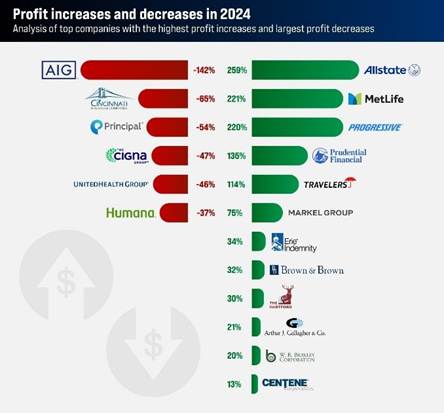

The Allstate Corporation saw the greatest profit increase in the US for the first three quarters of 2024, boasting a 259% increase in profits, a new Insurance Business+ report finds.

This turnaround was largely attributed to enhanced claims management, which allowed Allstate to reduce claims payouts and optimize operational costs.

One of the key drivers was a substantial 11.6% increase in property-liability earned premium. This growth was supported by ongoing premium rate hikes and high customer retention in the auto and homeowners’ insurance markets. These pricing adjustments played a crucial role in offsetting the impact of elevated claims costs and a rise in catastrophe-related losses.

Allstate’s auto insurance division emerged as a standout contributor, generating $486 million in underwriting income for the quarter. The segment’s performance was buoyed by strategic rate increases and disciplined cost control, although the overall number of policies in force saw a slight decline.

Allstate’s impressive gains were followed by a 221% profit increase for MetLife and a 220% profit increase for Progressive.

This data is part of a comprehensive Insurance Business+ report that analyzes the US insurance market’s conditions in the first three quarters of 2024. This analysis breaks down the companies with the highest profit increases and decreases during this period, highlighting reasons for successes and shortcomings.

The results reflect a broader trend: 2024 was a strong year for property and casualty (P&C) insurers. The sector posted a 12% year-over-year increase in net premiums earned, thanks to rate hikes and solid underwriting discipline.

Investment income jumped 18% in Q3, as higher interest rates delivered stronger yields across fixed-income portfolios. Moreover, the industry’s average combined ratio improved to 85.6%, signaling better profitability overall.

Drawing a sharp contrast with the likes of Allstate and MetLife, American International Group (AIG) faced several challenges during the year that forced its profits down 142%.

The insurer’s decision to spin off its life and retirement business, Corebridge Financial, led to a $1.4 billion net loss for the full year, down from $3.6 billion net income in 2023, compounding $325 million of catastrophe-related charges, primarily from hurricanes Milton and Helene.

This ultimately hampered underwriting profitability through the addition of 5.5 points to the fourth quarter’s 92.5 combined ratio for general insurance, up from 89.1% in the same quarter a year before. AIG’s underwriting income hit $454 million in the fourth quarter, down 29% from $642 million the year before.

AIG’s loss during the year was followed by similar, albeit lesser, profit declines for The Cincinnati Insurance Company, Principal, Cigna, UnitedHealth, and Humana.

The latest batch of tariffs unveiled by President Donald Trump earlier this month is also forecast to further strain insurers operating in several key lines of business, particularly auto and homeowners’ insurance.

A recent Insurance Business+ report explained that rising material costs from the newly introduced 25% duty on cars and car parts will likely increase claims costs for auto insurers, which may subsequently elect to adjust actuarial models, prompting rate hikes between six and 10% by the end of 2025.

A budding trade war following the tariffs may also prompt a wider economic downturn that could reduce the overall risk pool, further negatively affecting underwriting.

Similar trends are also expected in the homeowners’ and commercial property insurance businesses, with tariffs on construction materials such as steel, aluminum, and lumber anticipated to raise the cost of home repairs and premiums by association.

For brokers, the 2024 performance snapshot underscores the importance of aligning with insurers that are navigating market headwinds effectively – particularly those prioritizing underwriting discipline, investment strategy, and digital innovation.

Firms like Allstate, Progressive, MetLife, and Travelers are proving that tight cost control, strategic rate adjustments, and smart risk management can deliver significant returns even in challenging environments.

Meanwhile, the profit struggles of large health insurers highlight the risks associated with escalating care costs and regulatory uncertainty – though these companies remain key players in the growing Medicare and Medicaid space.

Brokers who adapt alongside top-performing carriers will be best positioned to deliver value to clients and capitalize on growth opportunities – whether in auto, property, cyber, or life and retirement sectors.

A full in-depth analysis can be found in the Top Insurers by Market Cap report. This analysis offers an early look at market conditions ahead of our full report, which will include Q4 data and an expanded view of the top 85 US insurers by market cap.