AI-Powered Underwriting & Pricing Intelligence

The intelligence edge: how AI is reshaping underwriting in 2026

Underwriting has always been an information problem – the challenge of knowing enough about a risk, quickly enough, to make a good decision. AI is changing both sides of that equation. AI has quickly moved from a promising innovation to a strategic priority across the insurance sector, changing everything from speed and efficiency to pricing and client expectations. And while the new tech has become a fixture of industry conversations at large, it’s in the realm of underwriting where AI has arguably undergone the most significant transformation.

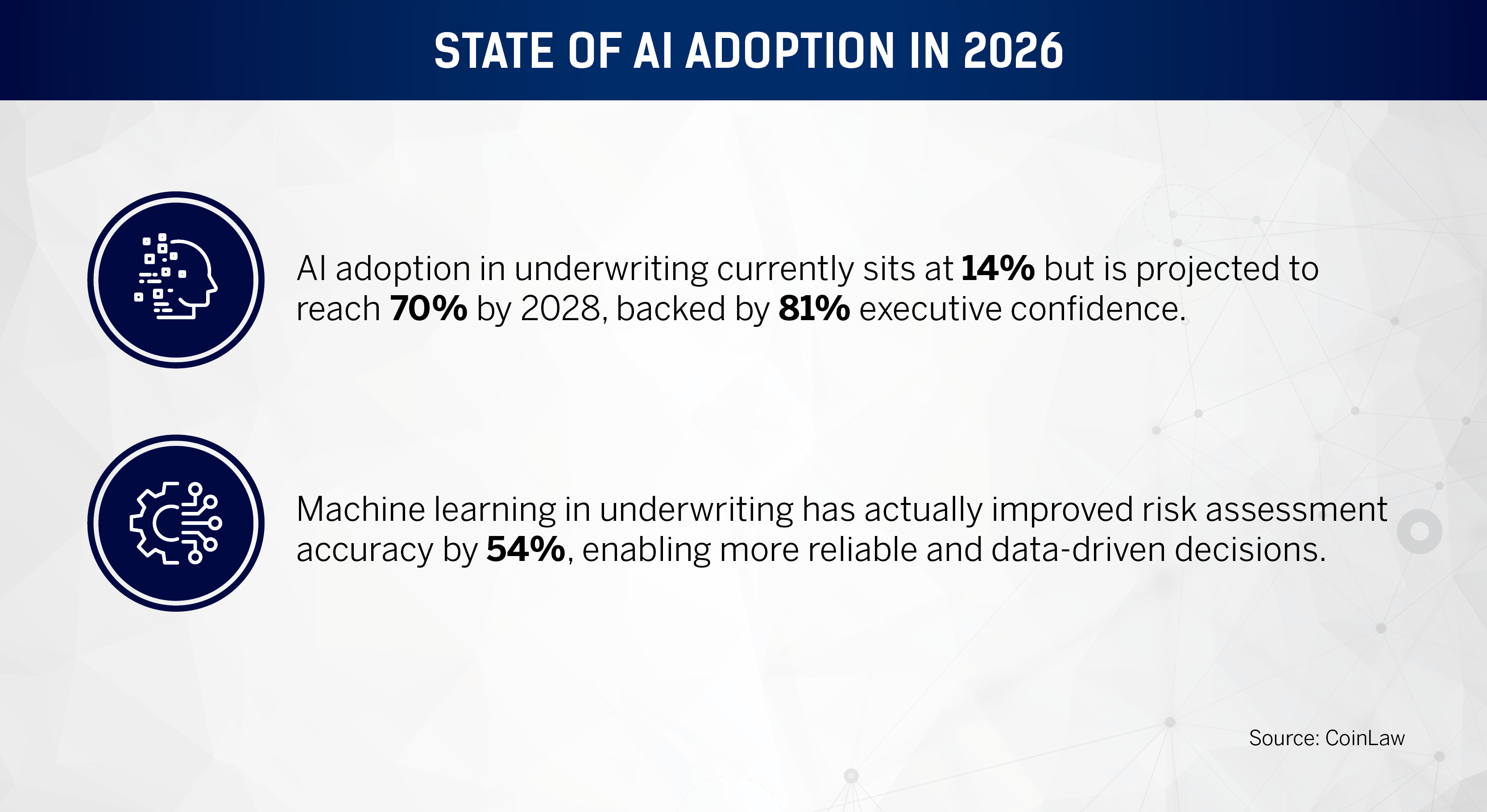

AI adoption in underwriting currently sits at 14 percent but is projected to reach 70 percent by 2028, backed by 81 percent executive confidence. Furthermore, machine learning in underwriting has actually improved risk assessment accuracy by 54 percent, enabling more reliable and data-driven decisions, according to CoinLaw.

For carriers and MGAs, this maturity curve has played out most visibly in submission handling, where the volume of risks being presented has outpaced the capacity of underwriting teams to evaluate them manually, creating pressure to find smarter ways to triage, prioritize, and assess.

But for underwriting teams, the appeal here was more obvious. Tasks that previously required hours of manual review could now be completed in minutes, helping insurers reduce administrative workloads and improve submission turnaround times. However, while the technology proved effective at extracting information, it did little to address a more fundamental challenge – how that information should be used.

From IDP to decision intelligence

As adoption increased, insurers quickly realized that data extraction alone would not deliver a meaningful competitive advantage – and that access to more information did not automatically result in better underwriting decisions. Instead, the industry’s focus began to shift from data collection to data utilization.

Throughout 2025, carriers increasingly explored how AI could support appetite checks, submission triage, and risk evaluation. Rather than simply moving information from one system to another, insurers began applying AI to help underwriters interpret risk, identify opportunities, and prioritize submissions more effectively.

In practice, this has meant moving beyond tools that simply read a submission to platforms that can compare it against a carrier’s appetite, flag inconsistencies in the data, and surface relevant loss history – all before the submission reaches an underwriter’s desk.

