Best Insurers for Claims in the USA | 5-Star Claims

Jump to winners | Jump to methodology

Excellence under pressure: how America’s top claims insurers are winning broker trust

Sixteen US insurance carriers have earned Insurance Business America’s 5-Star Claims designation for 2026, as rated by brokers across the country on claims management, communication, and operational efficiency. This report identifies which companies earned the designation and what they do differently.

Introduction – The pressure cooker:

US commercial claims in 2026

American brokers have a simple test for the carriers they recommend: be there when it matters. In commercial insurance claims – the moment of truth in every policy – that test is harder than ever to pass in 2026. Rising litigation severity, nuclear verdicts, and a litigation funding industry pouring billions into plaintiff-side cases have made the US claims environment one of the most challenging in the world. Against that backdrop, Insurance Business America’s 5-Star Claims 2026 report identifies the best insurers for claims in the US, as rated by brokers across the country.

The 2026 designation was awarded following a comprehensive two-phase broker-rated research process. Brokers were first invited to nominate the insurers they believed delivered the best claims management and claims handling, rating them across key performance indicators. Carriers that received sufficient broker nominations were then invited to submit detailed evidence of their claims capabilities. Final designations were awarded to those organizations that achieved outstanding broker ratings while also demonstrating excellence in claims management, operational efficiency, and broker engagement. Sixteen insurers earned the 5-Star Claims designation for 2026.

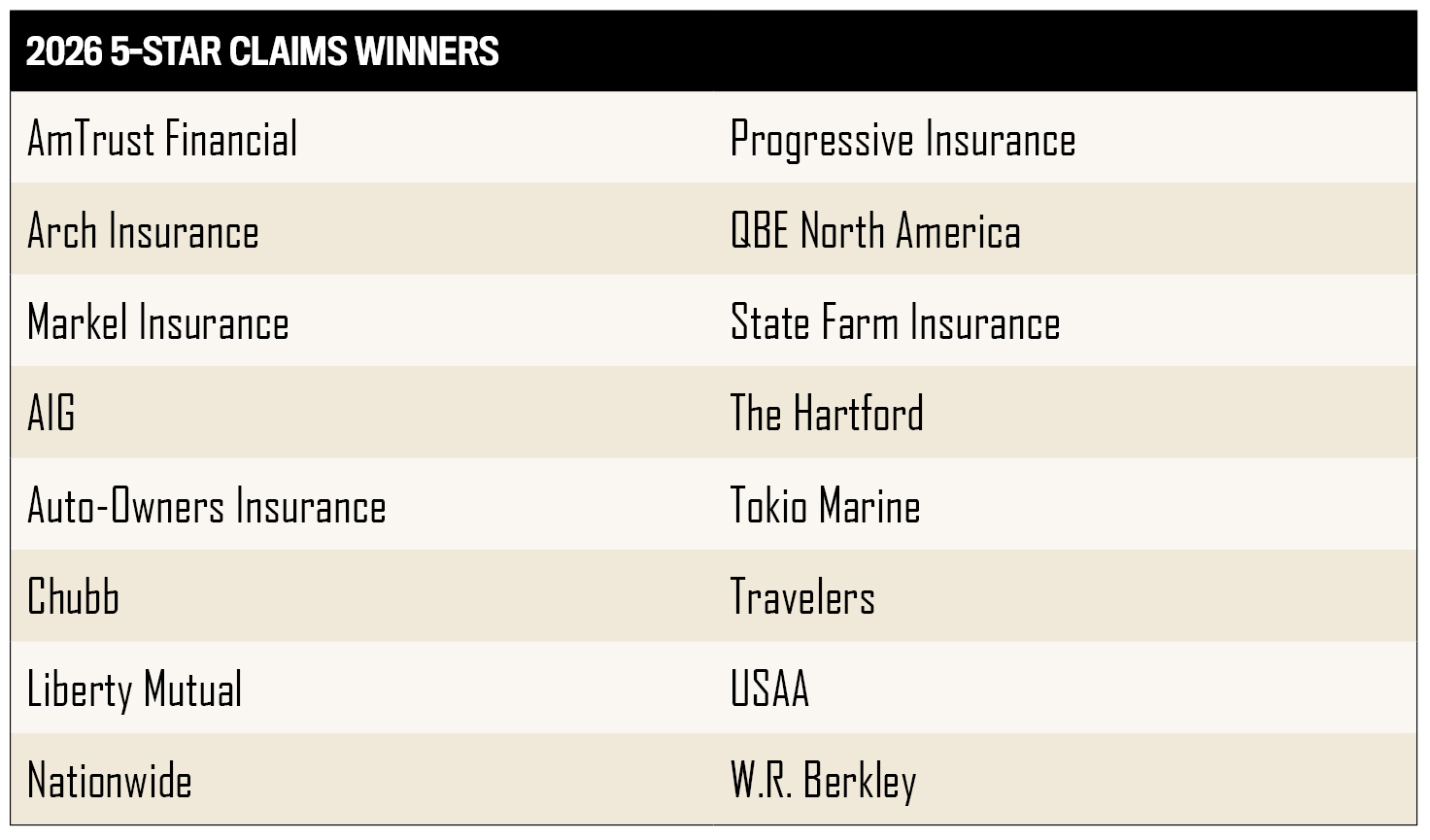

The 16 insurers that earned the 5-Star Claims designation for 2026 are the following:

The findings point to a clear pattern – the carriers brokers trust most for commercial insurance claims are those that:

-

communicate with consistency

-

deploy specialist expertise

-

use technology to free their people to exercise judgment, not to replace it

Industry context – What brokers demand

in 2026

The gap between what brokers expect from claims service and what insurers actually deliver has a single, consistent root cause: communication. According to Sean O’Neill, partner and head of the global insurance practice at Bain & Company in Boston, responsiveness and transparency are the two qualities brokers value most – and the inconsistency of communications remains the biggest disconnect in the claims process.

Sean O’NeillBain & Company

Brokers do not just want information; they want to know what is happening, why it is happening, and what happens next. O’Neill notes that expectations have evolved not in principle but in form and speed – the bar for how quickly and clearly information must be delivered continues to rise, shaped by the digital experiences professionals have in every other area of their lives.

