When KPMG presented the results on the Canadian insurance industry’s look back at 2013, it read like a horror story. This time around, the smiles have returned.

“When we conducted the survey last year, 2013 was a bad year,” says Paul Cleveland, vice president of insurance advisory services with KPMG. “What with all of the natural catastrophes in the P&C industry, Ontario was subjected to the 15 per cent rate reduction in auto, and Bill 15 was nowhere near being passed to put a check on fraud.”

.jpg)

Add to that the Office of the Superintendent of Financial Institutions was mandating Own Risk Solvency Assessments be produced, “so companies were trying to figure that one out,” says Cleveland.

“And the accounting standards were changing in IFRS4, valuing the policy liabilities using interest rates, and interest rates were very low,” says Cleveland. “So companies were being forced by these new standards to use low interest rates over the 20, 30 and 40 years, which had some severe implications from a profitability perspective.”

But at last week’s conference, those frowns were turned upside down.

The second annual Canadian Insurance Industry Risks & Opportunities Survey, which has just wrapped up, provided a much brighter outlook on how those in the industry saw themselves. This time around, KPMG asked what insurance professionals see as the biggest risks and opportunities in the industry; and what stage their organization is currently to either mitigate the risks or capitalize on the opportunities.

KPMG is looking to see if there has been a shift in trends and insights into the key issues the insurance world is experiencing, Cleveland told

Insurance Business, and examined the preliminary findings of some 160 plus respondents at the company’s 23rd annual insurance conference recently. (continued.)

#pb#

“This year was a much different year,” says Cleveland. “We didn’t have all the natural catastrophes. Although we did have a long winter, which affected the first six months of 2014, we didn’t have those catastrophes like in 2013. The insurers had done their first ORSAs, so people got through that; and IFRS4 implementation was actually deferred for a year to 2019. And as far as the interest rate issue – the IFRS proposals were relaxed, so the life insurers didn’t have to use current low interest rates to value the liability for the long term in force policies – they could actually use the rates that they believe most appropriate over that period of time.

“So going into this year, a lot of that uncertainty and risk that had been there before had gone.”

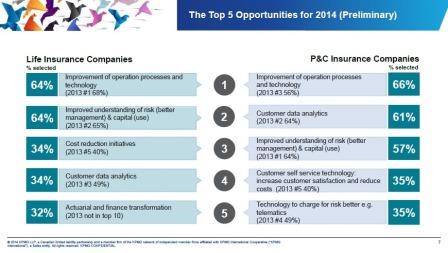

Breaking down the demographics of the results from the survey, 50 per cent were insurance executives or board members.

“This is a really good number,” says Cleveland, “as they are people who would have a broad view of risk.”

Breaking it down by product, about 50 per cent of respondents were from the P&C sector, with about a third identifying themselves as selling life.

“The balance were reinsurers, brokers, banks and related industries,” says Cleveland. “This wasn’t a finance and actuarial perspective we were getting – which when you think KPMG, you might think that is what you’re getting – but in actual fact, we were getting a broad perspective, particularly with 50 per cent being executives and board members (in insurance).”

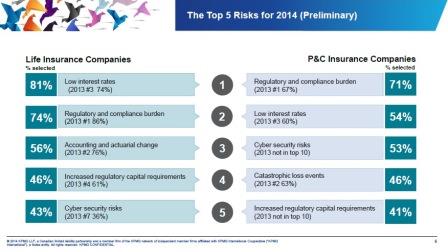

In 2013, 86 per cent placed regulatory and compliance burden on the life side, as their biggest risk.

“People this year didn’t feel as strongly as last year on those two concerns,” says Cleveland. “This year it was low interest rates, with 81 per cent identifying that as their biggest concern – up from 74 per cent in 2013.”

The full results will be compiled in the coming weeks, and will be made available in the new year, says Cleveland.