Australia’s largest listed entities are acknowledging climate-related risks to earnings and capital but, in many cases, are only beginning to quantify those exposures, leaving gaps for insurers, reinsurers, and institutional investors seeking to assess financial materiality.

Sustainability consultancy ERM has reviewed 33 climate disclosures lodged by Australian companies that report on a calendar-year basis under the new Australian Sustainability Reporting Standards (ASRS). The regime, which will phase in to 2028, requires large entities to disclose climate-related risks alongside greenhouse gas (GHG) emissions. ERM’s analysis indicates that about two-thirds of early reporters have identified at least one climate risk as material to their business. Fewer than one-third, however, have set out quantified estimates of how those risks could affect earnings, balance sheets, or cash flows. As a result, insurers and capital providers are receiving formal recognition of climate risk but limited consistent financial metrics for use in underwriting, risk modelling, and investment decisions.

Where companies have quantified exposure, ERM estimates that the early filers have reported between $2.5 billion and $4.5 billion in annualised climate-related financial risk. ERM notes that this represents only a portion of the total climate risk that has not historically been disclosed in financial or sustainability reports. “Australia’s mandatory climate reporting regime is doing exactly what it is designed to do, it’s getting the climate conversation tabled in the boardroom. Now companies have publicly acknowledged the financial risks associated with climate change, the next step is to build a strategy to remain profitable in world that is decarbonising and physically changing, and back their commitments with a credible transition plan,” said Dr Mary Stewart, ERM lead partner, corporate sustainability and climate change ANZ.

According to ERM’s review, many companies that have identified material climate exposures have not yet aligned capital allocation or governance settings with those risks. In most cases, the consultancy found little or no capital specifically set aside for adaptation, physical risk management, or transition investments, and few examples where climate indicators are integrated into executive remuneration, internal pricing, or capital planning frameworks. “Investors in particular need decision-useful information, and the onus is on reporters to quantify the risks they are declaring as material, including financial impacts, and explain how they intend to mitigate them,” Stewart said.

ERM also observed that most early reporters have deferred complex value chain reporting. Around three-quarters relied on first‑year exemptions to postpone quantifying Scope 3 emissions, leaving major elements of transition exposure outside current public disclosures. “The important work of quantifying Scope 3 emissions can also not start soon enough. Given the scale of these value chain emissions for most businesses, this is both a major gap in Australia’s climate disclosure landscape and an opportunity for businesses, opening the door to a materially stronger position with investors and customers,” Stewart said. The deferral of Scope 3 reporting may delay fuller visibility into counterparties’ supply chain and product-use emissions, which can influence transition risk, potential liability, and long‑tail exposure across portfolios.

