The Best Insurance Professionals Under 40 in the USA | Rising Stars

Jump to winners | Jump to methodology

Why 2026 is a defining moment for young insurance professionals in the USA

The best young insurance professionals in America are proving that empathy, human connection, and purpose-driven leadership are not soft qualities – they are the sharpest competitive tools in the industry.

The best insurance professionals under 40 in the USA are stepping into leadership roles at a speed no previous generation has experienced. The US insurance industry is in the middle of one of the most significant talent transitions in its modern history: decades of institutional knowledge are retiring out of the workforce faster than the industry has ever had to absorb, and the professionals filling those gaps are doing so under more pressure and with more opportunity than their predecessors.

Against that backdrop, Insurance Business America launched its 12th annual Rising Stars list in January 2026, inviting nominations for the most exceptional young insurance talent across the country. Nominees had to be 40 or under, committed to a career in insurance, and able to demonstrate a clear passion for the industry.

What the 2026 list reveals cuts against the prevailing narrative about the future of the profession. As artificial intelligence embeds itself into underwriting, claims, and distribution – and as the conventional wisdom says the winners will be whoever has the deepest technology fluency – the insurance professionals rising fastest are making a different argument. They are technically excellent. They know their markets, their products, and their numbers. But when asked what has actually driven their success, they do not reach for a certification or a platform. They reach for empathy.

Four of this year’s Rising Stars – Carter English and Lindsay Fisher of Higginbotham in Texas, Paige Kremer of RT Specialty in the Denver metropolitan area, and Joseph Cook of The Arizona Group– sat down with IBA to share how they got here. Each came from a different corner of the industry: benefits leadership, benefits consulting, specialty brokerage. What they have each arrived at independently, without comparison or coordination, says something important about where the industry is heading – and what it will take to lead it.

Class profile

Who are America's best insurance professionals under 40?

Experience & age

Age distribution

Years in insurance

Who they are

Path & recognition

How they found insurance

Nomination source

Source: IBA Rising Stars 2026 nomination and winner data, n=96 confirmed winners. All figures drawn from winner submission data and the Data for Editorial tab, Insurance Business America, June 2026.

Geographic spread

Where America's best insurance professionals under 40 are based

Winners by state — 22 states represented

Hover any state to see winner count · Darker shading = more winners

Source: IBA Rising Stars 2026 nomination and winner data, n=96 confirmed winners. State data drawn from the Data for Editorial tab, Insurance Business America, June 2026.

The market forces reshaping careers for insurance professionals under 40 in the USA

The numbers behind the talent shift are striking. Mindy Pranculeviciute, a senior recruiter at Talentfoot in the financial services sector, frames the current moment in terms that stop most young professionals in their tracks.

Industry context

A talent crisis and an opportunity — in the same moment

All figures current as of June 2026. Sources: US Bureau of Labor Statistics workforce projections via MarshBerry, March 2025; NAMIC workforce data via MarshBerry; Jonus Group, Navigating the Talent Shortage in the Insurance Industry, October 2025; Cake & Arrow, Why Gen Z is Ambivalent About Working in Insurance, October 2025 (n=519); The Jacobson Group and Aon, Q1 2026 US Insurance Labor Market Study, March 2026.

Mindy PranculeviciuteTalentfoot

The caveat is as important as the opportunity. “Scarcity gets you the interview, not the offer,” Pranculeviciute notes. “The vacuum doesn’t lift you automatically – it rewards the prepared.” That preparation means pairing genuine technical grounding with bridge capabilities: the ability to connect the analytical rigor of traditional insurance roles with modern fluency in data, AI, and people leadership. “Bridges get promoted,” she says.

Brett Carter, vice president and managing director at The Jacobson Group in Chicago – one of the insurance industry’s leading talent and staffing consultancies – sees the same dynamics from the hiring side. The 2026 retirement wave is real, the bench behind it is thin, and responsibility is available to ambitious professionals years ahead of schedule. But Carter is clear-eyed about what separates the top insurance professionals under 40 from those who are simply performing well.

Brett CarterThe Jacobson Group

Three patterns that consistently define top-performing insurance professionals under 40

The 2026 Rising Stars list – proudly supported by the Association of Professional Insurance Women – spans every corner of the US insurance industry. Brokers and underwriters sit alongside claims specialists, insurtech builders, reinsurance professionals, benefits consultants, and marketing leaders. That breadth is itself a story: insurance is not a single career path but a universe of them, and the best young insurance professionals of 2026 have found their place from a remarkable variety of starting points. IBA’s wider recognition of talent includes the best women insurance professionals in the USA, recognized annually through the IBA Elite Women report.

What unites them is more interesting than what distinguishes them. Pranculeviciute identifies three patterns in every exceptional young professional she has placed. First, they own outcomes rather than tasks – they find something broken, fix it, and build the fix into a process that outlives them. Second, they have commercial intuition – they connect their daily work to revenue, retention, and loss ratio, which means they already speak the language of the people who promote them. Third – “the one that surprises people” – they invest in others early.

Mindy PranculeviciuteTalentfoot

That third pattern runs through the 2026 Rising Stars list like a thread. It is visible in the scale of mentorship programs these insurance professionals have built, in the way they describe their careers not as individual achievements but as team outcomes, and most directly in the profiles of this year’s three featured winners.

Carter English: employee benefits leader and one of America’s best insurance professionals under 40

Carter English did not plan to sell insurance. He planned to coach football. After a playing career that required five hip surgeries and a stint working in the NFL, English transitioned into employee benefits at Higginbotham in Texas, where he spent his first few years uncertain whether the work meant anything at all. The turning point came not from a deal closed or a quota hit, but from a phone call.

An elderly man whose wife had been diagnosed with cancer had struggled to find coverage for her. English had helped him navigate the options and secure medical insurance. About six months later, the man called back. “He’s crying on the phone,” English recalls, “and he said, ‘I just wanted to let you know that my wife passed away a couple of weeks ago, but that I feel like I got six more months with her because of you.’”

