5-Star Construction 2022

Jump to winners | Jump to methodology

Building Britain back better

Boris Johnson has resigned, but the UK is still following his often-repeated slogan to “build back better.” According to the UK Office of National Statistics, as of May, the construction industry has experienced seven consecutive months of growth – in the face of ongoing challenges ranging from labour shortages, supply chain difficulties and inflation. What’s more, compared with pre-pandemic Britain in February 2020, construction output for May was 4.1% higher.

“I do see a lot of resilience, adaptability, and innovation within the construction sector,” says Daniel Storr, underwriting manager – construction at Q Underwriting.

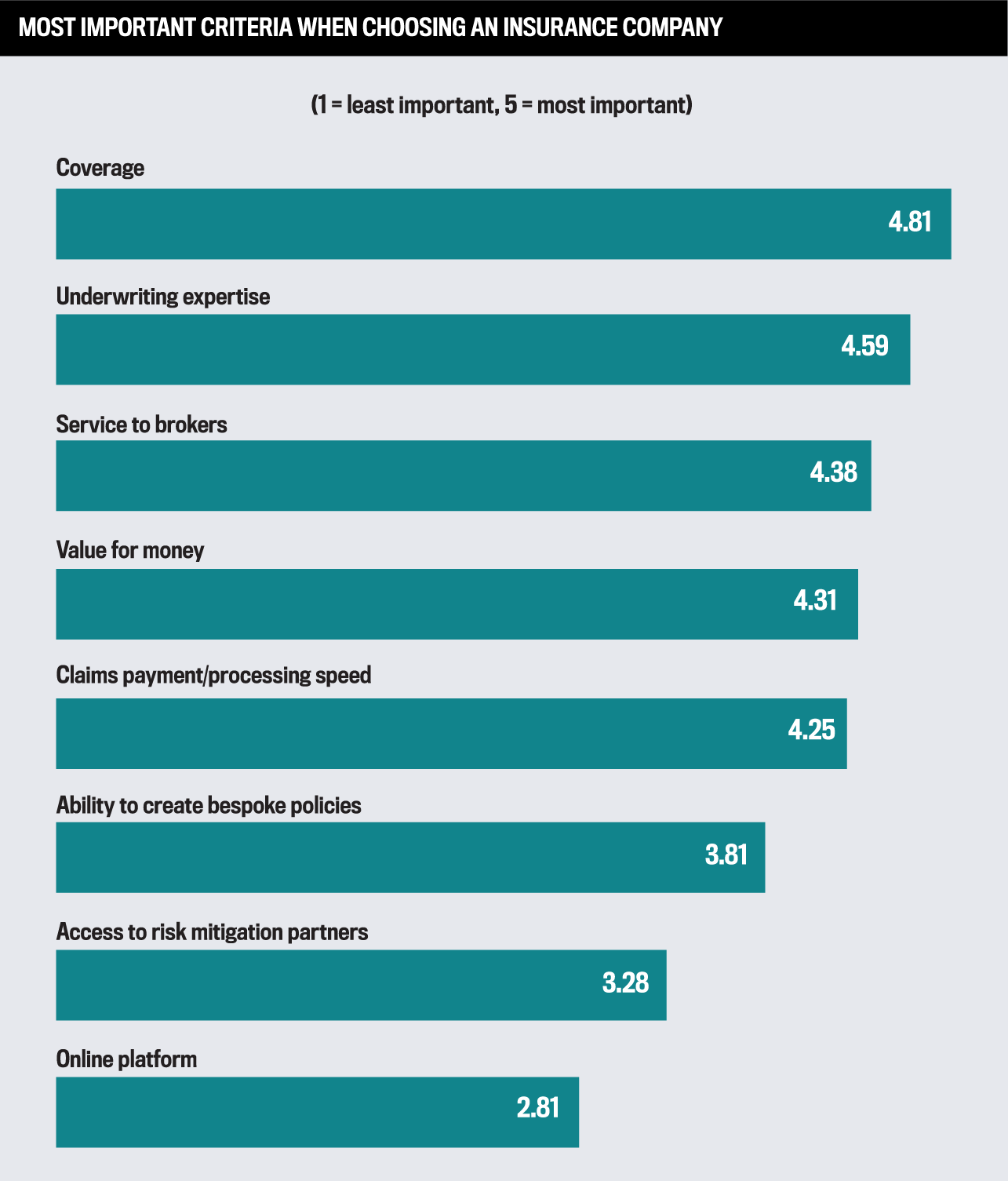

Along with 24 other insurers and MGAs, Q Underwriting has won a 2022 IBUK 5-Star Construction award for helping bolster the building industry. After asking hundreds of brokers to rate the construction insurers they’d worked with over the past 12 months, Insurance Business UK ranked the companies on work quality, specialist expertise, and client service across 15 categories.

“The one-stop shop is what we aim to do. I think the continuity of the underwriting solution and access to specialist London markets is what we pride ourselves on”

Simon Taylor, Jensten Underwriting

Perfect storm of political and regulatory forces

HSB notes five trends in the general UK construction industry. As part of the “build back better” initiative, the government has engaged in a five-year £640 billion plan to upgrade the country’s infrastructure. They’re also targeting the UK housing shortage. The industry is leveraging technologies to help cut costs. Moreover, they are dealing with delays caused by having to scale back personnel on site due to COVID concerns. Lastly, there’s Brexit, which has not only made it more difficult to access and leverage talent from overseas but also increased costs for importing and exporting construction materials.

“It would be most people’s view that Brexit and COVID have caused issues around the availability of labour, supply chain issues, and the ability to manufacture,” says Storr.

Regarding the housing shortage, he acknowledges the gap between what is required and what’s planned – emphasising that more focus on this issue could further help the UK “build back better,” considering construction’s overall impact on the general economy.