While historically, most systems were designed to improve workflow efficiency, in 2026, the next generation of AI platforms is increasingly being designed to support decision-making itself. This is reassuring news, especially considering that 82 percent of insurance leaders cited improving financial and operational performance as the primary driver for exploring AI – with nearly three-quarters of underwriting professionals specifically identifying it as a departmental priority, according to Roots.

Peeyush Rai Weav.ai

AI-powered risk assessment and appetite matching

Before AI, determining whether a risk aligned with a carrier’s appetite relied heavily on underwriter expertise and manual review. While effective, this approach can be difficult to scale as submission volumes increase and underwriting resources become more constrained. With the power of AI, tech-powered underwriting systems can process applications 70 percent faster while maintaining or improving accuracy – making the case that the bottleneck isn’t necessarily quality, it’s capacity.

In 2026, AI is increasingly being used to provide an initial assessment before a submission reaches an underwriter. By analyzing application data, historical performance, underwriting guidelines, and other risk indicators, these systems can help identify which opportunities warrant further attention and which are unlikely to fit a carrier’s appetite.

All in all, the main objective is not to replace underwriting judgment, but to direct it more effectively. The result is greater consistency, faster decision-making, and a more efficient allocation of underwriting resources – a finding supported by a Deloitte study that shows AI-driven underwriting processes can decrease costs by up to 50 percent while reducing processing time from weeks to minutes.

Straight-through processing and underwriting automation

As confidence in these AI-driven risk assessments grows, insurers are beginning to explore the higher levels of underwriting automation. Straight-through processing has long been viewed as a goal for the industry, but advances in AI are now making it a viable reality across selected classes of business in 2026.

According to Roots.ai’s State of AI Adoption in Insurance, 53 percent of underwriting professionals identify increasing speed to quote as a primary use case for AI. And, by combining risk scoring, appetite matching, and automated decision rules, insurers can now process certain submissions without requiring manual intervention.

“With AI, we have been able to enable a larger percentage of straight-through processing,” adds Peeyush Rai, founder and CEO of Weav.ai. “We have AI scorecards that assess the risk even before the underwriter sees it. In that assessment, the carrier is able to set thresholds as to what they consider a clean, great case or a clean denial – there’s also the ambiguous case in-between. The clean denials and the clean risks they go straight through – and they’re either denied or accepted.”