English pauses on the memory. “I remember just thinking, like, oh wow, I guess the work that I do does have some impact.” Around the same time, his direct report – the person he would eventually replace in the role – sat him down after he had been venting about finding no meaning in the work. The advice he received reframed everything: treat the money and the opportunity not as financial metrics, but as a chance to be generous to the people around you. Two events, close together, and English was committed to the industry in earnest.

Today, English leads Higginbotham’s employee benefits practice nationally. Higginbotham is the 15th largest insurance broker in the United States, with 130 offices across 22 states and approximately 700 salespeople who report to English’s organization. But what distinguishes him among his peers is not the scale of the role – it is that he has deliberately refused to stop doing the job while leading it.

Carter EnglishHigginbotham

English describes his approach as that of a “player-coach.” Most leaders at his level drop their sales responsibilities when they step into national leadership roles. English has not. He still carries an active book of business, sourced largely from partners across the Higginbotham footprint who ask for his involvement on complex accounts. He does not split commission. He is doing it because he believes a leader who does not live the same daily reality as their team loses credibility – and with credibility goes influence.

The approach is working in measurable terms. When English stepped into the role, Higginbotham’s employee benefits practice had grown 5 percent organically the year prior, against an internal target of 10 percent or above. Over the following two years, the practice recruited more than 150 new producers and retained more than 83 percent of them. Current year-on-year organic growth is above 12 percent.

English is careful about how he defines success. Revenue and growth figures, he says, are “hopefully just byproducts of doing a great job.” What he actually measures is whether his people leave the office with enough energy left to be present at home.

That philosophy has been shaped, in profound ways, by English’s daughter Isabel, who was born with Down syndrome. The day she was born was the day the family found out. He describes the initial experience honestly: the depression, the grief, the sense that every aspiration he had held for his child had vanished. What replaced those feelings was something he now considers more important than anything he has achieved professionally.

Carter EnglishHigginbotham

Isabel, now almost four years old, has changed how English grades himself and the people around him. He and his wife founded a school for children with special needs; he serves as president of the board. He describes the shift in his definition of success – away from resume achievements and awards, toward happiness, health, and passion – as “honestly just life giving.”

Higginbotham placed six employees on the 2026 Rising Stars list – believed to be the most of any single agency in the report’s history.

Why Carter English is one of the best insurance professionals under 40 in the USA

English’s story captures everything that defines this year’s Rising Stars class. He entered insurance without a plan, found meaning through a moment of genuine human impact, and built a leadership model around staying close to the work and the people doing it. He recruits 150 professionals, retains more than 83 percent of them, and leads a practice where annual revenue grew by more than 12 percent – not because he has the best systems, but because the people in his organization feel genuinely invested in what they are doing. That is the human edge in practice.

Q: How did a football coach become one of America’s best insurance leaders?

A: As a football coach, you’re constantly trying to mentor, inspire, recruit – do all the things to try to build a team and a culture. When I first transitioned into insurance, my first few years, I struggled to find a kind of meaning and purpose. But then, as I found purpose and passion in this work, I started to really see it. Now I tell people all the time that I feel like I just coach and recruit every day.

Q: Why does a national insurance practice leader still carry his own book of business?

A: If I’m asking people to do certain things every day and I’m not doing it actively and participating in it, then who am I to be that person? When I hear complaints, it’s not foreign to me because I’m probably seeing it with my own clients. We’re not in an ivory tower – we’re on the field with them.

Q: How do you define success as an insurance leader?

A: I always view the revenue and financial metrics as hopefully just byproducts of doing a great job. I hope that we create an environment of healthy external competition and joy in their work so that our people can go home and feel like they got wind in their sails – because work didn’t beat them down.

Q: Has your daughter, Isabel, changed how you lead people?

A: When she was born with Down syndrome, I remember thinking every dream and goal and aspiration I had for my child’s life was all gone now. And then you start to realize, what do I want for her? I want her to be happy and healthy, and I want her to find things that she loves. And so I have to check myself and say – if I believe God made her on purpose, then I can’t give her a different scorecard than I give myself. That changed my perspective on how I grade other people and how I grade myself. It’s been honestly just life-giving.

Q: Where does one of America’s top insurance leaders under 40 want to go next?

A: The competitor in me – I’d love to be a CEO one day. I’d love to run an entire agency. But I also tell myself all the time, if this was the best role that I ever had, then I did way better than I ever deserved. I really fight to be super content in my current state and hopefully just lead really well.

Lindsay Fisher: benefits consultant and one of the USA’s best insurance professionals under 40

Lindsay Fisher did not set out to become a benefits consultant. She was working in human resources – as a generalist, “a department of one,” as she puts it – when she hired Higginbotham as her company’s broker. She built strong relationships with the team there, stayed in touch after leaving that employer, and when an opportunity came to join the firm, she took it. She took a pay cut to do it. She joined as the first account coordinator in her region.

That origin story matters because it explains something about how Fisher approaches every client conversation. She has sat on the other side of the table. She knows what it is like to be the HR leader who has to understand a benefits renewal, explain it to a CFO, and then explain it again to 500 employees who just want their insurance to work when they need it. That experience does not just give her credibility – it gives her a specific kind of empathy that is hard to train.

Lindsay FisherHigginbotham

Fisher also holds an accounting degree and has worked in accounting, which she describes as equally important. Benefits consulting is ultimately a financial discipline: funding structures, actuarial analysis, renewal negotiations, and long-range cost containment. Fisher moves between the human and the financial dimensions of the work without treating them as separate. That combination – knowing what the P&L looks like and knowing what it feels like to be the employee whose cancer treatment just got denied – is the core of her practice.

