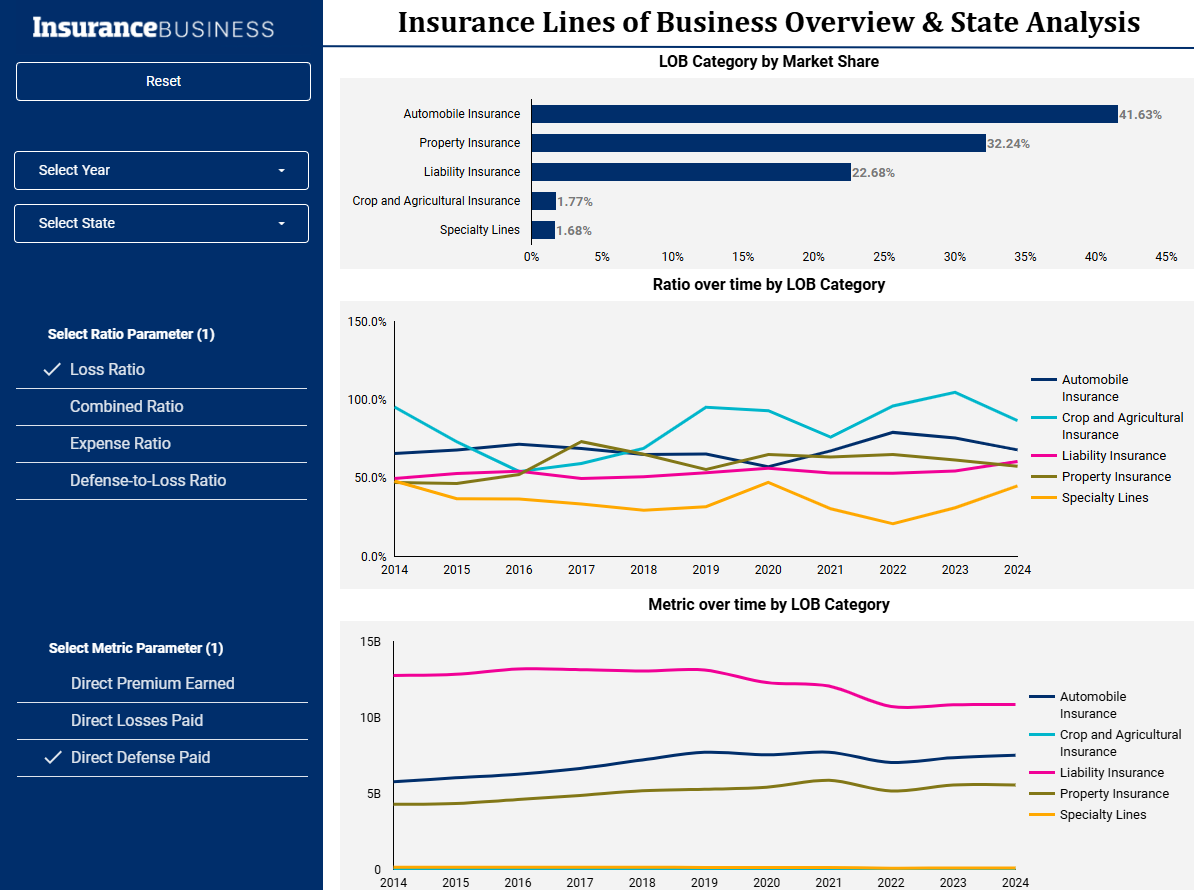

Automobile insurance continues to dominate the US property and casualty insurance market, after 10 years of holding the highest market share across all lines of business.

In 2024, this market share sat at 41.6%, peaking at 43.4% in 2018. This was followed by property insurance at 35.7% and liability insurance at 19.5%. Crop and agricultural insurance and specialty lines only held 1.8% and 1.7%, respectively.

Most notably, total private passenger auto insurance has the largest amount of direct premiums written reported as of March 3, 2025, at $344 billion, which is about 35% of all written premiums.

Automobile insurance commands the US insurance market due to its legal necessity, scale of vehicle ownership, high claim volume, regular renewals, and strategic bundling potential. It’s often the most visible and well-marketed line of insurance, with a consistent, built-in demand from virtually every adult household.

While this has served it well in recent years, the auto insurance market is forecast to take a hit from President Donald Trump’s latest tariff announcements, with many fearing a surge in premiums. Auto imports do not appear to be one of the tariffs that Trump put a pause on last week.

This data is part of a new Insurance Business+ dashboard: Property and Casualty Line of Business Performance and Market Trends.

Visit the IB+ Data Hub to access a innovative insurance analytics dashboard, with data sortable by year, state, line of business, and more!

Automobile insurance had the highest premium earned and highest market share, as well as the highest direct losses paid.

Furthermore, private passenger auto no-fault coverage (personal injury protection) represents just 4% of the market, while the commercial equivalent barely registers at 0.3%.

These figures likely reflect the narrow application of no-fault laws, which are active in only a handful of US states. Moreover, legislative shifts in jurisdictions like Michigan – which overhauled its no-fault rules in 2020 – have reshaped demand and reduced carrier exposure in this area.

Businesses anticipate the newly imposed tariffs, which include a 25% tax on all cars and car parts imported into the US, may significantly increase repair or replacement costs and therefore the amount of money insurers are required to pay out in the event of a claim. Insurance companies will likely pass this burden onto consumers in the form of higher premiums.

Rate comparison site Insurify forecasts that the full weight of the tariffs could push yearly auto insurance costs higher on a single vehicle, reaching as much as $2,750 from around $2,300.

For insurers, this breakdown provides more than just a snapshot of market composition; it’s a call to sharpen strategic focus. With liability lines anchoring the market, competition on pricing, underwriting discipline, and claims efficiency will remain fierce. At the same time, emerging risks – such as advanced driver-assistance systems, autonomous vehicles, and evolving fraud schemes – are adding new layers of complexity.

Brokers, too, will need to adapt their strategies in response to these evolving market conditions. The data suggests there may be untapped growth in commercial lines, particularly as businesses scale up fleets and look for bespoke coverage. Conversely, shrinking demand in no-fault jurisdictions calls for careful client education and a potential pivot in service offerings.

A full breakdown of the property and casualty lines of business can be found in the Property and Casualty Line of Business Performance and Market Trends dashboard.