The data from JD Power’s research confirms this picture. According to the JD Power 2025 US Claims Digital Experience Study, released December 2, 2025, receiving adequate digital updates is the top driver of claims satisfaction – yet insurers deliver on this key performance indicator just 22 percent of the time. Overall satisfaction with the auto insurance claims process stands at 700 on a 1,000-point scale, per the JD Power 2025 US Auto Claims Satisfaction Study (October 28, 2025), based on responses from 9,455 customers of the largest US providers. Mark Garrett, director of global insurance intelligence at JD Power, identifies proactive communication as the single most important factor separating the best-rated claims insurers from the rest.

Mark GarrettJD Power

Garrett’s research shows that mobile app experiences now achieve a satisfaction score of 775 against the overall study average of 700 – a 75-point gap. Apps perform particularly well on lower-severity claims where customers who begin the process digitally tend to stay in that channel; however, only 36 percent of auto insurance customers currently receive status updates via mobile app, despite app-based claims handling achieving the highest satisfaction scores. The highest-performing carriers are those that layer digital efficiency over – rather than instead of – human expertise.

That expertise is not a commodity. O’Neill argues that while specialist knowledge in claims handling is critical, it is necessary but insufficient on its own. The real currency of a claims relationship is trust – built or destroyed at every stage of the claims management process, from first notice of loss through final resolution.

How nuclear verdicts are reshaping

US claims

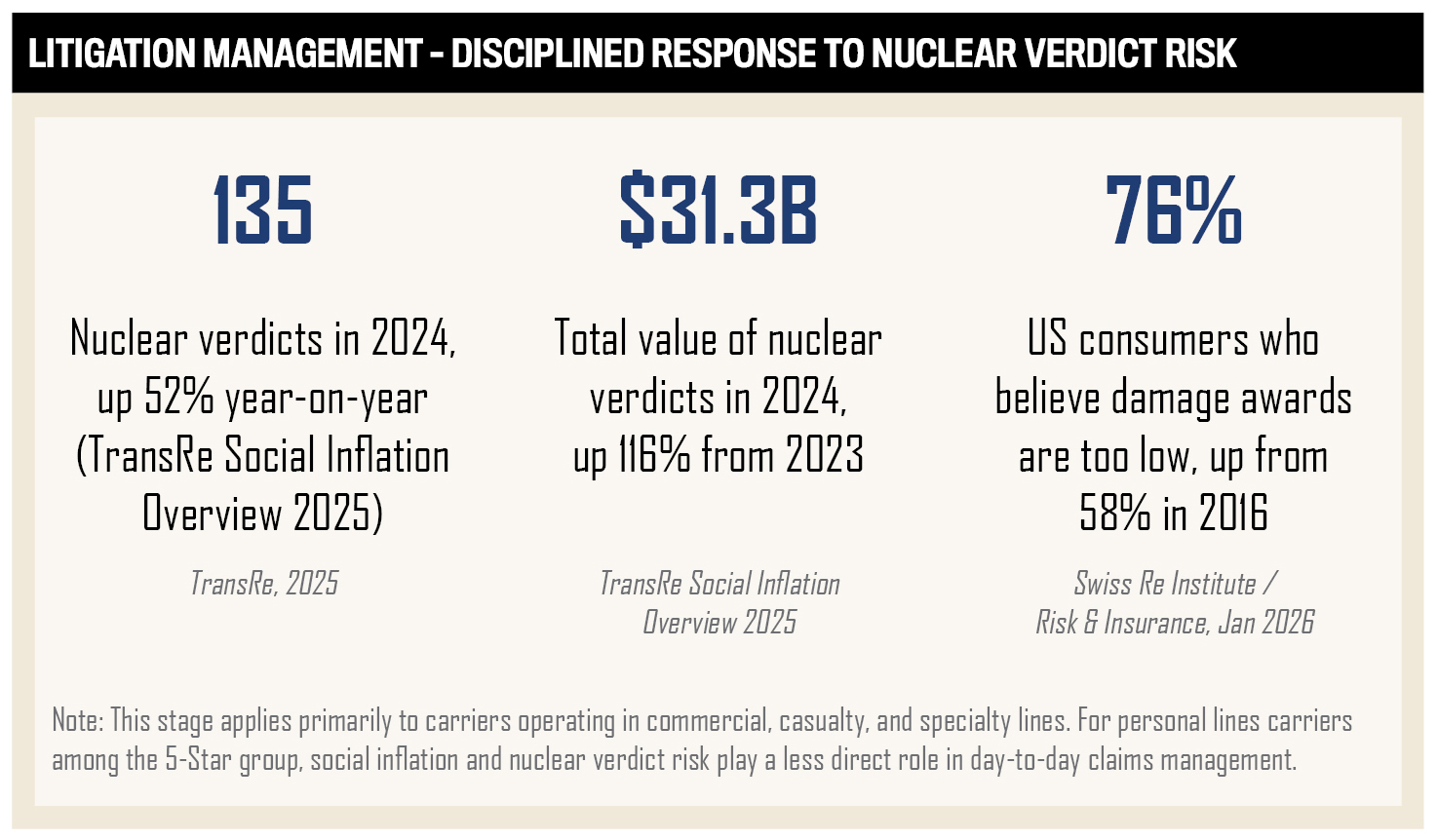

The US litigation environment amplifies the stakes of every claims decision. In 2024, there were 135 lawsuits resulting in nuclear verdicts – jury awards exceeding $10 million – against corporate defendants, a 52 percent increase over 2023, according to TransRe’s Social Inflation Overview 2025. The total value of those verdicts reached $31.3 billion, representing a 116 percent increase from the prior year.

The cultural forces driving this trend are measurable. According to Swiss Re Institute research published by Risk & Insurance in January 2026, 76 percent of US consumers now believe damage awards are too low – up from 58 percent in 2016. That 18-percentage-point shift in public attitude over nine years has fundamentally reshaped what juries consider fair compensation, with direct consequences for commercial lines claims handling across the market.

Attorney advertising and third-party litigation funding have compounded the problem. The US commercial litigation finance industry managed $16.1 billion in assets across 42 active capital providers from mid-2023 to mid-2024, according to the Westfleet Advisors 2024 Litigation Finance Report – providing the plaintiffs’ bar with institutional-scale resources to fund high-value cases. For carriers managing commercial insurance claims, this environment demands rigorous investigation, specialist defense counsel, and a clear strategic approach to litigation management.