Her most significant technical achievement over the past year was the migration of one of the largest Individual Coverage Health Reimbursement Arrangements (ICHRAs) of its kind to a new platform. An ICHRA is an innovative employer funding model that allows businesses to reimburse employees for individual health insurance premiums rather than sponsoring a group plan. Fisher is one of a small number of benefits consultants in the country who specialize in the model. The migration involved moving more than 1,000 employees and 1,000 individual policies from one platform to another in 2025.

Over three years of tracking renewal data, the average medical renewal across Fisher’s client portfolio has come in under 5 percent – a figure that includes the 2026 renewal cycle, widely regarded as one of the most challenging markets in recent memory.

But the achievement Fisher describes with the most animation is not the ICHRA migration. It is a phone call. A younger employee at one of her client organizations – the same age as Fisher – had been diagnosed with a rare form of cancer and was traveling to another state for treatment. He was trying to navigate the claims process at the same time he was navigating a life-altering diagnosis. Fisher spent days working with the carrier to ensure his imaging approvals were processed and his claims were moving.

Lindsay FisherHigginbotham, recalling a client employee’s message

Fisher talks about this case – and others like it, including a crane accident where an operator’s legs were crushed, and she deployed mental health resources for employees who had witnessed the event – not as extraordinary moments but as illustrations of what the job is for. “I think that brings me the most joy,” she says, “to feel like I can lift some of that stress off of people that are going through really challenging periods.”

On the question of AI, Fisher is neither resistant nor evangelical. She is using it to make back-office tasks faster and to help her articulate complex issues more clearly. But she frames her relationship with AI in terms of what it cannot do, not what it can. “I think the human element of what we do is really important,” she says. “I think it’s a differentiator, especially now going into this AI phase – and I think it’s even more important to continue to maintain now as we move into this new era.”

In 2024, Fisher received the Higginbotham Pinnacle Award for Excellence in Financial Services – a company-wide honor presented to one individual across a workforce of approximately 4,000 employees.

Why Lindsay Fisher is one of the best insurance professionals under 40 in the USA

Fisher’s career is built on a foundation most insurance professionals do not have: she has been the client. She has sat in the HR chair, navigated the benefits renewal from the employer’s side, and experienced firsthand what it means to have coverage that does not work when someone needs it. That perspective, combined with her accounting grounding and her deep technical knowledge of ICHRA structures, makes her an unusually complete advisor. Her 2024 Pinnacle Award – one recipient across 4,000 employees – is the institutional confirmation of what her clients already know.

Q: What quality gives you the edge as one of America’s top benefits consultants under 40?

A: I think that it’s basically empathy. And I think that comes from the fact that I used to be in HR – that’s where I started my career. It’s like just never losing sight of the fact that there are people at the end of it when we’re looking at financials and reviewing strategy. Being able to really add the human touch and continue to maintain it – especially with all of the AI stuff we’ve got going on – I think it’s even more important to continue to maintain now as we move into this new era.

Q: Does your HR background change how insurance clients receive you?

A: You sit down at the table with the HR team and with the other leadership folks, and they are like, ‘Oh, you get what it’s like to be on my side of the table.’ And so you create that credibility and that instant kind of rapport. I have an accounting degree as well, and I’ve worked in accounting. Having the understanding of the whole business and how this one benefits things impacts the broader picture of a P&L – that’s been helpful for me to have in my pocket.

Q: What brings a top young insurance professional the most satisfaction in this work?

A: Whenever we can help employees navigate a really challenging situation. Recently, I had an employee at one of my clients – he was diagnosed with a rare form of cancer, the same age as me – and he reached out. He emailed me after a couple of days and was just like, ‘This takes such a huge load off of me as I’m trying to figure this out. It’s so confusing and so overwhelming.’ That brings me the most joy – to feel like I can lift some of that stress off of people going through really challenging periods.

Q: How does a leading insurance professional under 40 think about AI in their practice?

A: I’m embracing it, but the way I’m viewing it from my position is – I think the human element of what we do is really important; I think it’s a differentiator, especially now going into this AI phase. I have been using AI to help me with some of those back-office-type things – just to make me faster, more efficient. But the human element? That’s still mine.

Q: Why did you move from being a generalist HR professional to specializing in benefits?

A: When I was in HR, I was essentially like a department of one. You kind of know a little bit about a lot of things. Once I had done that for a while, I thought I would really like to specialize in something. I’d like to be an expert in a thing. And I landed in health and welfare, which is where I am today. I like the fact that I now specialize in one thing, and people can come to me for that.

