Nearly 200 insurance and protection appointed representative (AR) relationships have been terminated but consumer finance has borne the brunt of cuts amid increased scrutiny from the Financial Conduct Authority (FCA) in the wake of the Greensill Capital scandal.

In total, at least 196 general insurance and protection AR relationships have seen ties cut after supervisory engagement from the regulator since the launch of its AR department in 2022, according to a Freedom of Information request response shared with Insurance Business by the FCA.

Meanwhile, four businesses falling into the general insurance and protection sector had applied for VREQS requirements, or permission variations, as of August 31, 2023, the FCA confirmed in its FOI response.

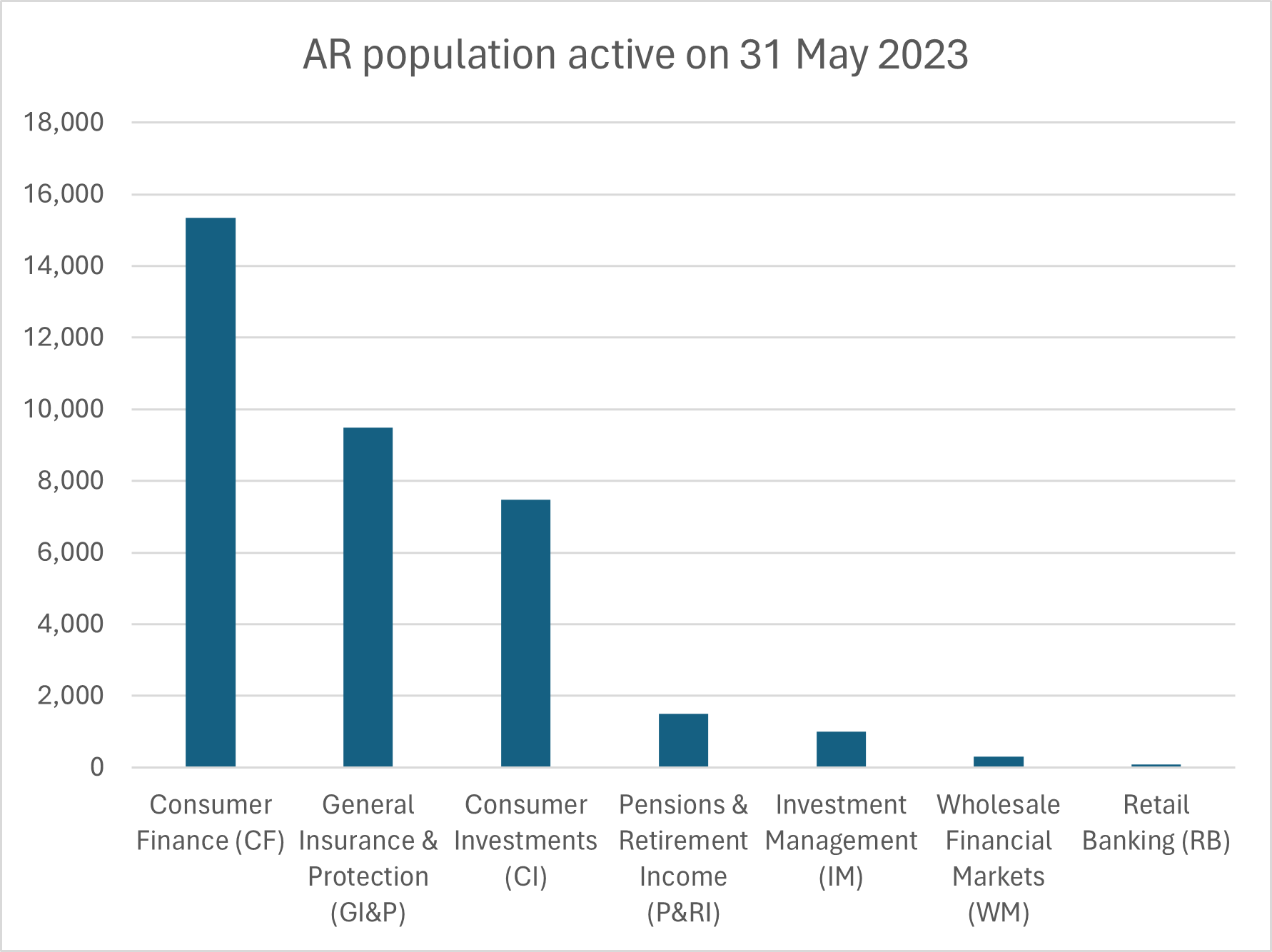

As of May 31, 2023, there were just under 9,500 ARs operating in the general insurance & protection sector.