The median verdict in cases over $10 million grew from $19.3 million in 2010 to $24.6 million in 2019 – a 27.5 percent increase that outpaced the general inflation rate of 17.2 percent over the same period, per a study of 1,376 such verdicts cited by the US Chamber of Commerce Institute for Legal Reform. The best-rated claims insurers in the 2026 IBA report have built their operations specifically to navigate this environment.

The median verdict in cases over $10 million grew from $19.3 million in 2010 to $24.6 million in 2019 – a 27.5 percent increase that outpaced the general inflation rate of 17.2 percent over the same period, per a study of 1,376 such verdicts cited by the US Chamber of Commerce Institute for Legal Reform. The best-rated claims insurers in the 2026 IBA report have built their operations specifically to navigate this environment.

Markel Insurance – flat, focused, and

built for the long game

A structure built to eliminate delay

When Richard Wolff, managing director of casualty claims at Markel Insurance in New York, describes what makes his casualty claims operation effective, he does not reach for superlatives about technology or proprietary systems. He points to something more fundamental: the way the organization is built.

Markel’s claims operation is deliberately flat. There are a few levels between a desk adjuster and the chief claims officer, and that structure is not incidental – it is by design. In a claims environment defined by rising severity and increasingly complex commercial lines litigation, the ability to escalate a decision quickly and reach the right answer faster than competitors is a tangible competitive advantage.

That flatness also shapes the culture. Senior leadership at Markel is accessible and approachable – a working environment where staff feel supported and engaged, and where engaged staff translates directly into better claims handling outcomes for insureds and broker partners.

Markel’s 2026 IBA submission reinforces this picture. The carrier has invested in deep product-specific specialization – claims teams organized around individual lines of business rather than generalist pools. The philosophy extends to specialist expertise at every level, from a fine arts claims specialist with experience at Sotheby’s to equine and agriculture specialists who are horse owners or former veterinary technicians. The belief is that nuanced knowledge of a client’s world drives better claims management decisions.

In the past 24 months, Markel has continued a structured modernization of its claims platform, rolling out ClaimCenter to improve real-time data capabilities, workflow visibility, and loss run reporting. The carrier has also accelerated litigation management initiatives in direct response to the social inflation and nuclear verdict risk, reshaping the US casualty and commercial lines claims landscape.

Richard WolffMarkel Insurance

Wolff’s assessment of the litigation challenge is direct. Claim severity in the United States continues to increase, driven by attorney advertising, litigation funding, and what he describes as a broader public immunity to large dollar amounts – the same dynamic identified in the Swiss Re Institute and TransRe research. Markel’s response is built on three pillars: rigorous investigation, excellent defense counsel, and a demonstrated willingness to take cases to verdict when appropriate. Without that willingness, Wolff argues, a carrier signals to the plaintiffs’ bar that it will always settle, which ultimately means overpaying on everything.

Q&A: Richard Wolff, Markel Corporation

Q: How is AI currently being used within Markel’s claims operation, and what is your overall philosophy on its role?

A: We are in the infant stages, but it is certainly not growing like an infant – the speed of development is fascinating. We have Copilot embedded in our claims system, and we are piloting a number of applications to have AI assist with triage. The goal is to create efficiencies that free up time for more analytical work. AI changes every day, and while it is designed to assist the human process, it still requires validation. I tell my team: use whatever tools are available to make you more efficient, but at the end of the day, whatever you use AI for, the result has to be correct. We still own the outcome.

Q: How do you think about the balance between AI efficiency and human judgment in claims?

A: I’d analogize it to having 14 clubs in your golf bag. Good players switch them out depending on what course they’re on – but at the end of the day, it’s the player and the swing that creates the ball going in the hole. AI is one of those clubs. I can use it to help get to the right claim result. But you cannot turn a blind eye and say whatever the bot says is the product. There have been lawyers who have gone sideways by allowing AI to write legal briefs that cited case law that did not exist. Judges do not particularly care for that. Neither would I if my team produced something wrong.

Q: What are the most concrete ways you are looking to use automation and AI to improve the employee experience?

A: We have a pilot looking at automating our triage processes to have a file directly assigned to an examiner. Freeing up manager time gives them the opportunity to be more analytical and less administrative. It might be hard to quantify the gain immediately, but I can tell you anecdotally that it will make my 15 managers incredibly happy – and happy means engaged. An engaged staff leads to better results. One feeds the other.

Q: Markel’s casualty claims team earned the 5-Star Claims designation based on broker ratings. What does that recognition mean

to you?

A: I have the privilege of having this conversation, but I don’t do the work. The credit goes to the people in my organization. They are the ones handling claims every day – my examiners and managers. If someone thought highly enough of us to nominate us and brokers rated us the way they did, that reflects the consistency and standards of the people doing the day-to-day work. I want to make that clear.

What a 5-Star claims process looks like

What separates the 16 insurers awarded the 2026 IBA 5-Star Claims designation from the wider market is not a single capability or investment – it is a process. Across every submission, interview, and broker rating in this year’s research, a consistent six-stage framework emerges: the carriers that brokers trust most follow the same fundamental arc, from first notice of loss to resolution, regardless of their size, structure, or line-of-business mix.