In addition, he notes the problem with costs for companies that manufacture bricks, tiles, and other construction materials. “People just doing DIY projects who go to builders and merchants and get a quote of one price on Friday, and it’s valid for 24 hours,” says Storr. “They come back on Monday, and the price had gone up. It’s volatile, it’s difficult. But I do believe that contractors have resilience, adaptability, and innovation on their side.”

Meanwhile, Simon Taylor, wholesale managing director of Jensten Underwriting – parent company of Policyfast, another 2022 IBUK 5-Star Construction winner – agrees with Storr’s appraisal and mentions two other points of contention. “The biggest issue that we’re facing at the moment is claims inflation,” he adds. “General inflation is running north of 15% or 20%, particularly in the construction sector. That presents problems for us in effectively managing claims, reserving claims, and getting the right price on the risk in order to make underwriting profit. But it’s very hard to get your technical pricing correct in such a volatile inflationary position.

“[In addition,] it’s not just the problem with Brexit and COVID, but also with China continuing to lock down with a zero-tolerance policy. That shortage of supply coming out of China for all things, but specifically construction materials, that’s feeding into the supply chain pressures as well.”

“ It would be most people’s view that Brexit and COVID have caused issues around the availability of labour, supply chain issues, and the ability to manufacture”

Daniel Storr, Q Underwriting

Inflation, inflation, inflation

Taylor and Jensten Underwriting are bullish regarding the recent construction boom. “It’s not just in the repair and maintenance, we’re actually seeing it in new builds, which is always good to see,” says Taylor.

For Taylor, the construction segment has been one of the better sectors to navigate the pandemic. Of course, that’s also reflected in a reasonable steady construction insurance market, where rates have been gradually increasing – especially liability rates over the last two years – but are more settled now.

Meanwhile, Storr echoes Taylor’s bullishness regarding the industry, emphasising the perseverance of the sector. As for trends in construction insurance, he spots a potential increase in business regarding composite materials associated with heavier builds and hazardous activities.