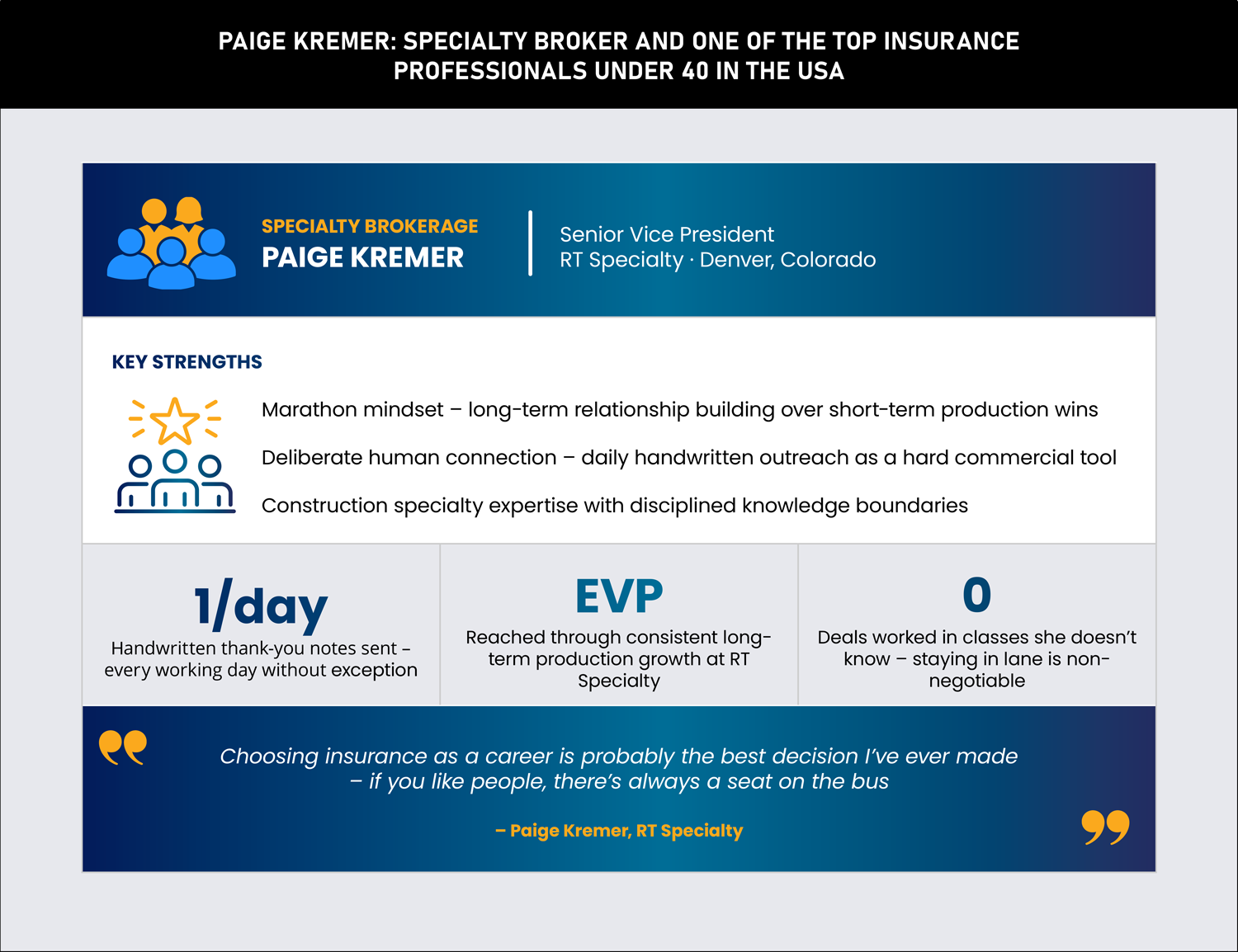

Paige Kremer: specialty broker and one of the top insurance professionals under 40 in the USA

Paige Kremer answers the phone from a plane. She has just landed, looks “a little disheveled,” and is not going to let that stop her. It is a small moment that captures something essential about her: she has built a career out of showing up, and she is not going to stop showing up because she is tired.

Kremer is a specialty broker at RT Specialty in Greenwood Village, Colorado – part of the greater Denver metropolitan area – where she focuses on construction risks. She has spent years building a book of business that is now large enough that she cannot service it alone – a problem she has spent the past 12–18 months solving by building and trusting a team. She is married to another RT broker. Many of her closest friends are underwriters. She describes insurance not as a job that she does but as a world she lives in. That is not a complaint. It is the source of her competitive advantage.

The most distinctive thing about Kremer’s practice is also the simplest: she writes a handwritten thank-you note every single day. It happens in the morning, with her coffee, before anything else. The recipients are underwriters, clients, retail agents, colleagues – anyone she wants to make feel seen. She did not arrive at this practice through a book or a training program. She arrived at it through a conviction about what endures.

Paige KremerRT Specialty

This is not a soft gesture in a hard industry. It is considered a commercial strategy. Kremer does not benchmark herself against other brokers – she considers the comparison a trap. “You’re comparing apples to oranges every day if you do that. I think it sets people back.” Instead, she focuses on standing out as a human being rather than a producer. The handwritten notes, the real conversations, and the genuine curiosity about what makes the person on the other end of a deal tick – these are the things that make retail agents bring their deals they could take to anyone.

Kremer is also a precise and disciplined technician. Her professional development does not happen in classrooms. It happens by taking on increasingly complex deals and not letting herself bluff through the ones she does not fully understand. She describes this in terms of glass balls and rubber balls. Rubber balls can be dropped – they bounce back. Glass balls cannot. As her career has progressed and the glass balls have multiplied, the requirement to genuinely know her market has grown with them.

Paige KremerRT Specialty

On AI, Kremer is consistent with the position her two fellow featured winners have independently staked out. Her team uses AI every day. She is clear-eyed about where it adds value: analyzing lengthy submissions that run to hundreds of pages, supporting back-office efficiency. She is equally clear-eyed about where it fails. “AI won’t tell you if it doesn’t know the answer – it’ll tell you whatever it thinks the answer is. Which I think is quite dangerous.” Her team treats AI as a tool, not a teammate.

Kremer’s views on work-life balance are characteristically direct. “As a salesperson, work-life balance is just not realistic.” She has integrated her professional and personal lives rather than separating them. Her best friends are underwriters. Her husband is a broker. She does not present this as a sacrifice. She presents it as the natural outcome of genuinely loving what you do and the people you do it with.

Paige KremerRT Specialty

Kremer is also building for a future that extends beyond her own production. Over the past 12-18 months, she has been hiring, training, and learning to let go of the reins – trusting her team to service accounts she has spent years building. She hires mostly from outside the insurance industry, preferring to train people from scratch. She insists on being back in the office with her team because she believes that training the next generation requires physical proximity and the small daily moments that remote work cannot replicate.

Why Paige Kremer is one of the top insurance professionals under 40 in the USA

Kremer’s career is built on a philosophy that is both simple and rare: stand out as a human being first, a broker second. The handwritten notes, the marathon mindset, the refusal to work in classes she does not know inside out – these are not personality quirks. They are a coherent commercial strategy that has delivered consistent production growth in both hard and soft markets. At 38, as an SVP at one of the country’s leading specialty brokerage firms, she is now doing something equally important: building the next generation of insurance professionals in her own image.