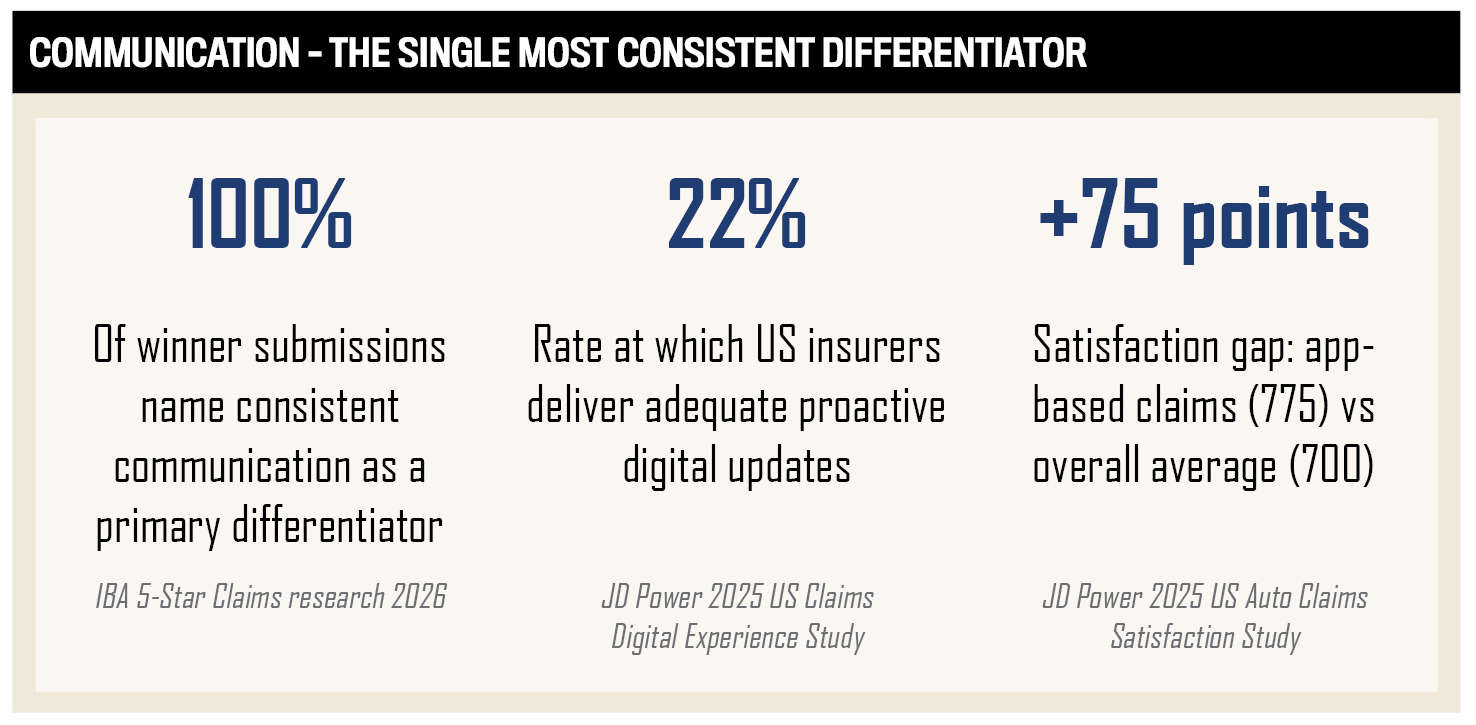

The data from the 2026 winner submissions make this visible in quantifiable terms. Every submitting winner deploys AI or analytics tools – 100 percent adoption among the 5-Star group. And every single submission – without exception – names consistent, proactive communication as a primary differentiator. That last finding is the most instructive, because JD Power’s 2025 US Claims Digital Experience Study shows that insurers deliver adequate proactive updates just 22 percent of the time across the market. The 5-Star carriers are the exception, not the norm.

The six stages below represent what the best-performing claims operations in the US consistently do, drawn directly from the 2026 winner submissions and broker research. They are not aspirational. They are observed.

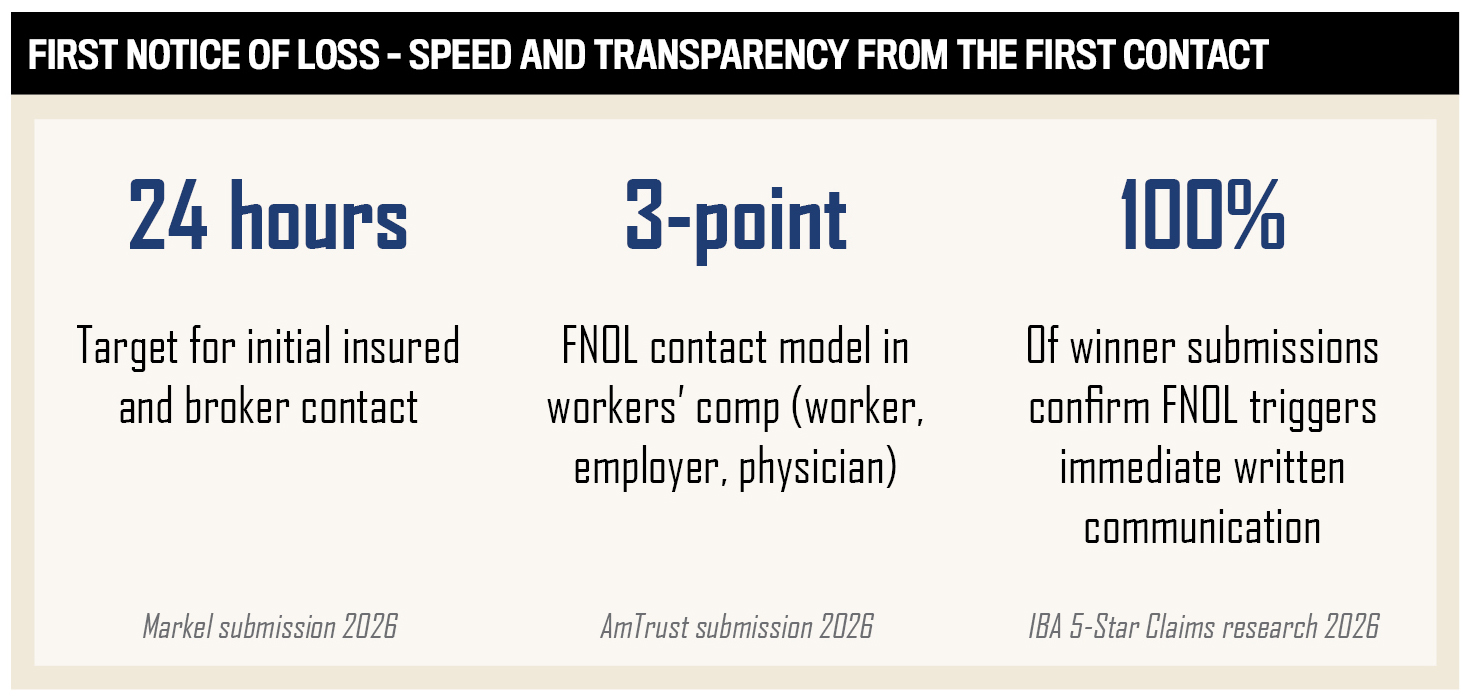

Stage 1: First notice of loss – speed and transparency from the first contact

The 5-Star process begins before the claims team has all the facts. Winners acknowledge claims promptly – typically within 24 hours – and reach out directly to both the insured and broker. An initial coverage position is established as quickly as possible and confirmed in writing, setting clear expectations from the outset. In workers’ compensation, this extends to simultaneous three-point contact between the injured worker, employer, and treating physician from the moment a claim is filed.

