5-Star Cyber 2023

Jump to winners | Jump to methodology

The great cyber boom

Cyber is a rapidly expanding sector of the British insurance industry and shows no signs of abating.

IBUK’s 5-Star Cyber winners are at the forefront of this, creating the right infrastructure for this increasingly important category.

“The markets are growing very quickly, and that awareness is something that’s really accelerated in the last 12 months or so,” says Mike Smith, a partner at Bain & Company London. “That rapid growth is also being accompanied by the rapid maturing of the product suite, and it’s one of the reasons why, I think, we’ve seen quite a lot of investment capital going into some of the providers in this sector.”

Tom Simcox, the founder and managing director of Simcox Brokers, a cyber specialist, adds, “There are several factors driving the demand for cyber insurance in the UK, including the increasing frequency and sophistication of cyber attacks, the growing reliance of businesses on technology and the internet, and the increasing regulatory requirements related to data protection and cybersecurity.”

What separates the best from the rest?

Erica Kofie, head of cyber proposition at 5-Star Cyber winner QBE, offers a unique insight.

“A good insurance provider is one that makes decisions that help it be a sustainable provider of insurance; one able to provide a stable, consistent product and service through all cyber market events.”

Therefore, according to Kofie, it’s important for cyber insurance providers to maintain expertise and collaborate with their customers.

“The underwriters should partner with their clients to understand their business and be able to explain to their brokers and clients what cover they are providing, how it is applicable to the client and why they are making the decisions they do.”

For Smith, there are key fundamentals required to stand out in the sector. “It’s the limits, it’s the pricing and it’s the coverage of the scope of the risk for the covered.”

Smith also stresses the merit of going the extra mile to understand the clients’ needs.

He explains, “What a small business needs relative to a medium-sized corporation versus a large corporation is obviously very different.”

Broker relationships are critical, as Smith reveals that “most cyber insurance cover is bought, essentially, with some form of recommendation or advice,” and so providers need to be mindful of their broker support.

“And once the policy is written, it is important to be able to deliver on it as efficiently as possible,” Smith adds. “So, that’s the training and the risk management advice we’ve touched on. It’s the incident response and obviously the claims management process itself and particularly the speed with which that can be addressed.”

For Simcox, a top-performing cyber provider requires a strong reputation and a history of financial stability. This is in addition to a track record of excellent customer service and comprehensive coverage for events such as targeted extortion, ransomware and funds transfer fraud.