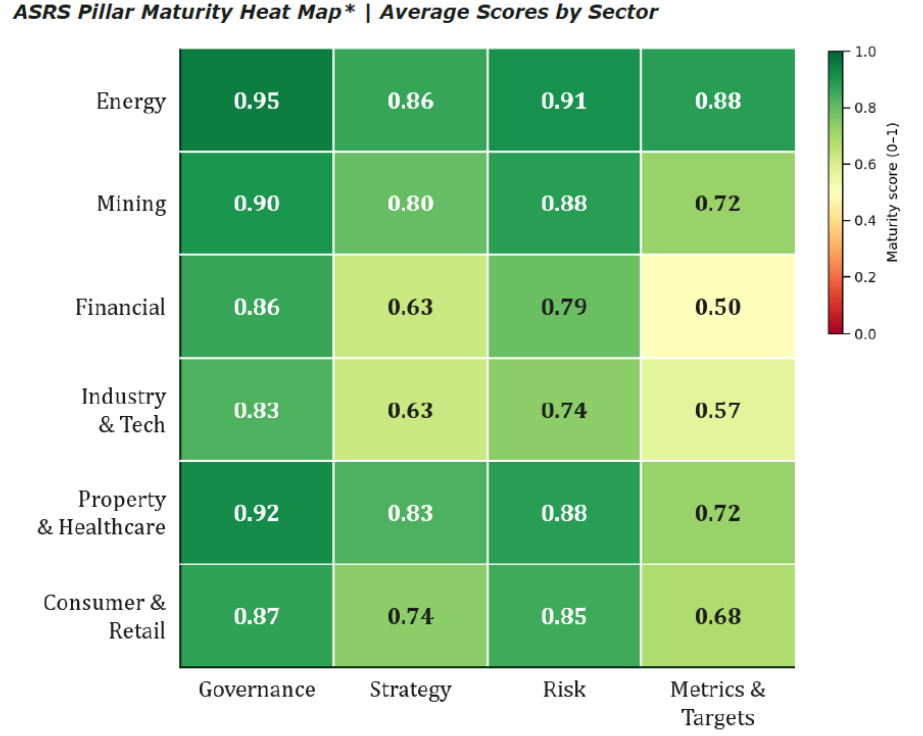

ERM scored the disclosures against four pillars – governance, strategy, risk management, and metrics and targets – and assessed both the presence and usefulness of reported information. Energy and mining companies, which have been under transition scrutiny for longer, are described as further advanced in quantifying climate-related financial exposures, linking those exposures to capital expenditure, and incorporating climate-related indicators into executive pay frameworks. By contrast, financial services entities – including banks and other financial institutions – were assessed as having comparatively developed governance structures, but lower scores on metrics and targets that indicate whether climate risks are being actively managed.

“Climate disclosure maturity reflects proximity to risk. Energy and mining companies have been living with transition pressure for years, and that shows up in a more sophisticated understanding of climate risk and a more strategic approach to managing it. For financial services the exposure is just as real, but the urgency to act just isn’t there from some of the early reporters. This should worry investors,” Stewart said. For general insurers and reinsurers, the variation suggests that large emitters may be providing more detailed transition information than some financial counterparties, affecting how different sectors can be assessed from an underwriting and counterparty risk perspective.

ERM’s assessment points to several areas where practice is developing. Boards are increasingly identified as accountable for climate risk, governance structures have become more defined, and disclosure of Scope 1 and 2 emissions – often with external assurance – is becoming more common. Many companies have also started to use international climate scenario frameworks, such as those of the IPCC, to test their strategies. However, ERM found that climate considerations are not yet consistently driving key business and capital decisions. Only a minority of early reporters have explicitly linked executive pay to climate-related outcomes, and in many cases the connection between risk identification and capital deployment, business model adjustments, or portfolio changes is limited.

“The gap between identified climate risk and capital deployed to address it is stark. Companies are disclosing significant financial exposures in one breath while allocating next to nothing to address it in another. That is not a disclosure challenge, it is a governance challenge,” Stewart said. She said the first year of mandatory reporting “was never going to be perfect,” and that the presence of significant unquantified risks and incomplete transition plans illustrates the rationale for the regime.

The initial ASRS reports are being released against a backdrop of inflationary pressure, energy market volatility, and geopolitical uncertainty. Stewart said entities that have mapped supply chain exposure, stress‑tested their business models, and developed climate adaptation capabilities are better positioned under these conditions. “Volatility in energy markets and escalating geopolitical uncertainty are not a reason to delay climate investment; they are the business case for it playing out in real time. Companies that did the work early are structurally more resilient. That is not a coincidence. Done well, climate risk disclosure is the foundation of business resilience and long-term performance. It is not a compliance or box-ticking exercise,” Stewart said.

ERM is encouraging investors to use AGM season to question boards on how climate risk is being addressed. Suggested topics include whether climate risk discussions go beyond emissions management to cover physical impacts; whether financial exposure has been quantified; how climate risk is integrated into strategy, executive pay, and capital deployment; the existence and status of a transition plan with defined timelines and accountability; and when deferred Scope 3 and value‑chain disclosures will be released. “What these first mandatory climate disclosures reveal is both encouraging and confronting. Governance is in place, but translating risk into strategy, capital, and accountability has just begun. Companies are recognising climate risk but still treating it as a future problem or viewing transition and physical risk as challenges to be tackled one after the other. They are not. Both demand a response now,” Stewart said.