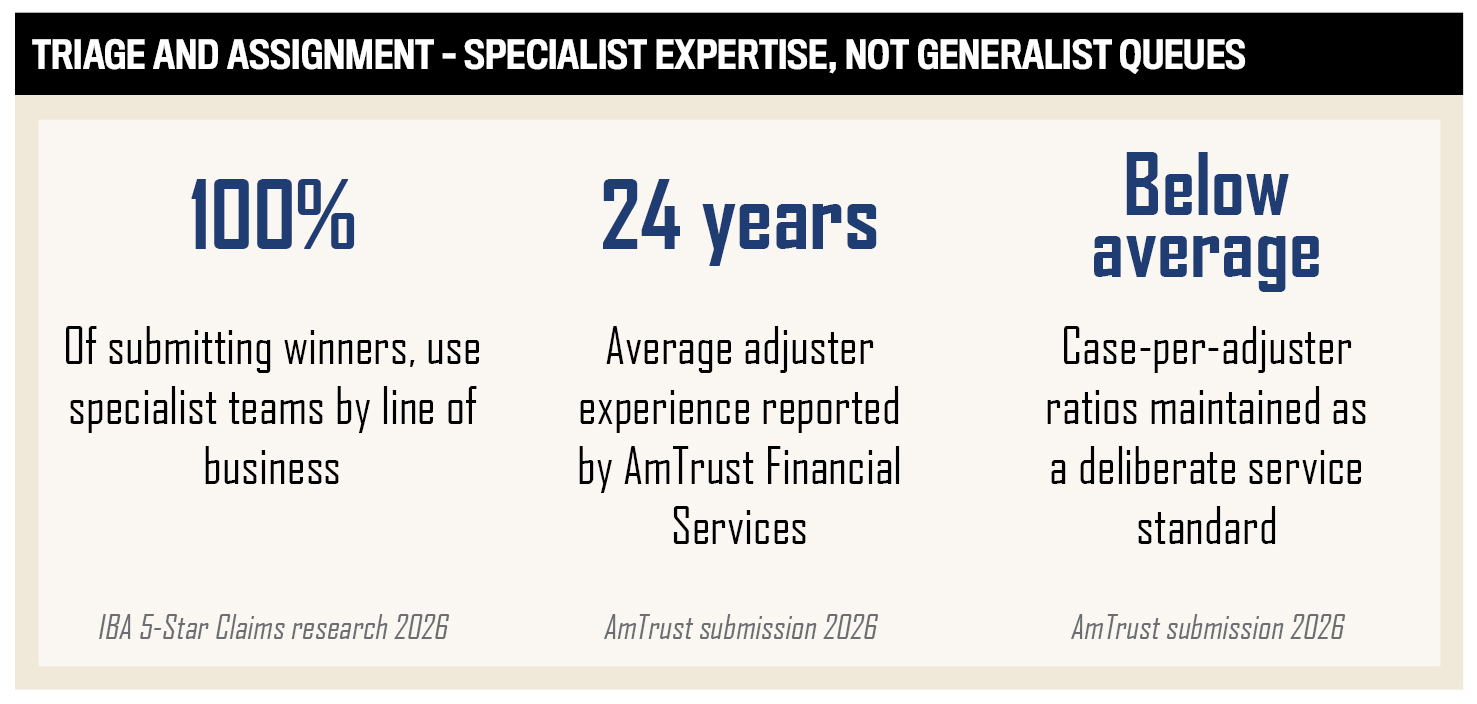

Stage 2: Triage and assignment – specialist expertise, not generalist queues

Every submitting winner routes claims to dedicated specialist teams organized by line of business, never to generalist pools. Deep product-specific expertise is treated as a competitive necessity: Markel’s fine arts claims specialists have worked at Sotheby’s; its equine claims specialists are horse owners or former veterinary technicians. AmTrust Financial Services reports that its adjusters average 24 years of industry experience and maintain below-industry case-per-adjuster ratios to ensure focused attention on every file. Complex and severe losses are escalated to dedicated specialist units rather than handled in the standard workflow.