Consumer finance, which had the most ARs of any sector at the end of May with 15,342, saw principal firms cut ties with 1,104 ARs and five firms apply for VREQs requirements as a result of the regulator’s actions, according to the FOI response.

|

Sector |

Sum of ARs Offboarded |

|---|---|

|

Consumer Finance |

1,104 |

|

General Insurance & Protection |

196 |

|

Consumer Investments |

38 |

|

Wholesale Financial Markets |

16 |

|

Investment Management |

13 |

|

Pensions & Retirement Income |

1 |

|

Retail Banking |

1 |

|

Grand Total |

1,369 |

Source: Financial Conduct Authority (FCA) response to Insurance Business FOIA request

It was in 2021 that the Treasury Select Committee published its report into Greensill Capital and called for the FCA and the Treasury to consider reforms to the AR regime, as failed lender Greensill had acted as an AR.

“Given that firms may be using the regime for purposes well beyond those for which it was originally designed, the Committee recommended that the FCA and Treasury consider reforms, with a view to limiting its scope and reducing opportunities for abuse,” the Treasury Select Committee recommended.

The FCA underwent a consultation into AR relationships in December 2021, having previously found potential harms and failings in insurance ARs during a 2016 thematic review.

Press release: We find failings in the oversight of appointed representatives in the general insurance sector https://t.co/eOoy8f9w50

— Financial Conduct Authority (@TheFCA) July 22, 2016

Firms using ARs have been found to have generated 50% to 400% more complaints and supervisory cases than other directly supervised firms, according to figures shared by FCA executive director, consumers and competition Sheldon Mills during a speech at the British Insurance Brokers’ Association’s (BIBA) annual conference in 2022.

The FCA’s AR department opened for business in 2022 to tackle “potential mis-selling and customer detriment” issues and risk management and control gaps previously identified at AR businesses.

Principal firms had to provide information about ARs by the end of February 2023, with the regulator bringing in a host of changes including a reduction in the pre-notification period for new AR appointments, requiring additional information on unregulated financial activities carried out by ARs, and changes to annual complaints reporting and revenue data sharing requirements.

Source: Financial Conduct Authority (FCA) data

As a result of changes, insurance principals with many ARs have looked to rationalise or streamline relationships to avoid the “increased regulatory burden of reporting”, according to Sue Mallender, senior consultant at regulatory and risk consultancy Sicsic Advisory.

“In some cases, it’s been necessary to reassess what the ARs are doing and removing some obsolete or legacy arrangements,” Mallender said.

Some firms have also looked to change the scope of their AR activities to make them non-regulated, for example through passive marketing rather than the regulated activity of introducing. Others have looked to alter remuneration arrangements in a bid to “circumvent” the business test for regulated activities, Mallender said.

It’s a practice that could be “high-risk” and may not lead to any “resource gain” to the firm given a level of oversight to make sure the AR does not overstep bounds would still be needed, according to Mallender.

“Under the new Consumer Duty world, the need for proper oversight of all parties who interact with customers becomes ever more important - not just for insurance, of course,” Mallender said.

The new rules should be understood as “enhancements” rather than sweeping changes, and it has always been the case that principals have been responsible for regulated activities carried out by ARs, according to Mallender.

“Good practice includes the essential aspects of good governance, e.g. formal written agreements which set out each party’s roles and responsibilities, regular monitoring and oversight with evidence and meetings,” Mallender said. “There should be ongoing, regular dialogue between principals and ARs to ensure any issues can be identified and addressed at the earliest stage, so the annual reporting and assessments become part of an ongoing monitoring arrangement, rather than a once-a-year panic.

“In essence, principals that treat their ARs as they would their internal departments in terms of understanding and oversight will do well.”

The comparatively high number of consumer finance ARs being dropped by principals could be because many consumer finance firms, such as car dealerships and retails outlets, are “generally not conducting regulated activities as part of their business”, meaning it could be harder to build the type of customer journey expected by the FCA, according to Mallender.

Another reason could be that they involve a lot of “face-to-face” interactions that are harder to monitor, Mallender said.

Insurance AR businesses can look vastly different to one another, with some only performing introducing functions (known as IARs) and others acting as full-time insurance brokers and advisors. This is an “important distinction” when thinking about how AR businesses function, according to Andy Fairchild, independent insurance consultant.

“The proposition that they offer to their end customers is fundamentally different, and that underpins everything that we’ve seen from the industry and from the regulator over the last few years,” Fairchild said.

Fairchild, a former insurance broking CEO, said the impacts of AR changes are likely to have been “largely administrative” for larger broker networks and that he “endorsed” standards changes.

“If you’re overseeing account execs at one of the big global brokers such as Marsh, or WTW, or one of the big UK consolidators, you’ve got a challenge of overseeing your account handlers on a very large level, and the standard that you employ there is one of an employee,” Fairchild said. “If you can take that into the AR regime and oversee the AR with the same sorts of standards, then that’s a fabulous principle.”

What’s your view on changes to the appointed representatives (AR) regime by the FCA in the wake of the Greensill Capital scandal? Share a comment below.