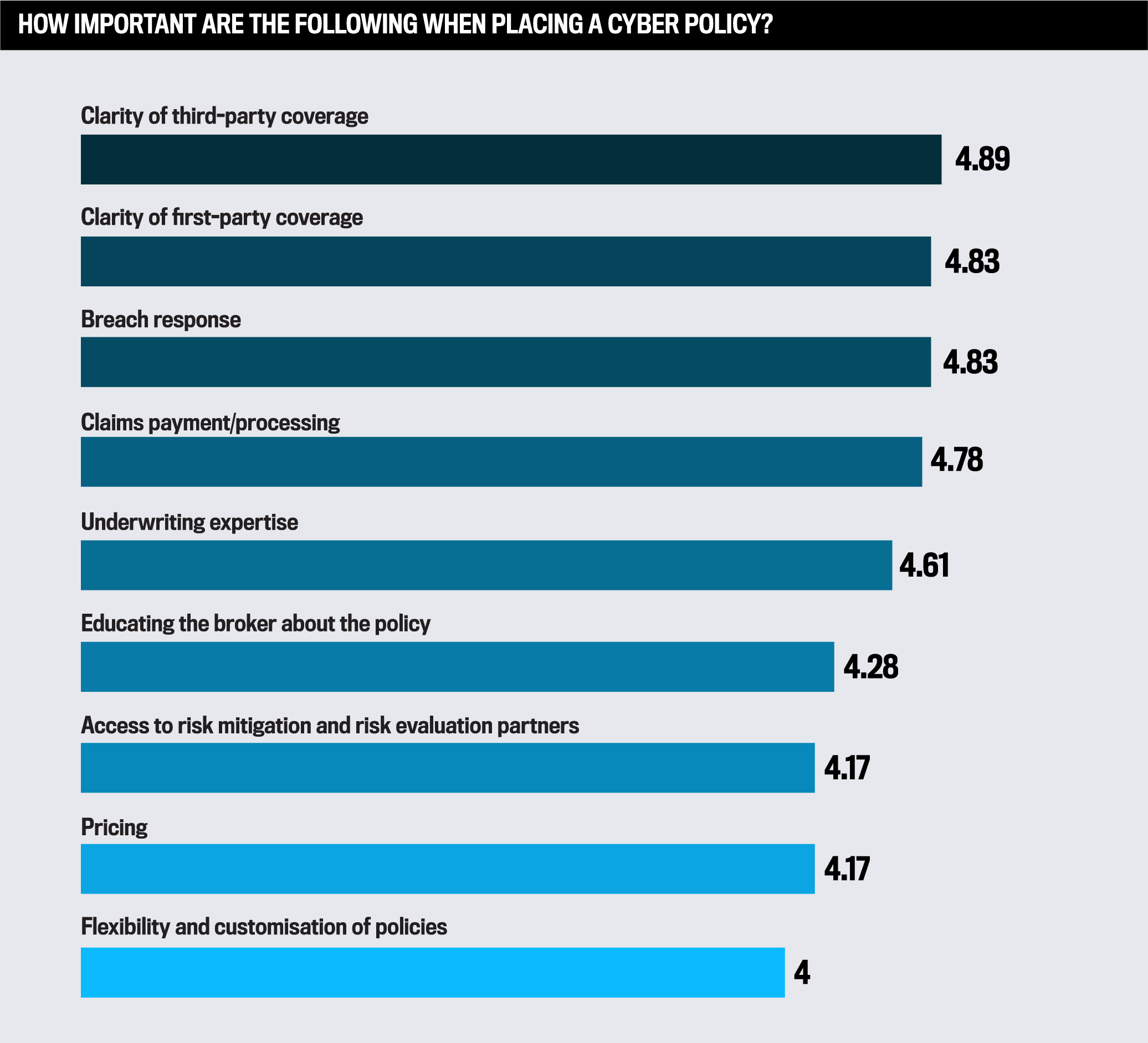

The results of IBUK’s survey align closely with Kofie’s, Smith’s and Simcox’s perspectives. In order of importance on a 1 (not important) to 5 (very important) scale, brokers ranked their top five most important categories below.

“There are several factors driving the demand for cyber insurance in the UK, including the increasing frequency and sophistication of cyber attacks, the growing reliance of businesses on technology and the internet, and the increasing regulatory requirements related to data protection and cybersecurity”

Tom Simcox, Simcox Brokers

Finer details

Those driving the UK cyber sector forward are listening to brokers.

QBE places importance on the clarity of their third-party coverage, the most important factor for brokers according to IBUK’s survey.

“Third-party liability claims are at the forefront of most cyber insurers’ minds, particularly given the relative long-tail nature of these losses compared with incident response costs,” says Kofie. “However, for some industries (specifically the legal and accounting sectors), third-party liability losses arising from cyber incidents remain covered in their PI policies, and therefore, it is important to discuss the potential overlap with your insurer, and clients should look to place both PI and cyber policies with the same insurer to ensure consistency of coverage where there may be a degree of overlap.”

This ethos is highlighted by Simcox, who advises placing importance on “clear and transparent policy terms and conditions that are easy for clients to understand and without onerous warranties.”

Also of great importance to brokers is the similar clarity of first-party coverage and breach response.

Demonstrating why QBE has been recognised, Kofie explains, “All reputable primary cyber insurers will have an incident response solution, offering their clients access to a 24/7 hotline to provide real-time assistance and support during a cyber incident.”

