Older Australians could face a health insurance bill shock under rebate changes, with analysis from Private Healthcare Australia (PHA) indicating that from April next year senior policyholders may see premium rises up to three times higher than those for younger members, and some retirees facing annual increases of more than $1,600.

The projected increases are linked to the Albanese government’s plan to remove the higher private health insurance rebate rates currently available to people as they move into older age brackets. Under existing arrangements, the means‑tested rebate steps up at ages 65 and 70, reducing net premiums for seniors. The government has signalled it wants to flatten these age-based tiers as part of a savings measure of around $3 billion for the federal budget.

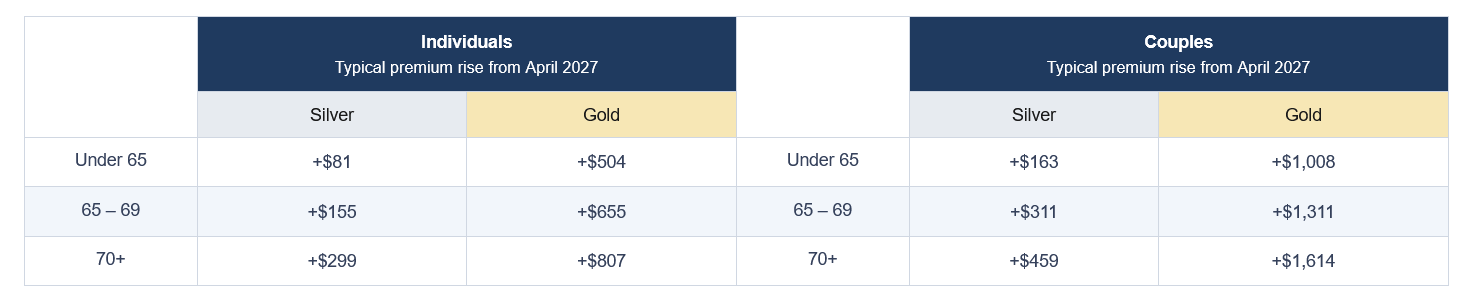

PHA says its modelling shows that, if the proposal proceeds, hospital cover will become significantly more expensive for those most likely to use it. For Australians aged 70 and over with gold hospital cover, PHA projects premium increases of more than 21% from April 2027, compared with around 4% for people under 65 on equivalent products. On a couples’ gold policy, the peak body estimates an increase of about $1,614 a year for households where the oldest partner is 70 or older. For single seniors on gold cover, the modelled rise is $807 a year.

“These are Australians who have done exactly what governments encouraged them to do – maintain health cover throughout their lives so they can access private healthcare and take pressure off the public system. Now, just when they need their hospital cover most, they are being singled out for the biggest price increases we’ve ever seen,” PHA chief executive Dr Rachel David said. PHA estimates more than 3 million Australians aged over 65 hold private cover, including over 400,000 pensioners, and says many older members have limited capacity to absorb higher net premiums.

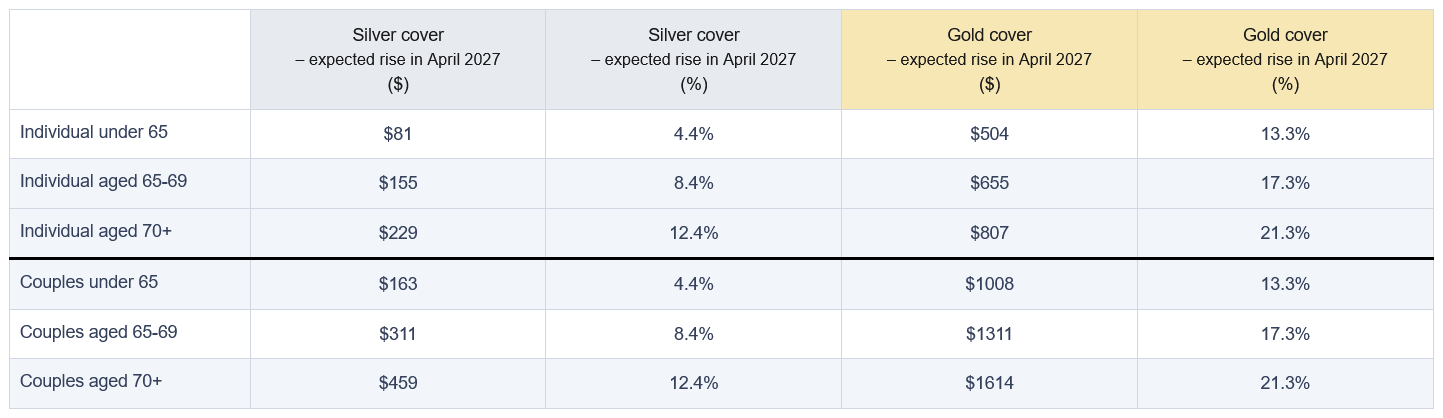

The PHA analysis draws on typical silver and gold hospital policies identified in Canstar market data, combined with recent premium trends in which gold products have recorded larger base increases than other levels of cover. The scenario assumes an industry‑wide premium change on April 1, 2027, and then applies the impact of removing the extra rebate support for older age groups. For individuals with silver hospital cover, PHA estimates indicative annual premium rises of $81 (4.4%) for those under 65, $155 (8.4%) for those aged 65 to 69, and $229 (12.4%) for people aged 70 and over. For gold cover, the modelled increases for singles are $504 (13.3%), $655 (17.3%), and $807 (21.3%) across the same age bands.

