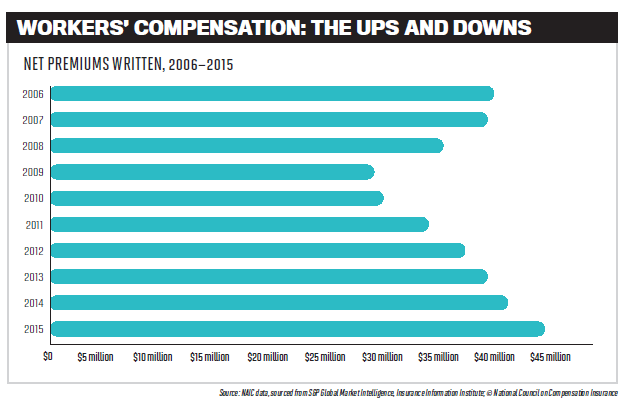

AS THE US economy has recovered from the global financial crisis, so too has the country’s workers’ compensation insurance sector. After experiencing a significant drop-off in the second half of the last decade, workers’ comp premiums have been rising steadily since 2011. The labor market has bounced back, corporate earnings are strong, and insurers have been able to raise rates. As a result, workers’ comp is now the largest commercial line written by US property & casualty insurers, contributing 10% of the P&C industry’s direct written premiums.

In a recent research report, Moody’s revealed that underwriting profitability in workers’ compensation has improved due to

prior year rate increases, a stable cost trend and strong revenue growth. The report did predict, however, that increased competition and rate pressure could drive margin compression in the next two years, along with other challenges.

“Many insurers have been looking for ways to improve the risk profile of their workers’ compensation book by reducing exposures in higher-hazard occupational classes or unprofitable accounts,” Moody’s vice president Siddhartha Ghosh said. “Longer-term public health trends – the increasing prevalence of diabetes, obesity and abuse of prescription drugs – could result in higher medical inflation, creating reserving challenges for the sector.”

Whereas these standard-market claims are generally uncomplicated in nature, the excess side of workers’ compensation deals with the complex and difficult-to-manage files, or what Stephen Peacock, assistant vice president of claims at Safety National, describes as “the top 5% of the worst claims that happen.”

“Being a specialist workers’ comp carrier, we often deal with claims related to shootings of police officers and injuries to other first responders,” Peacock says. “The biggest complexity of dealing with police claims is the medical side. There is often organ, spine or head damage, and the patient can end up being on life support and in the hospital for weeks or months. They may then need rehab for a long time and have to be placed in an assisted living facility or receive professional home nursing care for the rest of their life.”

The American Society of Addiction Medicine [ASAM] estimates that of the 21.5 million Americans 12 years and older who have a substance abuse problem, almost 2 million are addicted to prescription opioids. Statistics show that 94% of those who have opioid abuse problems switch to heroin because prescription opioids were “far more expensive and harder to obtain,” according to the ASAM.

The amount of injured workers becoming addicted to prescription opioids is on the rise, and although workers comp’ claims account for just a small percentage of the overall healthcare market, the impacts are far-reaching. Under workers’ compensation laws, physicians don’t have to follow Medicare rules and recommendations on opioid dosages and are able to prescribe as much as they see fit.

As a patient becomes more tolerant of opioid medications, doctors are prescribing higher dosages or changing the medication in order to keep the pain under control, which ends up pushing up the cost,” Peacock says. “In addition, people tend to become more dependent on the medication. So, if you try to reduce the dosage, the patient often ends up trying to supplement their medication with illicit drugs, which are less expensive.”

Based on its analysis of nearly 300,000 claims, the fi rm found that organizations with a formal post-injury engagement process enjoyed a reduction of more than 14.16% in average total costs compared to those who did not, reducing costs by an average of more than $1,550 per claim.

The same analysis found that companies that had a claim liaison or someone in a similar role also showed reductions in average total costs of 12.56%, which translates to savings of approximately $1,350 per claim.

As an excess workers’ comp carrier, playing an active role in patient recovery and making sure injured workers get the best possible care is something Midlands Management Corporation takes very seriously.

“It’s also about ensuring that the nurses, caseworkers and physicians employed by the carrier make sure the patient is embracing the treatment and doing everything they can to get better,” says Midlands president and CEO Charles C. Caldwell. “Sometimes patients can be lackadaisical about making appointments and following up on their own care. The caseworkers and nurses make sure those appointments are being kept and, in some cases, actually make the appointment for the injured worker.”

Despite the positives associated with implementing a post-injury engagement plan, the Gallagher Bassett study found that only a third of organizations are currently following an engagement strategy. “A portion of the remaining respondents seem to believe informal/voluntary engagement occurs, but cannot confirm that it does,” the report said. “Risk and claims managers wondering if they should formalize engagement processes and roles as part of their claims management strategy should definitely consider doing so.”

In October, the owner of a New Jerseybased electronic recycling warehouse was sentenced to three years in prison for orchestrating an insurance scam that cost an insurance company nearly $600,000 by lying about the kind of work his employees did in order to get cheaper rates on his workers’ compensation insurance.

Although a case like that is difficult to detect, Caldwell does believe brokers and agents have an important role to play in reducing workers’ comp fraud.

“Brokers and agents have to be vigilant and look out for red flags,” he says. “It may be that someone has a suspiciously high number of claims or that a certain medical facility has a lot of workers’ comp patients. Brokers and agents should definitely report anything they notice that seems unusual.”