Government and the Financial Conduct Authority (FCA) have pledged to act on secret insurance commissions being paid to property managing agents and freeholders as part of a bid to tackle soaring buildings insurance costs, with the insurance industry and the regulator having faced recent Parliamentary scrutiny.

Recent promised regulatory action on broker commissions and fair value and a promise from Secretary of State for Levelling Up, Housing and Communities Michael Gove to stamp out third-party commission payments, though, will only go so far in addressing the buildings insurance costs problem, according to both industry insiders and leaseholder advocates.

The FCA has proposed a range of measures, expected to be finalised this quarter, to help bring down buildings insurance costs, which have spiked to see some buildings costing hundreds of thousands of pounds to insure. Updates proposed by the financial services watchdog include:

In an example that has drawn ire from leaseholders and MPs, one policy was subject to a 62% commission payment. Many brokers and insurers had agreed commissions in excess of 30%, and more than half of total commissions were paid to managing agents or freeholders in 39% of cases.

Under changes, the regulator has proposed enforcing greater transparency and customer consideration for leaseholders where it comes to their insurance arrangements under ICOBs, PROD, and SYSC rules. This should see brokers forced to disclose commission levels and fee arrangements and, in theory, eradicate the risk of “secret” or inflated commissions.

“Our reforms will give leaseholders greater rights and transparency in the multi-occupancy buildings insurance market,” an FCA spokesperson said. “These rule changes will require those underwriting and selling insurance to act in leaseholders’ best interests and ban firms from recommending a policy based on the levels of commission or remuneration.

“We will act where firms are not following our rules.”

It has taken costly legal battles for leaseholders to attempt to gain access to insurance information, and to find out costs that have been paid to insurance brokers, freeholders and property managing agents, as seen in the landmark Canary Riverside case, which is subject to appeal.

Regulatory changes should go some way to providing greater transparency, and all organisations and individuals contacted by Insurance Business for this article agreed that the commissions scandal must be tackled. However, according to industry stakeholders and campaigners and advocates, this will not be a quick fix for the buildings insurance costs problem.

This has been a source of frustration for leaseholder advocates, who have alleged that there has been a lack of scrutiny of insurers with much focus drawn to brokers who have, to some extent, been “playing piggy in the middle”, in the words of one campaigner.

As of 2021 to 2022, there were an estimated 4.98 million leasehold dwellings in England alone, according to government figures, equating to 20% of housing stock in the country. Of these, 57% were owner occupied, 37% were privately owned and let, and 5% were in the social rented sector.

With the FCA’s analysis having found that some insurance commissions being taken were as low as 10%, not all leaseholders experiencing rising insurance costs will have unknowingly been affected by “rip-off” remuneration practices in the market.

An industry insider has shared concerns around the broker focus of the regulator’s recent investigations and proposals.

“The FCA talked about brokers but it’s the insurer that agrees the commission, and even if they’ve had their arm twisted, they’re still agreeing the commission,” said Branko Bjelobaba, Branko principal.

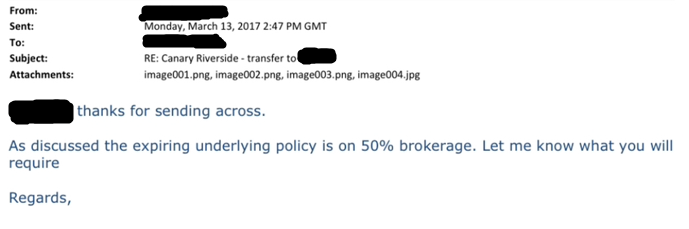

In an example of insurers acquiescing to or offering commissions of over 30%, cited by multiple interviewees including Bjelobaba, in a 2017 email sent by a representative of Tokio Marine Kiln Insurance (TMKI) in response to a broker inquiring about commission levels, regarding insurance arrangements for Canary Riverside, an underwriter confirmed that underlying brokerage was 50% (see image below).

“Let me know what you will require,” the underwriter, who no longer works for the business, which was put into run-off in 2019 and is therefore no longer active in the market, went on to say. The freeholders’ broker was reappointed to again look after the policy the day after this email was sent, it is understood, meaning the broker involved in the email chain did not receive any remuneration on this policy.

In its September 2022 report, the regulator cautioned of a lack of data being collated by insurers and brokers, with smaller portfolios better accounted for and its analysis therefore likely “skewed” towards smaller buildings. The regulator said it was still able to draw “meaningful conclusions” from this data and further qualitative analysis.

The average premium in a sample investigated in its April 2023 Broker Remuneration Review was around £11,625 – well below the hundreds of thousands of pounds that leaseholders have reported are being paid by some larger blocks, where advocates argue other factors could be at play in driving up costs that require more detailed investigation.