Q: What quality has most driven your success as a top insurance professional under 40?

A: I think empathy has always been a really, really strong trait for me, and I actually want to know what makes everyone around me tick. I think it’s very easy to become mechanical in what we do – in any business where you’re doing sales, it’s very easy to get robotic and kind of hide behind a computer. But I’ve always loved finding out what makes a person tick more than sending an email.

Q: Why does one of America’s best specialty brokers write a handwritten note every single day?

A: I try to really just focus on what I do versus what everyone else is doing. Standing out as a human – taking the time to write handwritten thank you notes to people every single day. I read somewhere that when all is said and done, and you’ve retired, the one thing you leave behind is your written word. People are hanging that up at their desks to egg them on to go get more new business or to do another deal for you. It sticks around. Whereas you’re pretty likely to forget an email.

Q: How should a rising insurance professional think about AI?

A: We use it quite a bit. We double-check it every single time – AI won’t tell you if it doesn’t know the answer; it’ll tell you whatever it thinks it is. Which I think is quite dangerous. So we’re certainly using it every day, but we’re using it more as a tool, not as a teammate. It’s helpful for analyzing a submission that is hundreds of pages long. But you could never rely on it for the more human aspects – like interpreting a coverage or knowing which markets are going to take the best care of you on a deal.

Q: What advice does a top insurance EVP under 40 give on building a team?

A: At some point, your book becomes sizable enough that you really just can’t do it all yourself. The babysitting is so bad for everyone. You can only babysit so long in your career. You gotta let people do what they do best. I’ve hired mostly from outside the insurance industry, which has been really fun because then you can teach them everything from square one, and they can develop their own habits.

Q: What does a career in insurance offer a young professional?

A: Choosing insurance as a career is probably the best decision I’ve ever made because I think if you like people, there’s always a seat on the bus in insurance. If I didn’t love brokering, if I wasn’t good at sales, I could have done underwriting – there are so many different roles. And if you can grow in a soft market, you can explode in a hard market.

Joseph Cook: cyber liability specialist and one of the best insurance professionals under 40 in the USA

Joseph Cook did not plan to work in insurance. The industry found him, as it found the majority of the 2026 Rising Stars class. What Cook did with that accidental entry is less accidental: 12 years later, he leads a technology, life sciences, and cyber liability practice group at The Arizona Group in Phoenix, Arizona, manages a $2.1 million revenue book, leads a team of eight, and holds a seat on the national board of the Young Risk Professionals. He is also, starting this August, heading to Carnegie Mellon for an eight-month master's program in cyber liability insurance. The accumulation is deliberate. The philosophy behind it, he says, is simple.

Joseph CookThe Arizona Group

Cook is careful not to let that word land softly. Empathy in his practice is not a warm style or a communication preference. It is a professional obligation – and in Arizona, a legal one. Arizona is one of only three states in the United States in which a licensed broker's duty to advise is held to the same standard as a doctor or an attorney. That shapes every difficult conversation Cook has with a client, including the ones they do not want to have.

He describes one such conversation in detail: a client who wanted to cancel a $758 annual policy despite having contracts that required the coverage. Cook knew what the consequences of cancellation would be – a certificate of insurance issued to municipalities and private entities would require notification, potentially pulling the client off active jobs until coverage was restored. He tried to advise the client. The client escalated.

Joseph CookThe Arizona Group

The story is told not as a complaint but as an illustration. Cook’s point is that the hardest part of insurance is not the technical work – it is communicating potential future crises to people who are not currently in crisis, who may have been in business for 15 or 20 years without a meaningful incident, and who interpret that track record as evidence they do not need the coverage they have. Against that psychology, empathy is a diagnostic tool, not just a communication style.

Cook frames his role in broader terms. His clients are not simply buying a financial product. They are businesses that create risk in their communities – 35 electrical contracting vehicles on public roads, construction equipment in shared spaces, technology platforms handling sensitive data. Cook's job, in his view, is to ensure that those who profit from operating in the community are also responsible for the risks they generate.

Joseph CookThe Arizona Group

Outside of his client work, Cook is building infrastructure for the next generation of insurance professionals in ways that are, again, not accidental. He is the founding chair of the Young Risk Professionals Phoenix Chapter, the sitting vice chair of the Young Risk Professionals National Board, and co-chair of Young Insurance Professionals for the Big I of Arizona. He is an adjunct faculty member at Northern Arizona University's emerging Risk Management and Insurance program, and is actively working with the university to develop a full four-year degree in risk management and insurance – writing curriculum, fundraising, and advising. He mentors new producers at The Arizona Group, participants in the Braven program, and students at NAU.

His CEO's endorsement in his nomination submission describes him as “a dynamic leader shaping the future of the insurance industry in the communities he serves.” In 2025 alone, Cook delivered 22 speaking engagements across webinars, panels, and podcasts; was named 2025 Producer of the Year at The Arizona Group; and was recognized as a 2025 Committee Chair of the Year by the Big I of Arizona.

In August 2026, Cook begins the eight-month Carnegie Mellon Chubb Cope Insurance Certification (CCIC) program in cyber liability insurance – a rigorous postgraduate qualification that combines campus time in Pittsburgh with virtual learning and a capstone project. It is the kind of credentialing that most people in the industry do not pursue. For Cook, it is the logical next step in a career built on accumulating hard expertise. His declared goal is a $3 million revenue book by 2030. He is currently at $2.1 million.

Why Joseph Cook is one of the best insurance professionals under 40 in the USA

Cook’s career is built on a conviction that most professionals in his industry articulate but fewer actually operationalize: that insurance, done correctly, is a form of community service. He arrived in the industry by chance in 2014. What followed was entirely by design – a $2.1 million book, a specialty practice group, two professional body chairmanships, an adjunct faculty role, a curriculum project, and a Carnegie Mellon qualification starting in August. He is 37. The human edge the 2026 Rising Stars class embodies is perhaps most explicitly stated by Cook himself, who frames both empathy and responsibility as professional superpowers in an industry that has historically priced neither.