As an MGA, he says, Q Underwriting sees a healthy appetite for construction business. However, he’s heard of others struggling at times to find the capacity to meet niche needs.

“We’re looking to develop long-term relationships with our capacity providers to have that continuity,” he reveals. “We’re always looking for quality of capacity. We do have expert underwriters, but as we grow, it’s important that we increase that underwriter pool and continue to develop that expertise.”

Along with Taylor, Storr is concerned about the impact of inflation on materials and labour costs and their potential impact on contract values.

The annual material price inflation increased to over 24% in March for a basket of materials, according to the Department for Business, Energy, and Industrial Strategy.

“[Regarding inflation in materials and labour costs,] what does that do to contract values?” says Storr.

“The contract durations? There’s uncertainty, there’s inflation, there’s greater cost. That’s the longer contracts. People’s risk acceptance might well be set, and is it being eroded constantly by the inflationary effects of what is taking place in the construction marketplace? And can they therefore, continue to meet the requirements of their clients who need higher contract limits and need longer maximum contract periods? So, I think it’s just about how we, as insurers, [stay] resilient, adaptable [and] innovative, because that’s what contractors seem to be as well. So, we just wanted to match the qualities. And that’s, I think, some of the challenges over the next couple of years.”

Categorical excellence

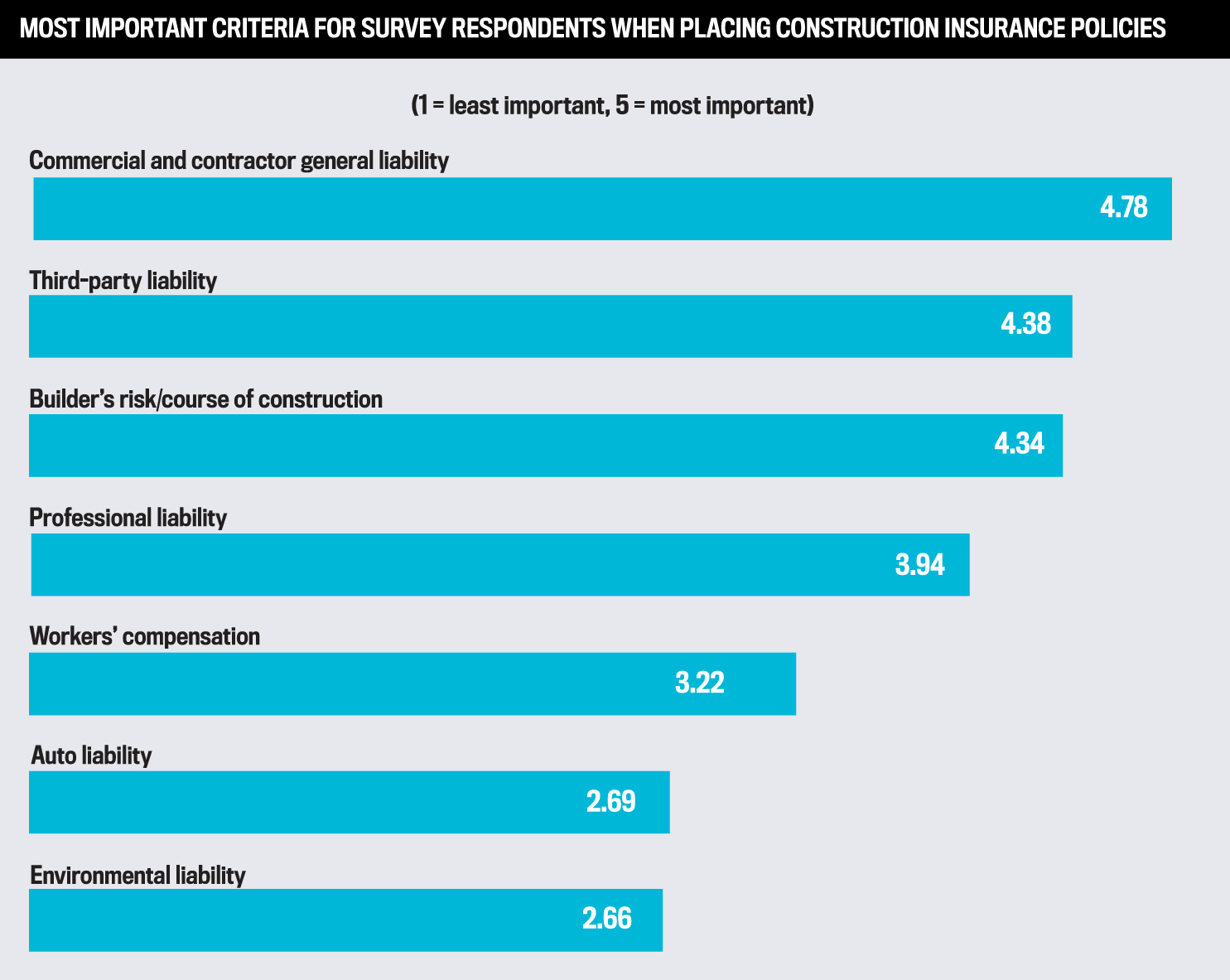

To honour specialised coverages, we assigned 2022 IBUK 5-Star Construction awards across 15 categories, from builder’s risk/course of construction, to auto liability and demolition.

Jensten Underwriting won in the professional liability category. What distinguishes them in that field?

“We have quality people who really understand what they’re doing in that space,” says Taylor. “We, as an MGA, make sure that we own the products and that we have the intellectual property on it so that we can respond quickly. We have our own in-house actuarial people. And I think the really key point for me is when there isn’t necessarily an underwriting solution for us in house, we’re able to then guide that broker into our Lloyd’s broker. And we do that seamlessly, or we’ll cover one bit in the team and then use the Lloyd’s markets on the other aspects to it.”