The benefits of AI here are significant. Automated underwriting workflows can reduce turnaround times, improve consistency, and allow underwriters to focus their attention on more complex risks where human expertise adds the greatest value. However, adoption still remains measured – as it should be. Most insurers continue to favor human-in-the-loop models, particularly for larger commercial risks where underwriting judgment, broker relationships, and market context remain critical components of the decision-making process. As a result, the industry’s focus is increasingly shifting from whether underwriting can be automated to determining which decisions should be automated and which should remain firmly in human hands.

Building a complete view of risk

Aside from the human-in-the-loop component, one core concern for AI in the underwriting process revolves around data quality. After all, the quality of an underwriting decision depends wholly on the quality of the information behind it. And while this sounds obvious, it has become one of the defining challenges of AI-powered underwriting in 2026. While carriers have made significant progress in automating risk assessment and streamlining underwriting workflows, many are now confronting a more fundamental issue: whether they have enough visibility into the risks they are being asked to assess.

For decades, underwriting decisions have been built around information supplied during the submission process. Application forms, broker presentations, loss histories, and third-party reports have long formed the foundation of risk evaluation. Yet these sources often provide only a partial view of a business and its exposures – and this disconnect is driving a significant shift in underwriting strategy. Rather than relying solely on information provided at the point of application, insurers are increasingly seeking ways to enrich their understanding of risk through additional sources of intelligence.