Q: What is the quality you feel has most driven your professional success?

A: What I lean into the most right now is empathy. I feel like that’s just a really powerful tool in communicating with human beings and trying to arrive at outcomes that are fair and with integrity and that we can all feel good about at the end of the day. Right. Even if sometimes you don't get the, let's call it, desired business outcome. You're really, really, really trying to conduct your business in such a way that you feel good about it and that you would hope anybody else conducting business would do the same for you or your family.

Q: You work in Arizona, which has an unusually high duty-to-advise standard for brokers. How does that shape your practice?

A: In my state, in Arizona, we are one of three states in which my duty to advise is on the same expectation as a doctor and attorney. So if I know what my duty to advise is, and I'm very acutely aware of that, I know I have to have this conversation with him whether he enjoys it or not. All I try to do is practice what I believe is empathy and good consultation. Sometimes to be empathetic, you have to have conversations that can be challenging. Or to maybe make it a little simpler – you have that example of being nice versus being kind. It's nice for nobody to tell you and ignore it and act like it's not there. It's kind for somebody to quietly tell you, hey, man, you got a little lettuce.

Q: How do you communicate with clients who resist your advice?

A: You absolutely have to work on being a bit of a chameleon, if you will, and remembering and recognizing who wants to be communicated to in what way. Some people just facts. Some people, how's the wife, how's the kids. Some people need softer language. Some people need you to be a bit firm for them to take it seriously. Some people it's phone; some people it's email. You're not going to achieve any meaningful results or put together any meaningful insurance programs with your clients if you can't communicate with them in the way that they want to be communicated to.

Q: Fatherhood has clearly changed your perspective. How has it affected your professional approach?

A: Some of the things that I used to have more patience for, I have a lot less patience for after my son is here. I think about my son in 30 years and owning a business. And I'm like, man, if my son ever talked to someone the way this person is talking to me right now, I would not feel good about the job I did as a father. I'll do my job and I'll be as good as I can be at it. But our business hours are 8 to 5 and you might think you're pretty important, but after 5 o’clock, there ain’t nothing more valuable than my son and my wife.

Q: What does a career in insurance mean to you, and what do you want the next generation to understand about it?

A: A career in insurance can be not just personally fulfilling but a true act of community service if pursued intentionally. My aspirations are to create as many pathways and connections for others as I possibly can. This industry has been wonderful to me, I want to share that with as many people as I can. Empathy, if you lead with care for others and a desire to understand their perspective you will undoubtedly do well. A close second would be taking responsibility – it can be a super-power.

How the best insurance professionals under 40 are preparing for an AI-driven industry

The forces shaping the 2026 Rising Stars list are not going away. The retirement wave will continue to transfer institutional knowledge and leadership responsibility to a younger generation for the foreseeable future. AI will continue to embed itself into the technical infrastructure of the industry – underwriting algorithms, claims automation, and distribution analytics. The insurance professionals who thrive in this environment will be those who understand both sides of that equation: what the technology can absorb and what it cannot.

Brett Carter of The Jacobson Group is direct about the opportunity for those who are prepared. “The professionals who are curious, adaptable, and willing to continuously learn will find themselves with opportunities that simply didn’t exist for previous generations.” His advice to young insurance professionals on AI is equally direct: genuine fluency is not about becoming a data scientist or technology expert. It is about understanding how to effectively leverage AI to improve decision-making, increase productivity, and create better outcomes – while still applying the critical thinking, judgment, and relationship-building skills that remain uniquely human.

What the data says about AI, careers, and the human advantage through 2035

Mindy Pranculeviciute of Talentfoot makes the same point in starker terms. “Build evidence, not hope,” she says. “Every Rising Star I’ve ever placed could instantly answer one question: ‘What’s measurably different because you were in that seat?’ You’re always building the case for the role you want next; the only question is whether you’re doing it deliberately.”

Conning’s 2025 C-suite survey of US insurance executives found that 55 percent of respondents are now at early or full adoption stages for generative AI – up from minimal utilization the prior year – and that the insurance workforce is expected to be reshaped by 2035, with roles adjusted to value customer relationship skills and technological literacy more highly than repetitive task execution.

Industry outlook

AI is embedding fast — accelerating demand for what it cannot replace

Sources: Datagrid, AI Agent for Insurance Statistics, December 2025 (citing BCG research); Conning, AI in Insurance: The C-Suite Verdict, June 2025; KPMG, 2025 Insurance CEO Outlook (110 insurance CEOs surveyed); Simplifai agentic AI deployment report, cited by CIO Dive, April 2026. Underwriting 2028 projection per Datagrid/BCG. All data current as of June 2026.

The 2026 Rising Stars are already building that evidence. They are doing it in benefits practices in Texas, in specialty brokerage in Denver, in construction excess underwriting in Illinois, in claims operations in Ohio, and in dozens of other roles across the country. What connects them is a shared conviction that the industry’s future does not belong to whoever automates the most – it belongs to whoever builds the best relationships, invests most deeply in the people around them, and shows up with genuine empathy in every interaction.

What defines the best young insurance professionals in America

The 2026 IBA Rising Stars list is the 12th edition of a report that has tracked the industry’s emerging talent since it began. Each year, the list reflects something true about the moment the industry is in. This year, the signal is unmistakable.

In a period defined by technological disruption, compressed career timelines, and a generational transfer of knowledge that has no precedent in the modern history of the profession, the professionals advancing fastest are not the ones who have simply acquired the most technical credentials. They are the ones who have understood something more fundamental: that insurance, at its core, is a people business. It is a business built on trust, on the relationships that hold when a claim comes in or a renewal goes sideways, on the human judgment that sits behind every risk assessment and every client conversation.