While Jensten Underwriting only won in one category, Taylor emphasises that the MGA is focused on helping out with all aspects of the construction business. “The one-stop shop is what we aim to do,” says Taylor. “I think the continuity of the underwriting solution and access to specialist London markets is what we pride ourselves on.”

Jensten Underwriting is proud of its people, underwriting skills, and partnerships with capacity providers, the Lloyd’s market and producing brokers.

Meanwhile, Q Underwriting won in builder’s risk/course of construction, commercial and contractor general liability, third party liability, civil contractors, general contractors, subcontractors, specialty trade contractors, professional construction service firms, developers and owners, heavy construction, and demolition.

What distinguishes them in these fields? “We’re looking at ways we can make it easier for brokers to transact business online with us,” says Storr. “But recognising the fact that there is inflationary pressure in the construction sector, we are looking to increase our capacity, our expertise, et cetera, in relation to larger contracts.

“Right now, we’re seeing more $10-million plus contacts. We are expecting more as those inflationary pressures do bite… So, expertise and making sure that we are managing that with our capacity partners is important. We have an emphasis on making sure we’re easy to deal with so that our e-trade platform is fit for purpose and that we get as much traffic through as we possibly can.”

Storr also notes that Q Underwriting has primary and excess layer facilities and the ability to give large liability limits.

“With expertise and experience comes empowerment,” he explains. “And we’ve got a culture which makes sure that empowerment is genuinely felt by the underwriters. That improves what we do across all these categories and improves the broker experience.”

Regarding the civil contractors’ award, Storr says there should be multiple rates to account for the diversity of the sector. As a result, Q Underwriting is in the process of segmenting its book to differentiate its rate and appetite. In terms of the heavy construction award in particular, he says, the company has a strong, healthy appetite for the heavy construction business. “So, because we’ve got that familiarity and confidence around heavy construction, we can cater not just for those heavy construction risks but also for those vanilla risks.”