For couples, silver-tier premiums are projected to rise by $163 (4.4%) for those under 65, $311 (8.4%) for couples aged 65 to 69, and $459 (12.4%) where at least one partner is 70 or older. On gold couples’ policies, the estimates are $1,008 (13.3%), $1,311 (17.3%), and $1,614 (21.3%). Under current rules, the rebate percentage on a couples’ policy is determined by the age of the older adult insured. David said these changes could force difficult choices for retirees reliant on the age pension, superannuation drawdowns, or savings. “For some older Australians this will mean choosing between paying for health insurance or dropping cover altogether. When seniors leave private health insurance, the pressure doesn’t disappear. It shifts straight onto already stretched public hospitals which ultimately costs taxpayers more,” David said.

PHA has also said it expects potential downgrades among older members, particularly out of gold products that commonly cover procedures such as joint replacements, cardiac care, cancer treatment, and cataract surgery. The organisation points to earlier economic assessments suggesting the rebate delivers a net fiscal benefit to government by reducing use of public hospital services. David cited 2023 work by University of Newcastle researchers that found “on average, the Australian government saves $554 for each person it helps with its health insurance subsidies per year.” She said: “Policies that push older Australians out of private cover ultimately increase waiting lists for everyone.” PHA has called for current rebate settings to be retained for low‑income Australians over 65 earning less than $55,000. “Older Australians have kept their side of the deal. They should not be asked to balance the Budget at the expense of their healthcare security,” David said.

Members Health Fund Alliance, which represents more than 20 not‑for‑profit and member‑owned health funds, takes a similar view, saying that cutting higher rebates for seniors is likely to increase overall government health spending by shifting demand to the public system. “Removing the private health insurance rebate for older Australians is likely to cost the Government much more than it saves. This is a drastic policy change that will hurt older, lower‑income Australians who have been loyal insurance members,” Matthew Koce CEO of Members Health said.

Members Health analysis suggests that if the age-based rebate tiers are removed, premiums would increase by around 5% for people aged 65-69 and by up to 11% for those over 70. For a senior household paying about $6,000 in annual premiums before rebates, Koce said this would translate to an extra $240 a year for people aged 65-69 and nearly $500 a year for those over 70. The alliance cites government‑commissioned actuarial modelling which it says found that removing the higher rebates for Australians over 65 would cut rebate outlays by about $482 million but add around $547 million to public hospital costs as more older patients rely solely on the public system.

“You cannot fix aged care by breaking the private health system, yet that is exactly what this policy threatens to do. The government is effectively treating ageing as a financial liability. It’s a kick in the teeth for senior Australians who have worked hard, paid their taxes, and maintained private health cover for decades to ensure they wouldn’t be a burden on the public system. The higher rebate tiers for those over 65 and over 70 are not a luxury; they are a critical affordability bridge for low‑ and middle‑income retirees on fixed budgets who are facing the highest health risks of their lives,” Koce said. He said a significant exit of older members or shift to lower levels of cover could have flow‑on effects for private hospitals, which perform most elective procedures such as hip and knee replacements and cataract operations. Members Health has called on the government to halt the proposal and undertake broader consultation with funds, hospitals, and consumer groups.

The Australian Medical Association (AMA) has separately raised concerns about the value of private health insurance for consumers and the way the sector is regulated. Federal AMA president Dr Danielle McMullen said a strong private hospital sector helps manage pressure on public hospitals and supports patient choice, but pointed to trends that, in the association’s view, have reduced value for consumers. “A massive 68% of hospital policies now contain exclusions, which means Australians are paying more for less. And the ratio of premiums revenue being paid out by insurers to cover patients’ treatment has dropped in recent years, and in 2024-25 was only 84%,” McMullen said.

In its 2026-27 pre‑budget submission, the AMA is calling for the introduction of a minimum pay‑out ratio of 90% of premium revenue returned as benefits, arguing this would support both patients and private hospitals and may improve confidence in insurance products. The AMA is also seeking minimum payable benefits for hospital‑in‑the‑home and home rehabilitation in the private sector, supported by legislation to maintain clinical autonomy, protect patient safety, and preserve patient choice. McMullen has raised concerns about insurer‑owned care models that “funnel patients to the insurer’s own services and this vertical integration ultimately restricts patient choice and access.”

To address what it sees as fragmented regulation, the AMA has proposed an independent private health system authority to bring together oversight functions currently spread across different agencies and separate the government’s policy role from day‑to‑day regulation. “An independent body would have the objectivity and expertise to oversee reform while balancing the interests of patients, hospitals, insurers, and doctors,” McMullen said.