The best insurance professionals under 40 in the USA have technical depth. They know their markets, their products, and their numbers. But what sets them apart – across backgrounds, specialisms, and geographies – is a deliberate, conscious investment in the human dimension of their work. They mentor. They show up in person. They write handwritten notes. They sit with employees in the worst moments of their lives and help them navigate a system designed to confuse them. They build teams by trusting people rather than babysitting them. They stay on the field with their people rather than retreating to the ivory tower. They build curriculums at universities. They frame insurance not as a product but as community service.

In a year when the industry is rightly focused on the question of what AI will change, the 2026 Rising Stars are answering a different question: what will never change. The answer, it turns out, is the human edge.

The Best Insurance Professionals Under 40 in the USA | Rising Stars

- Alec Ossorio

Manager, Commercial Insurance

Burns & Wilcox - Alexandra Santo

Manager, Professional Liability Claims

Golden Bear Insurance Company - Amber Allen

National Senior Marketing Director

AmeriLife Marketing Group - Amber Gregg

Litigation House Counsel

Progressive Insurance - Andrea Oldenburg

Director of Growth and Client Strategy, Real Estate, and Vice President

Lockton - Andrew Howard

Director, Risk Management and Global Risk Solutions (West Series)

Lockton - Aristotle Moulopoulos

Director of Entertainment

Alive Risk - Arlene Duran

Client Manager

C3 Risk & Insurance Services - Blaine LeBlanc

Vice President

Amwins - Brandon LaSpina

Senior Analyst – Cyber and Technology

EPIC Insurance Brokers & Consultants - Brett Ullman

Underwriter

Chesapeake Employers’ Insurance - Brian Thornton

Property Broker and Vice President

CRC Group - Britt Bowens

Senior Product Marketing Manager

Aspida - Brittany Bishop

Vice President, Employee Benefits

Higginbotham - Brooks Cochran

Executive Vice President, Casualty

Amwins - Caleb Merlain

Assistant Vice President, Private Client Services Manager

Personal Risk Management Solutions - Cameron Devine

Assistant Vice President, Binding Authority

XS Brokers - Casey Welch

Claims Auditor

insuranceclaim123.com - Chase Marable

Managing Director, Shareholder, Regional Sales Executive, and Missouri Office Leader

Higginbotham - Chris Bohn

Director of Wholesale Regional Partnerships

Berkshire Hathaway GUARD Insurance Companies - Chris Harvey

Underwriter

Loadsure - Chris Taylor

Director

Alvarez & Marsal - Cody Parsons

Executive Vice President

Amwins - Colleen Finn

Chief Marketing Officer, Home

Plymouth Rock Assurance - Cory McGinnis

Senior Vice President/Producer/Broker

USG Insurance Services - Dana Useldinger

Broker Production Manager

ARU - David Carey

Director

Alvarez & Marsal - Dawn Holland

Senior Account Manager

Lockton - Devon Williams

Senior Marketing Director

AmeriLife Marketing Group - Doug Blythe

Associate Managing Director

The American Equity Underwriters - Ed Mauceri

Senior E&S Property Underwriter

Swiss Re - Elen Sullivan

Underwriter II, Fine Art and Specie

AXA XL - Elizabeth Haggerty

Associate Account Executive

Alliant Insurance Services - Evan Legassey

Assistant Vice President – Brokerage Casualty

XS Brokers - Gabriel Palacios

Owner and Founder

GD Insurance Group - Georgia Schelberger

Vice President and Associate Managing Director

Towne Insurance - Grace Carlson

Assistant Vice President

CRC Group - Graham Topol

Co-Founder and Co-Chief Executive Officer

MGT Insurance - Irene Koelewijn

Vice President, Risk Placement

Christensen Group Insurance - Jack Mullally

Assistant Vice President/Underwriter

Swiss Re - James Kellard

Commercial Insurance Agent

Single Source Insurance - Jennifer Keefe

Vice President, Property

Amwins Re - Jillian Walsh

Production Underwriting Supervisor – Environmental Division

Great American Insurance Group - Kayla Russo

Environmental Underwriter

Crum & Forster - Madison Hulbert

Assistant Vice President and Account Executive

Lockton - Madison Kness

Client Executive, Commercial Lines

Wye River Insurance - Mark Jones Jr.

President and Chief Operating Officer

Goosehead Insurance - Megan Bell

Senior Vice President, Marketing

Falvey Insurance Group - Michelle Dimitri

Partner – Facultative Reinsurance

McGill and Partners - Nicole Alfaro

Communications Manager

Admiral Insurance Group (a Berkley Company) - Nicole Sivieri

Senior Vice President, Insurance Capital Solutions

bolt - Nicole Tirella

Senior Manager – Complex Risk

HUB International - Parker James

Senior Account Executive – Captive and Key Accounts

Higginbotham - Paula Trinchera

Vice President – Underwriting, D&F Property

Canopius - Rachael Najarian

Vice President and Senior Broker – Umbrella/Excess Casualty

Aon - Ravi Patel

Executive Vice President and Head of Property Practice

Risksmith - Samantha Manfredini Look

Senior Vice President, Employment Practices Liability

Aon - Sara Husty, CPCU, ARM, AU-M

Lead Underwriter

Berkshire Hathaway GUARD Insurance Companies - Shantelle Cabir

Senior Vice President and Business Insurance Broker

Newfront - Sharina Hicks

Senior Sales Representative

The Hartford - Shelby Vail

Marketing Director

AmeriLife - Steven Sanchez

Vice President and Associate Directo – Middle Market, and Renewable Energy Leader

