5-Star Cannabis Insurers: High-grade providers

Jump to winners | Jump to methodology | View PDF

Expectations are running high in the US cannabis market. Despite the COVID-19 pandemic’s deleterious effect on many sectors of the economy, the legal cannabis industry boomed in 2020. It’s currently valued at $15 billion and is anticipated to grow to up to $37 billion by 2024, according to Marijuana Business Daily. And all that new business will need insurance coverage.

“We are quite bullish on the growth in this particular sector,” says John Donahue, president of M.J. Hall & Company, a surplus lines brokerage based in California. “This is the first emerging market to hit the insurance space in a considerable amount of time. Many are and have been on the sidelines.

"Of those insurers still hesitant to jump into the sector, many are concerned with legal complications and exposures due to differences in state and federal laws. But things are changing. Congress recently reintroduced the Marijuana Opportunity Reinvestment and Expungement (MORE) Act, a bill to federally decriminalize cannabis, which was passed by the House late last year but failed in the Senate. And in March, a bipartisan group of senators introduced the Clarifying Law Around Insurance of Marijuana (CLAIM) Act, which would “create a safe harbor for insurers engaging in the business of insurance in connection with a cannabis-related legitimate business and for other purposes.

"Clearly, progress on these fronts is needed to bolster the sector. “On the federal level, the government has not clarified the contradiction between state and federal law enough,” Donahue says.

That’s limiting capacity in the cannabis space, says Crileen Kixmoeller, vice president of underwriting at James River Insurance, one of IBA’s 5-Star Cannabis Insurers.

“I don’t see the standard markets writing this business as admitted business on a national scale until there is legalization at the federal level,” she says.

Challenges and opportunities

With the legal aspects of this space still in flux, what distinguishes a leading provider of cannabis insurance in today’s market? Kixmoeller cites James River Insurance’s ability to tailor coverage to each client’s unique needs.

“We ask a lot of questions, not because we want to pester our clients, but because we want to do the best possible job for them,” she says, adding that “as an insurer, I think the most important thing we have to offer is our service. Timely response to requests for quotes, quick turnaround on policy issuance, being kind to one another when transacting business [are all important] – we’re all under stress in this current world."

Donahue likewise emphasizes the importance of customer service and also highlights the need to understand all elements of the business – from cultivation to processing – as a key indicator of competence.

“When an organization has this degree of depth in the industry, it can place more difficult-to-write risks and develop larger limits to address the needs of a wider breadth of insureds,” he says.

Providing excellent service also means being in tune with your clients’ key challenges. In the cannabis space, that includes compressed capacity for property and excess liability, Kixmoeller says, as well as a possible tightening of regulations on quality control and testing.

In addition, she says, “many segments of the insurance industry are experiencing an ongoing hard market. It’s very possible that it could bleed over into cannabis.”

Donahue, on the other hand, sees limited risks and lots of opportunities. COVID-19 ended up being a boon for the cannabis space, as state after state designated cannabis dispensaries essential operations. And looking ahead to 2022, he sees existing legal challenges likely giving way to greater opportunities, as legalization efforts are expected to succeed.

When it comes to the biggest issues clients have in this space, Donahue says retail producers are concerned with rede-fining bodily injury. He’s also seen a tight-ening of protective safeguard endorsements to deal with theft losses from last summer.

“Cannabis is an expensive commodity that can generate large losses with a relatively small amount of product,” he says.

Kixmoeller urges brokers and clients in the space to perform due diligence. “Make sure you’ve read the quotes first and that they are complete and contain the information that was presented and best represents the business,” she says. “It’s much easier to make changes at that stage than to try to undo errors or incorrect information on a policy.”

And what about pricing for cannabis insurance? “We do see some increases in the property portion of the premium, which could be a result of the overall market, as well as the first-party losses that have plagued the industry over the last year,” Donahue says.

Kixmoeller notes that “pricing thus far for cannabis on the liability side has been trending down, but as I said earlier, this could change. Other lines of coverage are seeing significant rate increases due to under-reserving, social inflation in jury awards and claims payments, and depressed pricing for so many years.”

While insurers that do participate in the cannabis space “are quite good at assessing the risk,” Donahue says, he notes that capacity is limited. “We are seeing some serious capital moving into this space. Facili-ties are becoming larger and larger. It is not uncommon to see a statement of values well in excess of $100 million. Since reinsurers seem somewhat reluctant to enter the space, capacity is constrained.”