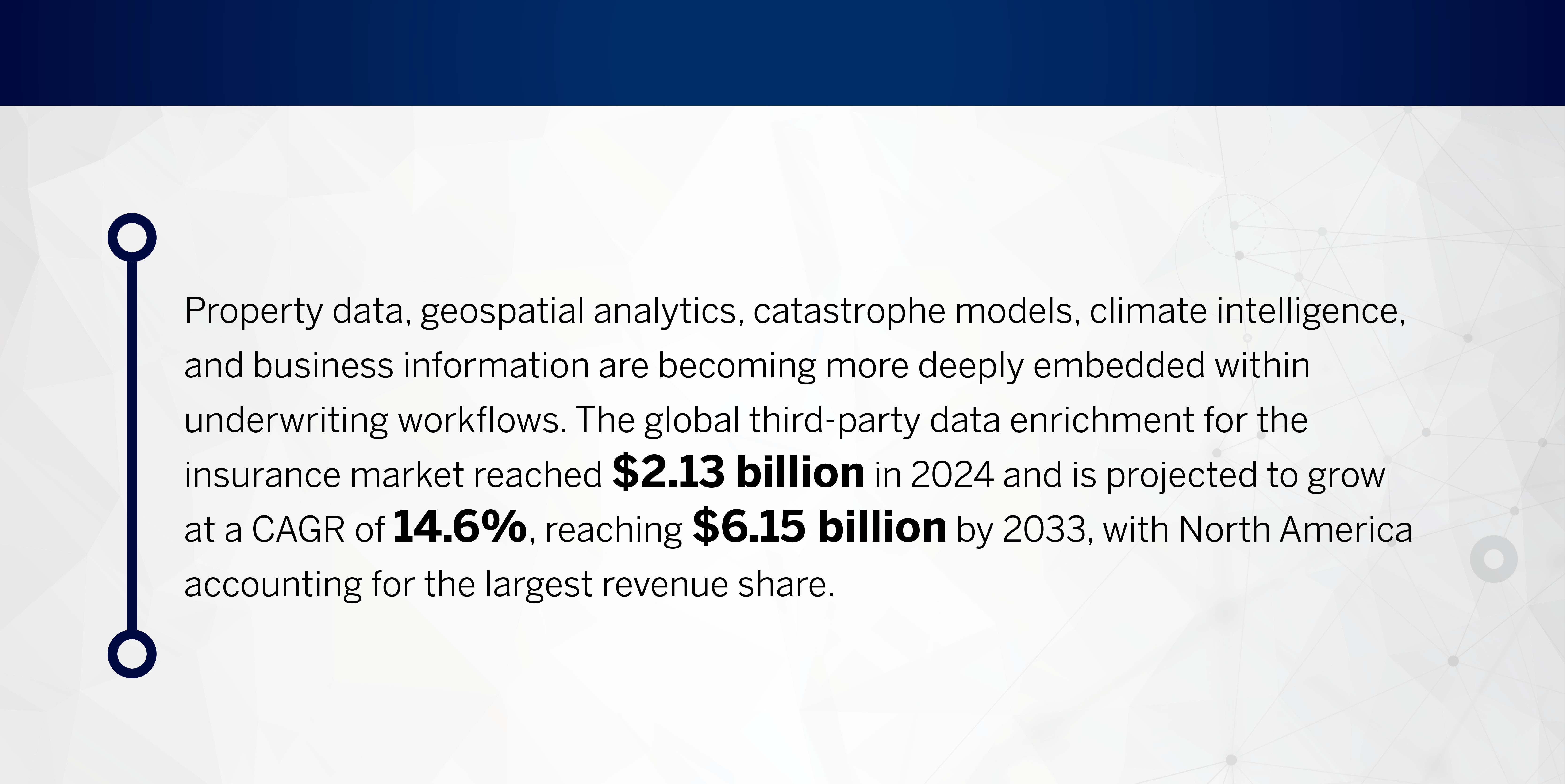

Property data, geospatial analytics, catastrophe models, climate intelligence, and business information are becoming more deeply embedded within underwriting workflows. The global third-party data enrichment for the insurance market reached $2.13 billion in 2024 and is projected to grow at a CAGR of 14.6 percent, reaching $6.15 billion by 2033, with North America accounting for the largest revenue share. These datasets provide additional context that can help carriers validate information, identify hidden exposures, and build a more detailed picture of the risks they are evaluating.

The trend reflects a broader change in thinking. Underwriting has traditionally been focused on gathering information. Increasingly, the challenge is understanding how different pieces of information connect together.

At Weav.ai, Rai explained that this collective view of data sets is something they practice day in, day out. As Rai told Insurance Business, access to external data is important, but data integrity is what drives meaningful outcomes.

“You need data from external sources, but how you handle the data is also important. We combine internal data sources, external data sources, and independent data sources into a completely cleansed and modeled knowledge graph,” he says. “The key is to really combine them into one view of the risk. When we build that accurate knowledge graph, that helps us get better pricing and rating. If you give pricing engines high-quality input, you’ll get a high-quality output.”

AI-powered pricing and rating

Building a more complete view of risk is also valuable in its own right. The real test, however, lies in whether those insights can be translated into better underwriting outcomes. And for insurers, that ultimately comes down to pricing.

The past several years have exposed the limitations of traditional pricing models – inflationary pressures, supply chain disruption, climate-related losses, and changing claims trends have created a more volatile operating environment, making it increasingly difficult for insurers to rely solely on historical loss experience when determining rates.

At the same time, underwriting teams are under growing pressure to balance profitability with growth. Price too aggressively and insurers risk losing market share, but price too conservatively and portfolios can quickly become unprofitable. And it’s at this intersection where AI is beginning to play a more significant role this year.

Unlike the first generation of pricing tools, which were largely focused on applying predefined rating factors, AI helps insurers to analyze larger volumes of information and identify patterns that may not be immediately visible through traditional methods. The objective is not necessarily to replace actuarial models or rating engines, but to enhance them with additional intelligence.

AI is also helping insurers identify trends across entire portfolios, enabling pricing teams to respond more quickly to emerging risks and shifts in loss experience. Rather than relying exclusively on periodic reviews, carriers are increasingly able to monitor performance continuously and make adjustments based on more current information.

That capability is becoming increasingly important as underwriting cycles shorten and market conditions evolve more rapidly. The ability to identify deteriorating performance, changing exposures or emerging concentrations of risk can provide insurers with an earlier opportunity to respond – both quickly and more effectively.

Peeyush RaiWeav.ai

Measuring success: from efficiency to profitability

For all the attention surrounding AI-powered underwriting, the technology’s long-term success will ultimately be determined by a far simpler question: does it improve business performance?