Lockton - Stevi Siber-Sanderowitz

Senior Counsel and Vice President, Insurance/Litigation Analytics

SterlingRisk - Summer Graziano

Senior Vice President – Hull and Liability Sales Leader

Aon - Tamila Garayo

Assistant Vice President and Private Client Services Manager

Personal Risk Management Solutions - Tanner Hackett

Chief Executive Officer

Counterpart - Taylor Dennis

Senior Manager, Process and Customer Excellence

Openly - Taylor Jones

Director, Business Development

Swingle Collins & Associates - Tori Sarmiento

Senior Sales Executive

INSTANDA - Trent Owens

Broker

CRC Group - Ty Travis

Commercial Insurance Broker

The Partners Group - William Steenbergen

Co-Founder and Chief Technology Officer

Federato

Insights

-

Brett Carter

Brett Carter

Vice President and Managing Director

The Jacobson Group -

Mindy Pranculeviciute

Mindy Pranculeviciute

Senior Recruiter, Accounting and Finance

Talentfoot

Frequently asked questions

Who are the best insurance professionals under 40 in the USA in 2026?

The best insurance professionals under 40 in the USA in 2026 are the winners of Insurance Business America’s 12th annual Rising Stars list – an annual recognition program identifying the most exceptional young insurance talent across the country. The 2026 list spans every major sector of the US insurance industry, from commercial and specialty brokerage to employee benefits consulting, excess and surplus lines underwriting, reinsurance, claims operations, insurtech, and risk management. Winners are selected by an independent panel of senior industry leaders. IBA also recognizes the top 100 insurance professionals in America through the annual IBA Hot 100.

What is a Rising Star in the US insurance industry?

A Rising Star in the US insurance industry is a professional aged 40 or under who has demonstrated exceptional achievement, leadership, and commitment to a career in insurance. Recognized by IBA’s annual Rising Stars program, these are individuals who combine genuine technical depth with leadership potential, measurable business impact, and a commitment to developing the professionals around them. The 2026 Rising Stars class was assessed on current role, key achievements, career goals, and contributions to shaping the industry.

How does IBA select the best young insurance professionals?

Starting in January 2026, IBA invited insurance professionals across the United States to nominate their most exceptional young talent for the 12th annual Rising Stars list. Nominees had to be aged 40 or under as of July 1, 2026, and committed to a career in insurance with a clear passion for the industry. The final list was determined by an independent panel of five industry leaders: Chase Marable of Higginbotham, Kelly Geary of EPIC Insurance Brokers & Consultants, Miranda Fischer of Alliant Insurance Services, Rebekah Ratliff of the National African American Insurance Association, and Samantha Manfredini Look of Aon.

What qualities define the best insurance professionals under 40?

The best insurance professionals under 40 combine technical expertise with a deliberate investment in the human dimension of their work. According to Mindy Pranculeviciute, senior recruiter at Talentfoot, the top three patterns are: owning outcomes rather than tasks, having commercial intuition that connects daily work to revenue and loss ratio, and investing in others early through mentorship and team development. The 2026 Rising Stars list also shows a consistent emphasis on empathy as a competitive differentiator, with multiple featured winners independently naming it as their strongest professional attribute.

How is AI affecting the careers of young insurance professionals in the USA?

AI is already embedded across the US insurance industry – in underwriting, claims processing, distribution, and analytics. According to Conning’s 2025 C-suite survey, 55 percent of US insurance executives are at early or full adoption stages for generative AI, and the insurance workforce is expected to be reshaped by 2035 to prioritize relationship skills and technological literacy. The 2026 Rising Stars use AI for efficiency – processing lengthy submissions, automating back-office tasks – while guarding their human competitive advantage: empathy, judgment, and the contextual knowledge that no model can replicate.

What is the insurance talent shortage, and how does it create opportunity for professionals under 40?

The US insurance industry is projected to lose approximately 400,000 workers through attrition by 2026, with 50 percent of the current workforce expected to retire by 2028, according to US Bureau of Labor Statistics projections cited by MarshBerry in March 2025. This has compressed career timelines significantly: talent specialists now report placing professionals into VP-level roles at year 7 or 8, compared to the historical 12–15 years. However, experts caution that the talent shortage creates opportunity, not automatic advancement – the professionals benefiting most are those who combine technical expertise with leadership and interpersonal skills.

Why does mentorship matter for insurance professionals under 40?

Mentorship is one of the clearest signals of leadership readiness in the insurance industry. The professionals on the 2026 Rising Stars list are notable not only for their individual achievements but also for their investment in developing others – running internship programs, coaching junior colleagues, founding professional networks, and building team cultures that outlast their direct involvement. According to Mindy Pranculeviciute of Talentfoot, young professionals who mentor and lift their teams signal leadership readiness years before they hold a formal leadership title: “Nobody rises alone, and decision-makers spot the ones who make everyone around them better.”

What sectors do the best young insurance professionals in the USA work in?

The 2026 Rising Stars list spans every major sector of the US insurance industry. The 2026 class includes professionals from commercial and specialty brokerage, excess and surplus lines underwriting, employee benefits consulting, reinsurance, claims operations, insurtech, marketing and communications, and risk management. The list features professionals from independent agencies, global carriers, wholesale brokers, managing general agencies (MGAs), and technology-driven insurtech companies – reflecting the extraordinary breadth of career paths the US insurance industry offers. The list also includes professionals from firms recognized among the top retail insurance brokers in the USA.

Methodology

Starting in January, Insurance Business America invited insurance professionals across the country to nominate their most exceptional young talent for the 12th annual Rising Stars list.

Nominees had to be aged 40 or under (as of July 1, 2026) and be committed to a career in insurance with a clear passion for the industry. Nominees were asked about their current role, key achievements, and career goals, as well as their contributions to shaping the industry.

Recommendations from managers and senior industry professionals were also taken into account. The Rising Stars were determined by an independent panel of industry leaders composed of:

The Rising Stars report is proudly supported by the Association of Professional Insurance Women.

Keep up with the latest news and events

Join our mailing list, it’s free!