Meanwhile, Simcox adds that providers who stand out are able to provide “a deep understanding of cybersecurity issues and are able to provide guidance and resources to help clients reduce their risk of a cyber event and manage their premium spend.”

Another aspect Kolfie opens up about is how her firm handles claims payments and processing.

“QBE has an in-house team of cyber claims experts to work with clients and incident response vendors throughout the life span of an IT security incident.”

Brokers also value dealing with professionals who understand the sector.

Simcox highlights how “helpful and knowledgeable underwriters” are key to making a mark.

Kofie agrees, “It is important to ensure underwriters are educated on emerging threats as well as regulatory nuances in different geographies.”

Technology also has a part to play. “The technology platform that allows for what is quite a complicated product to be underwritten quickly and efficiently is really important,” adds Smith.

In addition, the education of staff is another priority, particularly as the sector becomes bigger.

“Insurers should be confident in discussing coverage and the details of the policy with brokers and clients alike,” says Kofie. “At QBE, we have worked with many of our brokers to help them understand the application of the policy to different industry clients and how the policy would respond to particular cyber events.”

“Most cyber insurance cover is bought, essentially, with some form of recommendation or advice”

Mike Smith, Bain & Company London

What more do brokers want from cyber insurers?

In the survey, brokers also offered their insights into what else they would like to see as standard practice within the UK sector. Notably, one says that it’s important to “increase flexibility and understanding around MFA [multifactor authentication]. A lot of underwriters still have a ‘no MFA, no quote’ attitude, even if a client is in the process of implementing MFA.”

“At QBE, we have allowed some clients a grace period for the implementation of MFA, understanding it was not something all companies had in place when we first started to require it,” explains Kofie. “MFA for remote access has been identified as a key defence against malicious actors seeking to gain unauthorised access to client networks. Indeed, Microsoft states that MFA can stop 99.9% of compromised account attacks. Clearly, MFA is not the silver bullet for all malicious attacks, and there are emerging threats using ‘man-in-the-middle’ tactics to circumvent MFA controls; however, it is widely considered a key element of basic cyber hygiene.”

Another broker asks that insurers “deploy meaningful capacity on a primary basis.”

“While we understand the demand for large primary capacity, the insurance market is trying to provide sustainable cover to clients,” says Kofie. “Managing capacity, particularly on a primary basis, helps insurers manage the potential volatility in their portfolios. We have seen large losses destabilise insurers’ portfolios. Larger line sizes are available when written on a co-insurance basis, although these types of placements are rare in the cyber market.”

Other brokers say providers could improve their offerings by having flexibility, keeping up with the latest technologies and advice on risk management, stopping restrictions on cover, educating the brokers, simplifying the products and training brokers so they can educate clients.

In conclusion, Kofie addresses how the industry is responding to brokers. “While the severity of claims still remains a threat, a reduction in frequency has allowed insurers to provide more pricing certainty to brokers and clients, in turn allowing them to budget more accurately, which should enhance the overall buying experience,” she adds. “If the claims trend continues, then we would expect the market to continue to become more competitive, particularly for those clients who can demonstrate mature levels of IT risk security and governance.”

“While the severity of claims still remains a threat, a reduction in frequency has allowed insurers to provide more pricing certainty to brokers and clients”

Erica Kofie, QBE

5-Star Cyber 2023

- Beazley

- Brit

- CFC Underwriting

- Coalition

- DUAL

- MPR Underwriting

- NMU

- Pen Underwriting

Methodology

To select the best cyber insurers for 2023, Insurance Business UK enlisted some of the industry’s top experts. During a 15-week process, the IBUK research team conducted one-on-one interviews with specialist brokers and surveyed more within the publication’s network to gain a keen understanding of what insurance professionals think of current market offerings.

Brokers were first quizzed on what features they thought were most important in a cyber insurance policy and then asked how the insurers they dealt with rated on those attributes. Insurers were measured on the strength of their relationships with brokers, their ability to handle claims, their underwriting expertise and, most importantly, the strength of the individual products they provide.

Keep up with the latest news and events

Join our mailing list, it’s free!