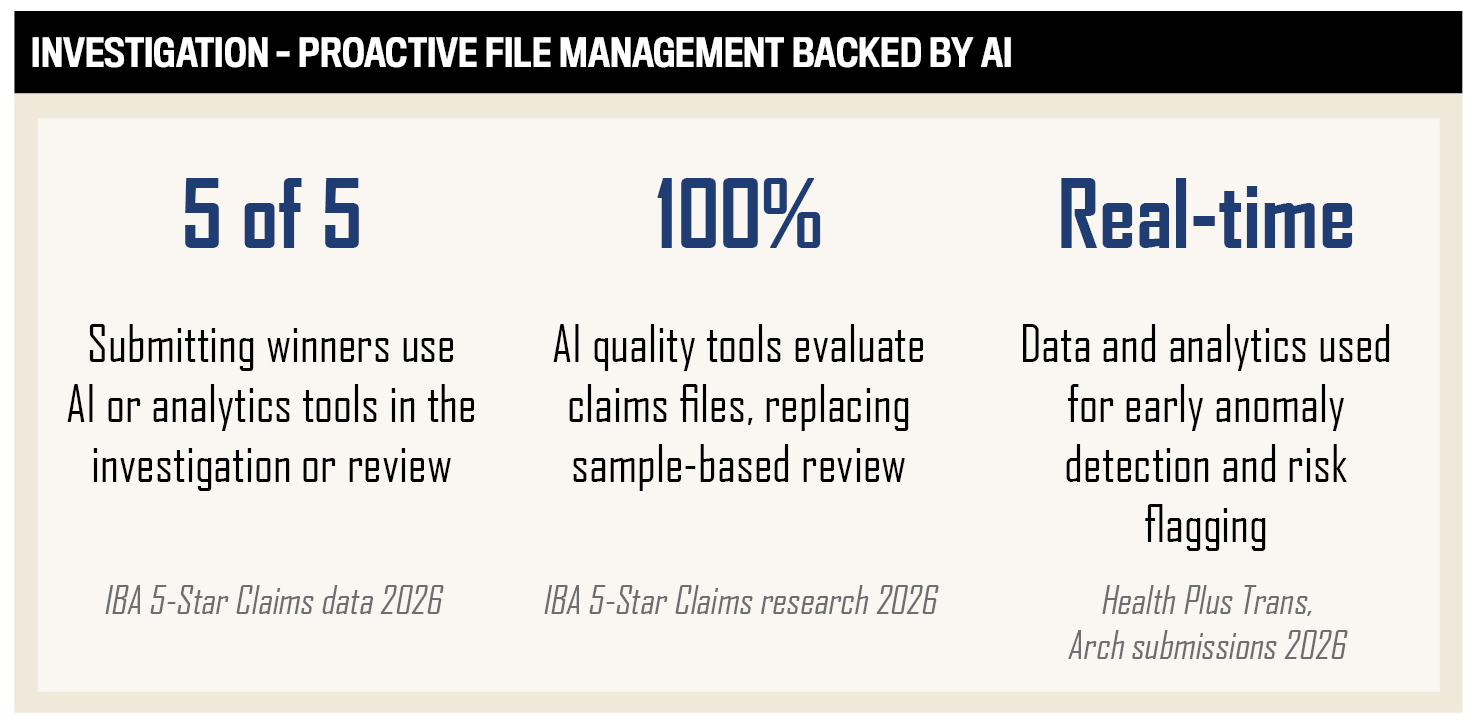

Stage 3: Investigation – proactive file management backed by AI

Winners manage files proactively, with continual reassessment as facts evolve rather than periodic milestone reviews. AI tools are deployed for file review, anomaly detection, fraud flagging, and quality scoring – but in every case, the human adjuster retains ownership of the outcome. The best operations deploy AI quality tools that evaluate claims files continuously rather than on a sample basis, providing real-time feedback to adjusters and supervisors and raising the overall standard of file handling.

Stage 4: Communication – the single most consistent differentiator

Communication is the single finding that runs through every submission, every interview, and every broker rating in the 2026 research. All five submitting winners describe it as a core pillar of their claims operation, not a downstream function. The best performers send proactive status updates – not only when the insured calls – from first notice of loss through final resolution. Settlement strategies and coverage positions are explained clearly and confirmed in writing. Digital channels, including secure two-way texting platforms, mobile app updates, and automated notifications, are used to eliminate the need for follow-up calls entirely.

Sean O’NeillBain & Company

JD Power’s 2025 US Claims Digital Experience Study puts the stakes in stark relief: despite proactive communication being the number one driver of claims satisfaction, US insurers deliver it adequately just 22 percent of the time. The 5-Star carriers have turned that gap into a structural advantage.

Stage 5: Litigation management – disciplined response to nuclear verdict risk

In a market shaped by nuclear verdicts and social inflation, litigation management is no longer a back-office function – it is a front-line differentiator. The 5-Star carriers approach it with strategic intent. Markel’s Richard Wolff describes a three-pillar response: rigorous investigation on every file, the deployment of specialist defense counsel, and a demonstrated willingness to take cases to verdict when appropriate. That last element is deliberate – without it, a carrier signals to the plaintiffs’ bar that it will always settle, which ultimately means overpaying on everything.

Multiple winner submissions reference accelerated investment in litigation management in the past 24 months, with real-time analytics used to identify litigated-claim trends at the portfolio level and refine defense strategy accordingly. In-house coverage counsel is engaged early on complex files rather than at escalation. Allocation and other insurance considerations are addressed proactively rather than at dispute.

