California topped the charts in 2024, earning the highest direct premium in the US property and casualty insurance market with $94 billion.

This was followed by Florida with $71 billion and Texas with $59 billion, according to new Insurance Business+ data.

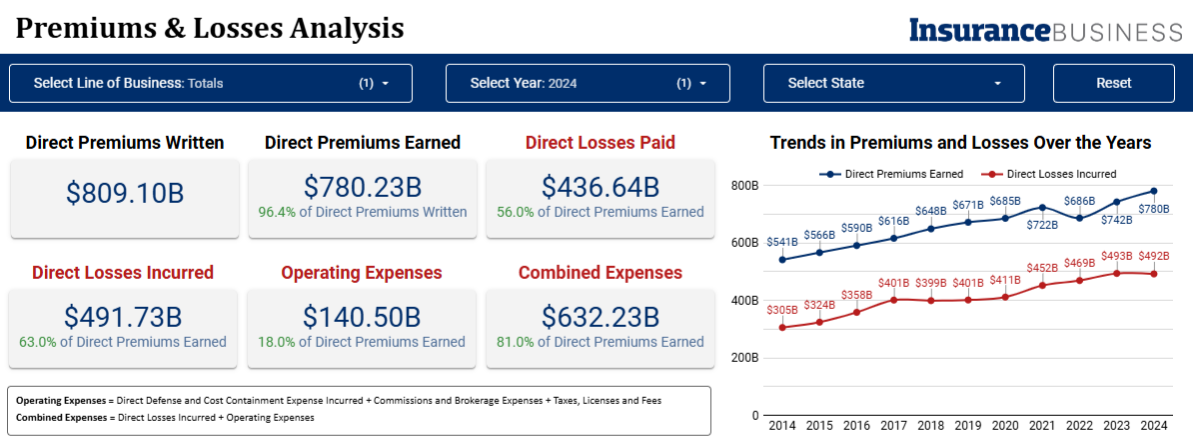

Direct premiums earned for the entire property and casualty industry totaled $780 billion in 2024, up from $742 billion in 2023. This has increased steadily since 2014, with the exception of a dip in 2022, which rebounded in 2023.

In 2022, the industry grappled with elevated claims severities driven by inflation. Notably, used car inflation resulted in approximately $15 billion in additional claims costs, particularly affecting personal auto insurance. This surge in claims costs pressured underwriting profitability and constrained premium growth, according to Swiss Re.

Direct losses incurred constituted 63% of direct premiums earned at $492 billion.

Interested in more insurance data? Subscribe to the IB+ Data Hub and unlock cutting-edge data in our powerful, interactive dashboard.

Despite leading the nation in premium volume, California’s insurance market remains under significant pressure.

Following the catastrophic wildfires in January 2025 – now considered the most expensive wildfire event in US history – insurers have been navigating a perfect storm of high exposure, regulatory restrictions, and rising reinsurance costs. More than 16,000 structures were destroyed across some of Southern California’s most affluent communities, according to the California Department of Forestry and Fire Protection.

A Morningstar DBRS report highlighted that reinsurance costs, which have remained elevated since 2023, are further complicating the outlook for insurers operating in the state.

As reinsurance attachment points have increased, primary insurers are retaining more risk, amplifying their exposure to natural catastrophes. In some cases, carriers are also contending with additional expenses such as reinstatement premiums, depending on the structure of their reinsurance programs.

These growing costs have already prompted several major insurers to halt new policy issuance in high-risk areas. In response to the mounting crisis, California implemented regulatory reforms in December 2024, allowing insurers to pass along reinsurance costs to policyholders for the first time.

Morningstar DBRS described the reform as a “step in the right direction” but warned that transferring reinsurance costs to consumers could worsen affordability issues – potentially prompting pushback from advocacy groups and triggering additional regulatory scrutiny.

State Farm holds the largest market share at 12.81% – more than double the share held by Progressive – ranked second – at 6.18%.

Most of State Farm’s direct premiums earned come from California, totaling $9.9 billion, while Progressive earns the largest share of its premiums from Florida, at $10.4 billion.

Most of State Farm’s direct premiums earned come from California, totaling $9.9 billion, while Progressive earns the largest share of its premiums from Florida, at $10.4 billion.

State Farm is traditionally strong in personal auto and homeowners’ insurance, both of which are in high demand in California. The company has built long-term brand loyalty there and holds one of the largest market shares in the state.

Progressive has focused more heavily on auto insurance and high-risk drivers, making Florida’s unique risk environment (higher accident and fraud rates, dense urban areas) a key growth area. It has become one of the leading insurers for non-standard auto coverage in the state.

A full insight into premiums and losses within the property and casualty sector can be found in the Property and Casualty Financial Insights dashboard.