Independent insurance agency owner Scott Leavitt has encountered a few small group clients surprised to discover that in some cases, sending their employees to the controversial HealthCare.gov exchange site yielded greater affordability than continuing to offer coverage themselves.

“Some groups ask, ‘Am I hurting my employees by offering benefits?’” said Leavitt, who runs Scott Leavitt Insurance in Boise, Idaho. “In one situation, an employee discovered she could insure her family of four for less than she could insure herself through her employer. This saves money for the company and gives workers better benefits for a cheaper price.”

It’s not the message that Leavitt, who does much of his business in the small group market, wants to give. However, a new report from PricewaterhouseCoopers (PwC) reveals that it may be a recurring one.

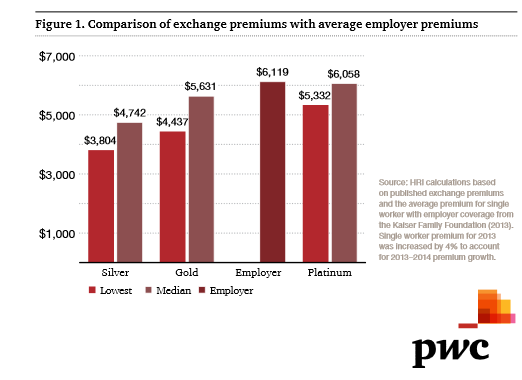

According to PwC, the national average premium for workers this year is $6,119 compared with a median cost for a similar platinum exchange plan of $5,844 and a gold plan of $4,885. Considering that employer-provided coverage pays for roughly 85% of medical costs, gold and platinum plans (which offer 80% and 90% coverage, respectively) are comparable.

That’s a premium 8% lower than standard employer coverage under the platinum plan, PwC noted, and the reason that so many small businesses are finding they’re better off sending employees to the exchanges this year than struggling to continue offering their own health coverage.

“It does suggest that the Public Exchange Individual Premiums are, in the aggregate, competitive or potentially lower than the average cost of comparable health coverage for employers nationally,” Michael Thompson, a principal in PwC’s Human Resource Services practice, told

Insurance Business.

However, the study does not suggest all employers would be better off abandoning their own offerings. Thompson noted that the average premiums in the study generally reflect those of larger employers, while Leavitt suggested that individual premiums are going to “go through the roof” in 2015, perhaps making employer-offered coverage more competitive with what’s on the individual exchange market.

Furthermore, as San Francisco Bay area agency owner Colleen Callahan points out, employees of small businesses choosing to drop health insurance benefits may face unfriendly tax implications.

“What we try to remind [clients considering dropping coverage] or point out to them is that there are tax implications,” Callahan said. “The employee can at least deduct their contribution through payroll right now with their employer and depending on how the employer handles it, it could be added to the employee’s taxable income if the employer subsidizes the new premium.”

That isn’t a great reflection on companies still striving to attract quality and loyal employees through health benefit—a trend Callahan has seen among her clients.

“I think more of the employers want to continue to offer health insurance as a group coverage, particularly family businesses who want to keep it from a personal standpoint,” she said.