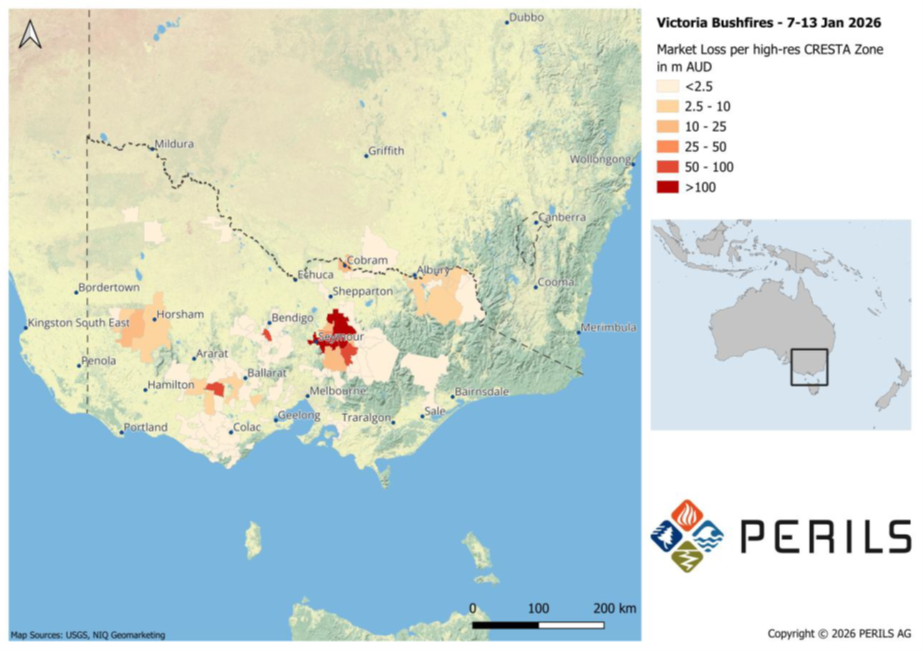

When PERILS AG released its third industry loss estimate for the January 2026 Victoria bushfires on July 14, 2026, the topline figure – $860 million – told part of the story. The more consequential number sits inside it: 68% of that loss fell on commercial lines. Agriculture Victoria data helps explain why. The split – commercial lines property at 68%, personal lines property at 30%, and motor hull at 2% – is atypical for an Australian bushfire event and carries direct implications for how the market models, prices, and aggregates rural commercial exposure.

The January 2026 fires were not a repeat of the 2019-20 Black Summer in hazard type or loss distribution. PERILS head of Asia-Pacific Darryl Pidcock drew the distinction in an earlier report: “This event differed from the 2019-20 fires as it occurred primarily in grassland areas, fuelled by extremely dry grasses, intense winds, with fires moving at up to 25 kmph at their peak.” That hazard characteristic matters for understanding the commercial lines concentration. A post-event field survey by risk modeller Risk Frontiers, conducted in February 2026 at the Longwood fireground, found that the fire footprint extended across open grazing and pastoral land, with damage including the destruction of hundreds of residential and agricultural buildings, hundreds of kilometres of fencing, and significant livestock losses. Dry grass across paddocks allowed fires to spread quickly, with embers starting fires near buildings and secondary items such as round hay bales, which then spread across open areas and contributed to impacting isolated structures.

The scale of agricultural loss across the state confirms the commercial exposure concentration was structural, not incidental. Agriculture Victoria data collected as of Feb. 13, 2026, recorded statewide losses of 45,593 livestock – including 35,807 sheep and 2,553 beef cattle – alongside 531 farm buildings destroyed, 569 vehicles and pieces of machinery lost, 9,625 kilometres of fencing destroyed, and 40,438 tonnes of hay and silage lost. Softwood plantation losses alone reached 11,136 hectares, with a further 188 hectares of wine grapes and 108 hectares of apple and pear orchards affected. That loss profile – spanning stored commodities, farm infrastructure, orchards, and working machinery across 150,518 hectares of affected farm area – sits predominantly within commercial lines coverage, not personal lines. It provides a direct evidential basis for the 68% commercial share that the PERILS headline figure alone does not.

The Insurance Council of Australia (ICA) declared a Significant Event on Jan. 11, 2026, activating claims data collection and industry coordination processes. The declaration was escalated to an Insurance Catastrophe on Jan. 16, with 2,369 claims lodged across property, commercial, and motor lines at that point, and around 30% of all property claims assessed as total losses. As of Jan. 28, the ICA reported more than $200 million in insured losses from 3,123 lodged claims, spanning home and contents, motor, commercial, and business interruption policies. By May 2026, more than 4,700 claims had been lodged in total.

The PERILS loss estimate has tracked upward across each reporting interval: $786 million at six weeks, $810 million at three months, and $860 million at six months – a cumulative increase of 9.4%. A fourth and final estimate is due Jan. 13, 2027. Commercial lines claims, which typically take longer to resolve due to business interruption components and complex asset valuations, are likely to drive further development before that date.

For catastrophe modellers and reinsurance buyers, the commercial lines concentration raises a specific technical question: whether current Australian bushfire event sets adequately represent the exposure profile of fast-moving grassfires across agriculturally dense regions, as distinct from the forest canopy fire scenarios that shaped model development after Black Summer. Risk Frontiers’ field observations from the Longwood fire confirmed that building losses extended well beyond the immediate bushland interface, reflecting long-range ember attack and grassfire spread – a pattern that differs from more forest-dominated fire events.

PERILS product manager Luzi Hitz noted in a February 2026 report that “after six years of mainly ‘wet’ cat events in Australia, including floods, cyclones, and severe convective storms, the 2026 Victoria bushfires serve as a reminder of the significant bushfire risk in Australia.” Pidcock added that the postcode and coverage-type breakdown in the July release is intended to enable a better understanding of the damage caused and support the ongoing development of bushfire models.

A Victorian parliamentary inquiry into the 2026 summer fires is underway, with a report due July 28, 2026. Its findings on agricultural losses, infrastructure damage, and emergency response are expected to inform regulatory and land-use planning discussions with implications for the broader insurance market. The PERILS final estimate, due Jan. 13, 2027, will provide the most complete view of commercial lines development once the majority of claims have settled.