The first wave of results has been relatively easy to measure. Across the industry, insurers have reported meaningful reductions in submission processing times and quote turnaround, with some carriers cutting end-to-end underwriting cycle times from days to hours. For underwriting teams, this has translated into greater capacity to handle submission volumes without a proportionate increase in headcount – a tangible operational return on investment.

These efficiency gains have played an important role in driving adoption. Yet many insurers now view them as the starting point rather than the end goal, with the real promise of AI resting in its ability to improve underwriting outcomes.

Reducing the time it takes to process a submission is valuable, but only if insurers continue to select the right risks and maintain pricing discipline. Faster decisions do not automatically translate into better decisions, and many carriers are now looking beyond operational metrics to assess whether AI is influencing portfolio performance more broadly – with a WTW March 2026 survey finding that insurers who use more sophisticated analytics achieved combined ratios six percentage points lower than slower adopters between 2022 and 2024.

That shift is changing how success is measured. Historically, underwriting technology projects were often evaluated through operational indicators such as productivity, turnaround times, and cost savings. While those metrics remain important, insurers are increasingly focused on understanding the relationship between AI adoption and core underwriting measures, including loss ratios, combined ratios, premium growth, and portfolio profitability.

Unlike operational improvements, which can often be measured within weeks or months, underwriting performance develops over much longer periods. The quality of a risk selection decision may not become fully apparent until years after a policy has been written, making it difficult to establish a direct link between AI adoption and underwriting results in the short term. And this means many insurers are still in the early stages of evaluating the technology's broader impact.

What is becoming increasingly clear, however, is that AI is changing the way carriers monitor performance. Rather than relying solely on periodic reviews and historical reporting, insurers are beginning to use AI-driven analytics to identify emerging trends, monitor portfolio performance, and detect areas of concern earlier in the underwriting cycle.

AI and underwriting in 2030: what comes next?

The evolution of AI-powered underwriting has been marked by a series of distinct stages. The first focused on efficiency, with insurers deploying intelligent document processing tools to reduce manual workloads and accelerate submission handling. The second centered on decision intelligence, as carriers began applying AI to risk assessment, appetite matching, and underwriting automation.

The industry is now entering its third phase. Rather than focusing on individual use cases, insurers are increasingly looking at how AI can influence underwriting performance more broadly. The conversation is shifting away from point solutions and toward connected underwriting ecosystems, where risk assessment, pricing, portfolio management, and performance monitoring operate as part of a continuous feedback loop.

This reflects a growing recognition that underwriting is not a series of isolated decisions. Every risk written contributes to a wider portfolio, and every portfolio generates insights that can inform future underwriting decisions. The insurers gaining the most value from AI are therefore moving beyond workflow automation and looking at how the technology can support underwriting strategy as a whole.

At the same time, expectations are becoming more realistic. The early excitement surrounding AI often centered on the prospect of fully autonomous underwriting. But while automation levels continue to increase, particularly for lower-complexity risks, the market has largely settled on a more pragmatic view. Because in 2026, for most carriers, the objective is not to remove underwriters from the process but to equip them with better information, stronger insights, and more efficient workflows.

The competitive landscape is also beginning to change, with access to AI no longer being a differentiator in itself. Most insurers can deploy similar technologies, purchase similar datasets, and automate similar processes – but real advantage is increasingly determined by how effectively those capabilities are integrated into underwriting operations and how successfully organizations translate intelligence into action.

Looking ahead, the most successful insurers are unlikely to be those that simply automate more tasks. Instead, the real AI giants will be those that develop a deeper understanding of risk, make more informed underwriting decisions, and create stronger links between underwriting activity and portfolio performance.

The past three years have demonstrated that AI can make underwriting faster, and the next phase will determine whether it can make underwriting better.

“As underwriting becomes more automated and AI-driven, the real shift is that decisions are no longer confined to a single desk or system – they are made in a network of models, data sources, and portfolios that constantly learn from each other,” says Rai. “In that world, the real advantage goes to those who can plug their underwriting into the network, not just automate tasks inside one system.”

Keep up with the latest news and events

Join our mailing list, it’s free!