Storr added that Q Underwriting places an importance on growing accounts, as well as its products, risk appetite, and quality underwriters. Their year-on-year growth of their flagship contractors combined product is in excess of 25% based on strong new business performance, good retention level and growth in contracting activity.

5-Star Construction 2022

Auto liability

- Lloyd’s

Builder’s risk/course of construction

- Chapman & Stacey Underwriting Agency

- Ensurance

- HDI Global SE

- Mi Commercial Risks

- Origin UW Limited

- Pen Underwriting

- Q Underwriting

- RSA

Civil contractors

- Brit

- CNA

- HDI

- Lloyd’s

- Manchester Underwriting Management

- Origin Underwriting

- Probitas 1492

- PRS

- Q Underwriting

- RSA Insurance

- Syndicate 2525

Commercial and contractor general liability

- Brit

- Chapman & Stacey Underwriting Agency

- CNA

- Manchester Underwriting Management

- Mi Commercial Risks

- Origin UW Limited

- Pen Underwriting

- Probitas 1492

- PRS

- Q Underwriting

- RSA Insurance

- Syndicate 2525

Demolition

- Liberty Specialty Markets

- Lloyd’s

- Manchester Underwriting Management

- Mi Commercial Risks

- Probitas 1492

- Q Underwriting

Developers and owners

- Brit

- Chapman & Stacey Underwriting Agency

- CNA

- HDI

- Manchester Underwriting Management

- Mi Commercial Risks

- Origin Underwriting

- ProAktive

- Probitas 1492

- PRS

- Q Underwriting

- RSA

- Syndicate 2525

Environmental liability

- CFC Underwriting

- Liberty Specialty Markets

- Lloyd’s

- Pen Underwriting

General contractors

- Brit

- Chapman & Stacey Underwriting Agency

- CNA

- Lloyd’s

- Manchester Underwriting Management

- Origin Underwriting

- Probitas 1492

- PRS

- Q Underwriting

- RSA

- Syndicate 2525

Heavy construction

- Amwins

- Brit

- CNA

- HDI

- Manchester Underwriting Management

- Mi Commercial Risks

- Probitas 1492

- PRS

- Q Underwriting

- RSA

- Syndicate 2525

- Thames Underwriting

Professional construction service firms

- Chapman & Stacey Underwriting Agency

- HCC

- Lloyd’s

- Mi Commercial Risks

- Origin Underwriting

- Q Underwriting

Professional liability

- Chapman & Stacey Underwriting Agency

- CNA

- HCC

- Lloyd’s

- Policyfast

- PremCo

- Starr Insurance

Specialty trade contractors

- Chapman & Stacey Underwriting Agency

- CNA

- Lloyd’s

- Manchester Underwriting Management

- Mi Commercial Risks

- Origin Underwriting

- Probitas 1492

- PRS

- Q Underwriting

- Syndicate 2525

Subcontractors

- Chapman & Stacey Underwriting Agency

- Liberty Specialty Markets

- Lloyd’s

- Q Underwriting

- RSA

Third-party liability

- Mi Commercial Risks

- Origin Underwriting

- Q Underwriting

- RSA Insurance

Workers’ compensation

- CNA

- Origin Underwriting

Methodology

To select the best construction insurance providers for 2022, Insurance Business UK sourced feedback from insurance brokers. IBUK’s research team began by conducting a survey with a wide range of brokerages to determine what brokers value in a construction insurer. The team also spoke to hundreds of brokers across the country, asking them to rate the construction insurers they had worked with over the past 12 months.

The in-depth information gathered enabled the research team to assign weighted values to each criterion being rated by brokers. At the end of the research period, the insurance providers that received the highest rankings in terms of work quality, specialist expertise, and client service were named 5-Star Award winners in construction insurance.

Keep up with the latest news and events

Join our mailing list, it’s free!