In an emailed comment, British Insurance Brokers’ Association (BIBA) executive director and incoming CEO Graeme Trudgill told Insurance Business that in the broker association’s view, the FCA’s data appears “robust”; however, he pointed out that broker commissions as a percentage have been falling while the amount being taken by insurers has continued to increase.

In its April 2023 report, the FCA found a gradual reduction in remuneration (from 29% in 2019 to 25.9% in 2022) and commission (from 23.9% in 2019 to 22.3% in 2022) as a percentage of GWP, which increased by 82% from 2019 to 2021.

“The focus ever since has been on commissions, but there is no escaping the fact that premiums have been increasing at a more rapid rate than broker earnings,” Trudgill said.

The FCA itself flagged numerous market issues, among them several not pertaining to the role of brokers and property managing agents, in its initial September 2022 report. Among these were potential competition concerns, a capacity constriction and premium inflation that was unlikely to return to pre-remediation levels for buildings affected by fire safety risk discovered in the aftermath of 2017’s Grenfell Tower fire.

“We recognise the financial and emotional strain being placed on leaseholders and we’re working hard as an industry to do what we can to try and help reduce insurance costs for them,” an ABI spokesperson said. “The FCA’s report set out a number of reasons as to why insurance premiums have increased for multi-occupancy buildings affected by building safety issues and whilst we agree the regulator should consider the level of broker and managing agent commissions, this is just one aspect of a wider issue.”

The ABI spokesperson said there is “no single insurance intervention that will help all leaseholders equally”, and pointed to further steps that could be taken, including an end to insurance premium tax (IPT) of 12%, something that BIBA has also drawn attention to, being charged on buildings insurance policies and continued remediation and adherence to building safety standards.

“We urge the government to escalate this work as quickly as possible,” they said.

It is hoped that a reinsurance pooling arrangement, being worked on by the ABI and BIBA, will go some way in putting downwards pressure on insurance pricing.

However, some stakeholders – including The Property Institute (TPI), which has seen its industry under fire over property managing agents’ commission takes – have been left unimpressed by the regulator and government leaving these developments in the hands of trade associations.

“The FCA investigated the reasons for the increases in premiums but concluded they could not comment on whether the increases charged by insurers are reasonable,” TPI CEO Andrew Bulmer said in an emailed comment. “That will be a disappointment to leaseholders hit by large increases and we believe the FCA should redouble their efforts to understand if the increases are justified.”

There is an additional challenge for the regulator and for government as they look to clamp down on sky high insurance costs and ensure transparency across the chain: the FCA has oversight of some, but not all, entities connected to property managing agents across some functions. As of a 2005 report obtained by the Leasehold Knowledge Partnership via FOI, the FCA’s predecessor the FSA said, as of 18 years ago, it had oversight of approximately 650 property managing agents.

Speaking at a recent committee hearing, FCA executive director, consumers and competition Sheldon Mills – a leaseholder himself – said that regulation of property managing agents or freeholders could drive a “more consistent, coherent approach”. TPI, too, has added to calls for regulation to help target what Bulmer termed a “minority of rogue agents”. At present, it is unclear which organisation might take on responsibility as a regulator.

Gove has pledged that property managing agents will move to a fee- rather than commission-based model, a change TPI’s CEO said the organisation supports.

Another key battleground for leaseholders: under current plans, they will continue to be unable to avail of the Financial Ombudsman Service (FOS) where it comes to contesting claims decisions, despite being the ultimate payers of the premium. This is a matter that FCA representatives have contended must be addressed by government, as it pertains to contract law and the payment of service charges to leaseholders is not currently a regulated activity.

“That the FCA haven’t even done just a basic [courtesy] of making us as a customer doesn’t fill me with hope about this fair value,” said Harry Scoffin, Commonhold Now co-founder.

One option, considered but not adopted in proposals by the regulator, could be to make leaseholders end customers of a policy. However, FCA director of general insurance and conduct specialists Matthew Brewis told MPs that it would be more expensive for people to insure individually, due to levels of bureaucracy and administration involved, with one “master policy” still needing to be in place.

“That totally ignores the fact it already happens,” Leasehold Knowledge Partnership chair Martin Boyd said. “Those leaseholders who do own freehold of their site and are deemed party to the contract already have these rights.”

With the government taking action on ground rent and lease extensions, and more changes planned, commissions have been just one cog in a wheel of premium problems, which in turn have presented just one faulty part of the leasehold costs machine.

It’s a machine that will take work from multiple stakeholders to fix, and the commission crackdown can only serve as one part of remediation efforts. In the interim, campaigners will likely continue to call for enhanced scrutiny of the role of insurers and draw attention to any further climbing costs.