What brokers want

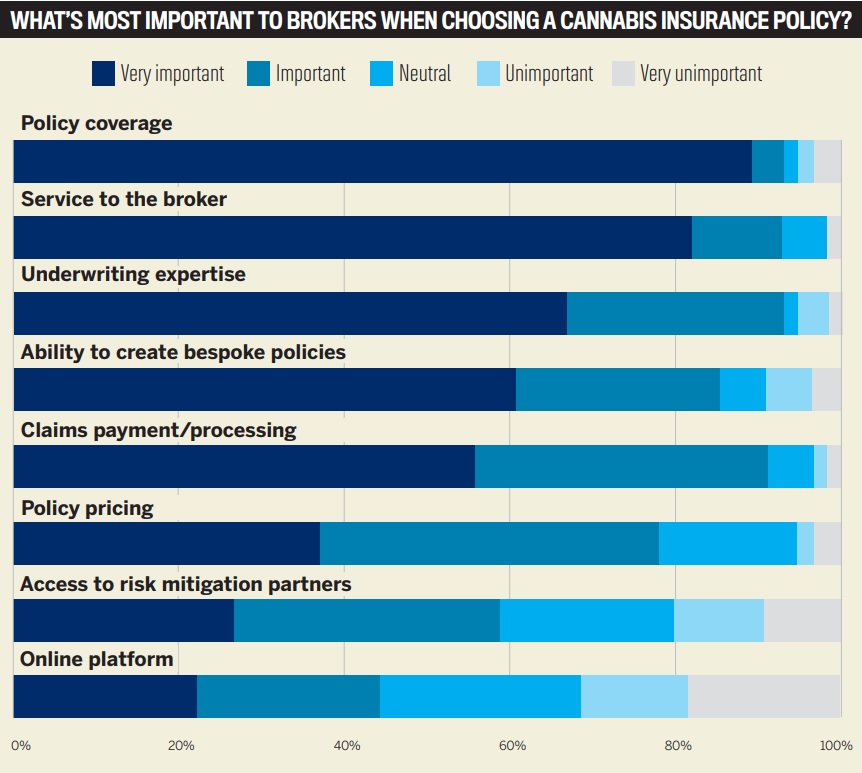

Of the hundreds of brokers IBA surveyed about their cannabis insurance providers, an overwhelming majority (89%) said policy coverage is of the utmost importance when selecting an insurer in this space. A couple of brokers noted that while pricing is also important, having enough coverage is critical for cannabis businesses. “In this field, it is better to be overinsured,” one broker said, while another said “the most important thing is that carriers have a comprehensive policy that provides the most coverage and the most coverage benefits for the client.”

Nearly as many brokers (81%) pointed to service as a critical factor when choosing a cannabis insurer. One broker emphasized that service includes both underwriting and claims handling and lamented the current state of the latter in the cannabis space, saying, “At this point, everyone is bad.” Another pointed out that speedy service is paramount: “[Brokers don’t want] to wait on turnaround of a submission. If they have good customer service, they will have a good turnaround time.”

Also key to brokers is underwriting expertise – 67% rated it as an important factor when choosing a cannabis insurer. For one broker, finding an underwriter who is easy to work with is crucial, while another said they only work with underwriters who have a proven track record. A third emphasized sector knowledge: “In cannabis, there are a lot of changing legal aspects – policies and forms aren’t always in line with legalization, so we need to work with underwriters who really know what they are doing and what is going on in the industry.”

The ability to customize policies was also an important factor for well over half of brokers (60%). As one broker put it, “Customization is important because there are many restrictions on cannabis companies.” Another noted that the “best carriers can tailor the coverage policy to clients’ specific needs.”

Meanwhile, 56% of brokers said claims payment/processing speed was key. One pointed out that most companies outsource their claims, but said the best insurers in this space are the ones with internal claims handling teams. Another noted that claims handling and management are especially critical in workers’ compensation insurance.

Relatively unimportant to brokers when choosing a cannabis policy were pricing (deemed important by only 37% of brokers), access to risk mitigation partners (26%) and an insurer’s online platform (22%).

5-Star Cannabis Insurers

- Admiral Insurance

- Cannasure Insurance Services

- Canopius Insurance

- Golden Bear Insurance

- James River Insurance Company

- Kinsale

- Quadscore

- Veracity Insurance

Methodology

‘Market-leading’ is a phrase many insurance companies like to use when describing their products. Now 10 companies can claim that title on the back of hard market research from the people who matter most: insurance brokers.

To select the best cannabis insurers for 2021, IBA surveyed hundreds of brokers to gain a keen understanding of what insurance professionals think of current market offerings. Brokers were first quizzed on what features they thought were most important in a cannabis insurance policy and then asked how the insurers they dealt with rated on those attributes.

Insurers were measured on the strength of their relationships with brokers, ability to handle claims, underwriting expertise and, most importantly, the strength of the individual products they provide.

Best in Cannabis Insurance

- General Liability

- Property Liability

- Professional Liability

- Package Liability

- Products Liability

- Workers’ Compensation

- MGAs

Learn more about our partner

National Cannabis Industry Association

Keep up with the latest news and events

Join our mailing list, it’s free!