This article was created in partnership with QBE.

Cyberattacks seem to be almost a daily occurrence for organisations nowadays, with the number of incidents having increased by a staggering 104% by the end of 2024. That’s according to a recent report launched by QBE - Connected Business: digital dependency fuelling risk.

According to QBE’s research, the growing number and sheer scale of these cyberattacks are creating havoc across Europe – with high profile incidents such as the NotPetya mass cyberattack and CrowdStrike’s infamous Falcon Sensor failure in 2024 only fuelling the fire.

And it’s starting to seriously concern leaders and their teams. Data from QBE found that 78% of UK IT decision makers are concerned about the cyber threats their firms may face this year, with 47% of businesses revealing that they already suffered at least on cyber incident in the past 12 months.

Speaking to IB, David Warr (pictured), QBE insurance portfolio manager for cyber, explained that this peak in incidents is driving interest, with more and more companies beginning to see the benefits of investing in cyber insurance.

“In some parts of the world, take-up for cyber insurance has been slow but as more businesses see their competitors making use of it and see the disruption caused by events, it is spurring them on to look for coverage themselves,” he said. “CrowdStrike has contributed to changing perceptions of cyber risk and cyber protection. It has raised awareness of the types of events covered under a cyber policy, with cover provided for both security incidents as well as operational issues.”

According to QBE’s report, leaders are sizing up AI’s role in their overall cyber security – with 32% of organisations adding that they believe it will enhance their protection while 15% argue it will increase cyber risk. Because AI is something of a double edged sword; with every new opportunity or advancement AI offers up to businesses, it’s offering the same leg up to cyber criminals.

“AI is both a hindrance and a help to the cyber landscape,” added Warr. “As AI becomes more widely accessible, cybercriminals and cyber activists can launch larger-scale attacks at a faster pace. This increased capability in scale and speed brought on by AI could threaten the cyber domain. However, controlled and managed use of AI can also help detect cyber vulnerabilities.”

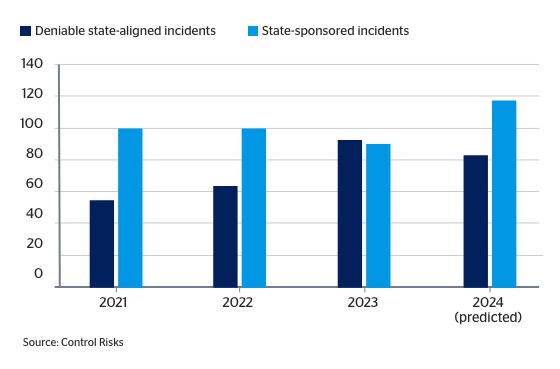

One way AI is helping companies here is in identifying and responding to ransomware attacks. According to QBE, ransomware attacks in 2023 were up 74% on 2022 – and they’re not looking like slowing down. According to Control Risk data, ransomware attacks across the entirely of 2024 were on the rise, with 5,200 publicly named attacks predicted in 2025 – up from 4,800 last year. What’s more, globally, the average ransom payment in 2023 increased five-fold to USD$2m compared to USD$400,000 the previous year.

And yet, despite these growing risks, 43% of companies still don’t have cyber insurance – with 36% adding that they don’t even have an incident response plan to address a cyber event. When asked why this is, the majority of businesses said it’s not a priority, it’s too expensive and that their business simply wouldn’t be a target – a dangerous outlook in today’s risky landscape.

It’s time to start thinking about cybercrime preventatively rather than curatively – and that begins with implementing the best cyber insurance. QBE has developed a range of tools and risk services for their clients to help them reduce their cyber risk and assist with recovery during a cyber event. For more information, please visit here.