Stage 6: Resolution and closure – speed, choice, and closed-loop learning

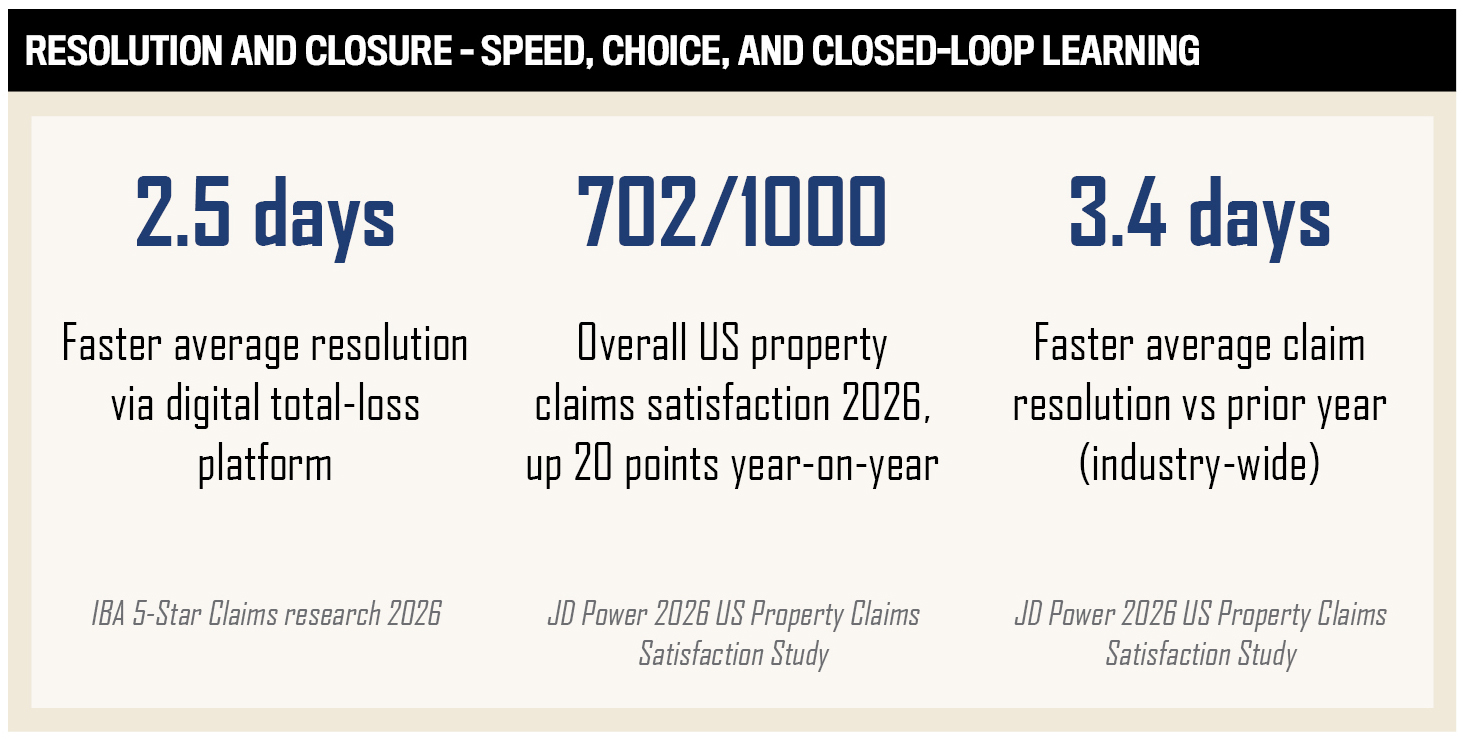

The 5-Star process does not end at settlement – it loops back into the organization. Winners track cycle time and file closure as primary performance metrics, reporting them transparently against set operational goals. Modern payment options, including PayPal and Venmo, are available to reduce friction at final disbursement. For total loss auto claims, leading carriers deploy dedicated digital platforms that coordinate the insured, insurer, and third-party vendors in a single workflow, significantly reducing resolution time.

Critically, winners feed resolution data back into the broader organization. Claim insights and trends are shared with underwriting and actuarial partners, so that closure is not the end of the claim’s value – it is the beginning of better risk decision-making. JD Power’s 2026 US Property Claims Satisfaction Study confirms that this focus is delivering: overall industry satisfaction rose 20 points to 702, with claims resolved 3.4 days faster than the prior year.

The human-technology balance: the thread across all six stages

Across all six stages, one principle holds constant among the 2026 5-Star winners: technology serves people, not the other way around. Every submitting winner uses AI or analytics tools – but everyone frames AI as an efficiency layer that frees experienced adjusters to exercise the judgment, empathy, and relationship-building that technology cannot replicate. Markel’s Wolff puts it plainly: AI is one of 14 clubs in the bag. The player and the swing still determine the outcome.

That balance is harder to achieve than it sounds. According to a Sedgwick report covered by Risk & Insurance in April 2026, only 7 percent of property insurance carriers have achieved scalable AI success in claims operations – despite nearly two-thirds acknowledging a gap between their AI ambitions and current reality. The 5-Star carriers are building in both directions simultaneously: modernizing their technology stack while deepening the specialist human expertise that gives technology its context. That combination, repeated consistently across six stages of a claims lifecycle, is what broker trust is built on.

Industry outlook – the next frontier

The question facing the best claims operations in the United States is not how to match current expectations – it is what comes after them. The JD Power 2026 US Property Claims Satisfaction Study offers an encouraging baseline: overall satisfaction rose 20 points to 702, with claims resolved 3.4 days faster than the prior year. That improvement is real. But it is also uneven, and the carriers that define the next benchmark will be those that understand precisely where the gaps remain.

Sean O’Neill at Bain is direct about where investment has and has not landed. Significant focus has been placed on first notice of loss, intake, and the associated triage – the most visible and digitally tractable parts of the claims lifecycle. Less attention has been paid to investigation, settlement, and subrogation. These are harder to automate, harder to measure from the outside, and harder to differentiate on. They are also where the most consequential claims decisions are made, and where the gap between the best carriers and the rest is widest.

Sean O’NeillBain & Company

For commercial lines carriers in particular, closing this gap requires the same discipline in investigation and settlement strategy that the best operations already apply to litigation management. The 5-Star carriers have demonstrated that systematic investment across the full claims lifecycle – not just its most visible stages – is what produces consistent broker trust over time.

Loss prevention: from reactive to proactive

Beyond closing existing process gaps, the more transformative shift on the horizon is the move from reactive claims management to proactive loss prevention. The signals from connected devices, telematics-equipped vehicles, and smart building systems are creating a genuine opportunity for carriers to help clients reduce and prevent losses before they occur – a fundamentally different operating model from the one the industry has run for a century.

O’Neill at Bain argues that there needs to be an inflection in the total cost of risk in the industry, and that loss prevention will play an outsized role in getting there. The mechanics are straightforward in principle: a carrier with access to real-time IoT data from a commercial property can identify a failing HVAC system, a sprinkler pressure drop, or unusual after-hours entry before they become a claim. A telematics-equipped fleet can surface high-risk driving behavior before it produces a liability event. The same data infrastructure that powers modern claims management can, in theory, be redeployed upstream.

In practice, this requires a significant operational transformation. Most carriers were not built to deliver advisory services or real-time risk monitoring at scale. The carriers best positioned to capitalize on loss prevention will be those that have already invested in the data infrastructure, analytics capability, and client-facing communication frameworks that modern claims management demands – because those same foundations are precisely what proactive loss prevention requires.

What the next benchmark looks like

The 2026 5-Star Claims winners represent the current standard. The next benchmark will belong to carriers that extend that standard into the parts of the claims lifecycle that have received the least investment – investigation, settlement, and subrogation – while simultaneously building the capability to shift from responding to losses to preventing them.

For brokers, the implication is clear: the carriers worth recommending in 2027 and beyond will not just be the ones that handle claims well when they arrive. They will be the ones who demonstrably help clients arrive at fewer claims in the first place. That is a higher bar than any broker satisfaction survey currently measures – and it is where the most forward-thinking carriers in the 2026 5-Star group are already looking.

