Health insurers, medical associations, and not‑for‑profit funds are calling on the federal government to reconsider plans to reduce the private health insurance rebate for Australians over 65, saying the change could prompt older, low‑income members to reduce or drop cover and shift more demand to public hospitals. The proposal, outlined by Health Minister Mark Butler ahead of the federal budget, would remove the higher age‑based rebate tiers at 65 and 70 so that older Australians receive the same percentage rebate as younger policyholders.

The government plans to direct the savings to aged care and has described the measure as supporting intergenerational equity. “Right now, we subsidise private health cover for Australians over 65 at a higher rate than other Australians. That’s not fair between generations,” Butler said, as reported by 9News. He said the rebate shift is intended to free up “precious taxpayers’ dollars” for aged care services, acknowledging the changes “would not be welcomed by all” but arguing it was “the right thing to do.”

Private Healthcare Australia (PHA), which represents the majority of private health insurers, is urging the government to limit the impact on retirees on modest incomes, including aged pensioners and part‑pensioners. “About 39% of Australians with private health insurance earn less than $55,000 a year. This includes more than 900,000 older Australians who will be affected by the government’s proposed changes announced yesterday as part of its aged care cost‑of‑living measures,” PHA chief executive Dr Rachel David said.

David said many in this group have annual incomes under $30,000 and live outside inner metropolitan areas. PHA figures indicate that around 2.6 million Australians aged 65 and over hold hospital cover, with about 70% living outside inner metro districts and 27% in rural electorates. According to PHA, this points to extensive use of private cover among older Australians in regional and rural communities. Government modelling reportedly suggests around 44,000 people may leave private health insurance under the changes. David said the people most likely to exit or downgrade policies are those with greater healthcare requirements. “The public hospital system is already under pressure and cannot provide timely care for many of these patients. That’s precisely why they rely on private health cover to manage their health,” David said.

PHA supports reducing rebates for retirees on higher incomes, including those earning six‑figure sums, consistent with its budget submission. However, the association is advocating an income‑based approach that preserves higher rebates for low‑income members and is pressing for broader reform to address system costs. “There is a large cohort of older Australians with chronic conditions who rely on the private system and already devote a significant share of their limited incomes to their healthcare. It is economically counterproductive to reduce the rebate and push high‑needs patients out of private cover. This will increase pressure on public emergency departments, public hospital beds, and elective surgery waiting lists, which are already struggling,” David said.

PHA has proposed a package that would:

PHA estimates that this package could achieve around 70% to 75% of the government’s revenue target while “significantly improving equity” and argues that reforming device pricing should be a priority. David said: “Many medical devices cost between 30% and 100% more in Australia than in comparable markets such as New Zealand. As a first step, aligning prices for common devices with New Zealand benchmarks could save consumers around $300 million a year.”

Members Health Fund Alliance, representing more than 20 not‑for‑profit and member‑owned funds, is also asking the government to pause the measure and broaden consultation, citing projected premium increases for older policyholders and additional costs for the public system. Chief executive Matthew Koce said internal analysis indicates the removal of higher age‑based rebates would have a concentrated effect on premiums for seniors. “Analysis indicates premiums would increase by around 5% for people aged 65-69, and by up to 11% for people aged over 70, the equivalent of around three years’ worth of premium increases in a single year. For a senior household paying an annual premium of around $6,000 before rebates, this would mean an increase of approximately $240 per year for people aged 65-69 and nearly $500 per year for those aged over 70,” Koce said.

Koce referred to actuarial modelling commissioned by the government that found removing higher rebates for Australians over 65 would reduce rebate expenditure by about $482 million while adding approximately $547 million in costs to the public hospital system. “The higher rebate tiers for those over 65 and over 70 are not a luxury; they are a critical affordability bridge for low‑ and middle‑income retirees on fixed budgets who are facing the highest health risks of their lives,” he said. Members Health has argued that a sizeable reduction in older membership could affect private hospitals’ revenue base, particularly for elective surgery categories such as hip, knee, and cataract procedures, and increase caseloads in public hospitals.

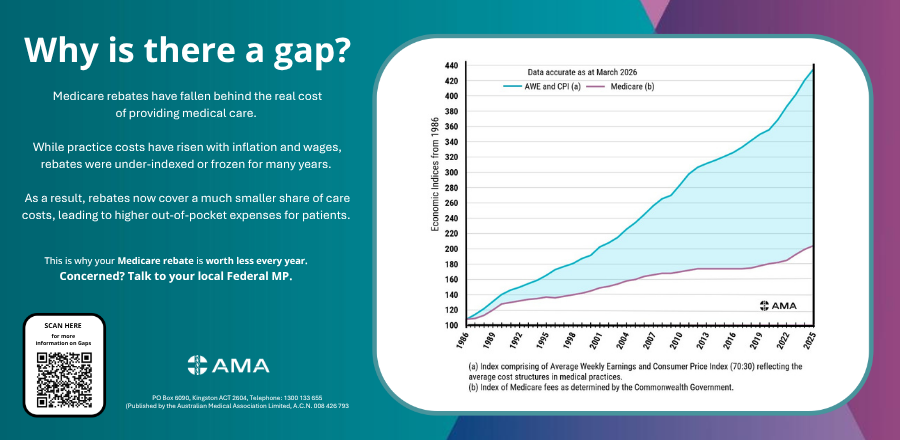

The Australian Medical Association (AMA) is linking the rebate discussion to wider funding and benefit settings, emphasising long‑term Medicare rebate indexation trends and practice costs as key factors in out‑of‑pocket charges. Releasing a new “Gaps Poster,” AMA president Dr Danielle McMullen said inflation and operating costs have outpaced the Medicare indexation rate. “We have had decades of under-indexation, and half a decade of a Medicare freeze, leaving the rebate woefully out of reach of covering the cost of care,” McMullen said. She said recent changes to bulk‑billing incentives have improved access for some patients but apply to “a tiny fraction” of the more than 5,000 Medicare Benefits Schedule items. “These are ‘bolt-on’ incentives, not Medicare reform. And they don’t do anything if you need to see a specialist for a consultation, a privately billing GP, or need surgery,” she said.

In non‑GP specialist care, the AMA is calling for increases in Medicare rebates, reform of no‑gap and known‑gap arrangements in private health insurance, improved indexation and transparency of insurers’ rebate schedules, and a higher proportion of premium revenue being paid back into healthcare. The association is also seeking greater investment in public hospital outpatient clinics to support access through both public and private settings. McMullen said that without broader reform, “the gaps will only continue to grow, further impacting patients.”

Separate analysis by comparison site Canstar, reported by 9News, examines the combined impact of the proposed rebate changes and the 2026 premium round on older policyholders. On gold hospital policies, Canstar estimates that aligning the rebate for those over 65 with younger cohorts would add about $205 a year for people aged 65-69 and $410 a year for people aged 70 and over. On basic cover, the corresponding increases are estimated at $53 and $105 a year.

These changes would follow an average 4.41% premium increase that took effect on April 1. Taken together, the analysis suggests older members could pay between $136 more a year on basic policies and up to $815 more a year on gold policies. “It’s a potential double whammy that many older Australians won’t be able to afford, particularly those on modest fixed incomes. Some may even be forced to reconsider the level of cover they hold,” Canstar data insights director Sally Tindall said, as reported by 9News. Based on Australian Bureau of Statistics (ABS) estimates cited in the analysis, around 4.4 million Australians aged over 65 could be affected by the rebate alignment.