Conclusion

The 16 insurers recognized in the 2026 IBA 5-Star Claims report did not earn broker trust by accident. Across organizations of different sizes, structures, and line-of-business mixes, a consistent picture emerges: the best claims insurers are flat enough to make decisions quickly, specialized enough to bring genuine expertise to every file, and disciplined enough to use technology as a tool rather than a shortcut.

They communicate clearly and consistently – from first notice of loss through final resolution. They hire people who know their clients’ worlds deeply. They demonstrate a willingness to go to a verdict when the alternative is rewarding a litigation system that feeds on hesitation. And they understand that the measure of a claims operation is not just how efficiently it processes claims, but how well it delivers on the promise that every insurance policy ultimately represents.

In a market shaped by social inflation, nuclear verdicts, and rising expectations from commercial insurance clients, those qualities are not table stakes. They are differentiators – and the 2026 5-Star Claims winners have earned the right to be recognized for them.

Best Insurers for Claims in the USA | 5-Star Claims

- AIG

- Auto-Owners Insurance

- Chubb

- Liberty Mutual

- Nationwide

- Progressive Insurance

- QBE North America

- State Farm Insurance

- The Hartford

- Tokio Marine

- Travelers

- USAA

- W. R. Berkley

Insights

-

Mark Garrett

Mark Garrett

Director of Insurance Intelligence

JD Power -

Sean O’Neill

Sean O’Neill

Partner and Head of the Global Insurance Practice

Bain & Co

FAQ about the Best Insurers for Claims in the USA

What is the IBA 5-Star Claims award?

The Insurance Business America 5-Star Claims award recognizes US insurance carriers that achieve outstanding broker ratings for claims service quality. Brokers rate their insurer partners across key performance indicators, including communication, turnaround times, broker support, operational efficiency, and overall claims handling. Carriers that receive sufficient broker nominations and demonstrate excellence in claims management and broker engagement are awarded the 5-Star Claims designation.

How were the 2026 5-Star Claims winners selected?

IBA conducted a two-phase broker-rated research process for 2026. In phase one, brokers across the United States nominated the insurers they rated most highly for claims service. In phase two, insurers that received sufficient broker nominations completed a detailed submission covering claims capabilities, service standards, turnaround processes, technological innovation, and broker support frameworks. Final designations were based primarily on broker ratings, with additional weighting applied to consistency of service and demonstrated outcomes.

What are the best insurers for commercial insurance claims in the US?

The 2026 IBA 5-Star Claims report identifies the best insurers for commercial insurance claims as determined by professional broker ratings across the United States. The 16 designated carriers – including Chubb, Travelers, Arch Insurance, AIG, The Hartford, and Markel Insurance– consistently score highest for timeliness, transparency, and technical expertise in handling commercial and specialty lines claims – the three factors brokers weigh most heavily in the IBA research.

What do brokers value most in a claims insurer?

According to Sean O’Neill, partner and head of the global insurance practice at Bain & Company in Boston, responsiveness and transparency are the two qualities brokers value most from carriers on claims. Specifically, brokers want to know the status of a claim, understand why decisions have been made, and receive clear guidance on what happens next. The most common source of dissatisfaction is inconsistent communication – carriers that respond well in some cases but not others, or that communicate clearly at first notice of loss but go quiet during claims investigation and settlement.

What are the best insurers for workers’ compensation claims?

Among the 2026 IBA 5-Star Claims winners, carriers with strong broker ratings for workers’ compensation claims handling include AmTrust Financial Services, Markel Insurance, Arch Insurance, The Hartford, and Travelers. AmTrust Financial Services, in particular, operates a workers’ compensation claims model anchored in three-point contact at first notice of loss – establishing communication between the injured worker, the employer, and the treating physician from the outset. The Hartford and Travelers are recognized for their nationwide workers’ compensation claims management infrastructure and specialist adjuster networks.

How is AI changing the claims management process in the United States?

Artificial intelligence is increasingly embedded in claims management across the US market, primarily in triage automation, file review, damage assessment using computer vision, fraud detection, and next-best-action guidance for adjusters. However, according to a Sedgwick report covered by Risk & Insurance in April 2026, only 7 percent of property insurance carriers have achieved scalable AI success in claims operations. Industry experts and leading carriers consistently emphasize that AI is a tool for enhancing claims handling performance, not replacing human judgment. Carriers that use AI to free experienced adjusters for more complex analytical and relationship work are achieving the strongest results.

What is driving rising claims severity in the US?

Rising claims severity in the United States is driven by a combination of structural and behavioral factors. According to TransRe’s Social Inflation Overview 2025, there were 135 nuclear verdicts – jury awards exceeding $10 million – in 2024, a 52 percent increase over 2023, with a total value of $31.3 billion. Attorney advertising and third-party litigation funding have expanded resources available to plaintiffs, while Swiss Re Institute research published in January 2026 shows 76 percent of US consumers now believe damage awards are too low, up from 58 percent in 2016. The result is a harder litigation environment requiring carriers to invest in thorough claims investigation, specialist defense counsel, and a willingness to take cases to verdict.

What is loss prevention, and why is it the next frontier for claims insurers?

Loss prevention refers to the use of real-time data from connected devices, telematics, and smart building systems to identify risk signals and help clients avoid or reduce losses before they occur. Bain & Company research identifies loss prevention as the next major differentiator for US carriers, requiring a fundamental shift from the reactive claims management model that has historically defined the industry to a proactive one. Carriers that can build the data infrastructure, analytic capabilities, and client communication frameworks to deliver meaningful loss prevention will hold a structural advantage in the years ahead.

Methodology

To determine the 5-Star Claims insurers for 2026, Insurance Business America conducted a comprehensive research process leveraging its national network of brokers and industry professionals. Insurers that received a sufficient volume of broker nominations were then invited to complete a detailed submission. This submission required insurers to provide supporting evidence of their claims capabilities, including service standards, claims turnaround times, dispute resolution processes, technological innovation, and broker support frameworks.

The research team analyzed both quantitative survey results and qualitative insurer submissions. Final scores were calculated based on broker ratings across key performance indicators, with additional weighting applied to consistency of service and demonstrated outcomes.

The 5-Star Claims designation was awarded to those organizations that achieved outstanding broker ratings while also demonstrating excellence in claims management, operational efficiency, and broker engagement.

Keep up with the latest news and events

Join our mailing list, it’s free!