There is a number that should be pinned to the wall of every insurance executive's office: 60.

That is the percentage of insurance customers, according to Accenture research, who would switch providers for more personalised service. Not for a lower premium. Not after a claims dispute. Simply because another carrier offered to treat them as an individual rather than a policy number.

For an industry that has historically competed on price, brand recognition, and distribution reach, this figure represents a tectonic shift. The battleground for customer loyalty has moved — and a significant portion of the market has not yet noticed.

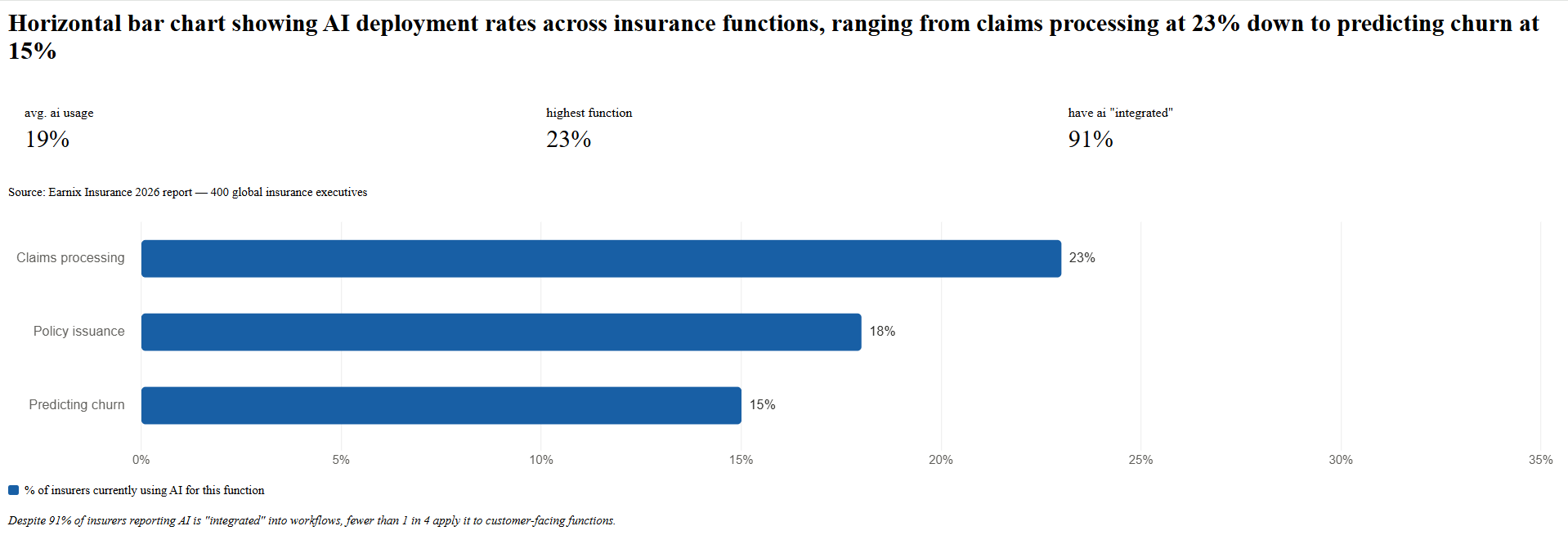

The Earnix Insurance 2026: The Race to Reinvent report, which surveyed 400 global insurance executives, captures the scale of the industry's challenge with uncomfortable precision. While usage-based and personalised policies are gaining traction, only roughly one in four insurers say they can deliver personalisation at scale today. That means approximately 75 per cent of the industry is asking customers to accept a generic experience in a market where 60 per cent of those customers are willing to leave for something better.

This is not primarily a technology gap. Modern personalisation platforms, AI-driven recommendation engines, and integrated data architectures exist and are commercially available. The gap is strategic: too many carriers have not yet treated personalisation as a core growth lever, positioning it instead as an enhancement to be bolted on after more pressing digital transformation priorities.

That sequencing is backward. As Insurance Business reported in its deep-dive on AI-powered personalisation at scale, the goal of leading insurers globally is now to deliver "highly individualised experiences at every touchpoint, whether digital or human-assisted, using real-time data and AI." IAG's executive general manager of digital business described the ambition as creating a "connected experience where different touchpoints in previous stages are providing context for the current conversation." That is not a future aspiration; it is an operating model already in deployment among early movers.

The word "personalisation" risks becoming a marketing abstraction unless grounded in what it means operationally for a policyholder.

At a minimum, it means that when a customer calls about their home insurance, the agent — or the AI-assisted interface — already knows they recently renewed their auto policy, have a teenage driver, and live in a postcode that experienced severe weather last spring. It means coverage recommendations that reflect their actual life stage, not a demographic cohort. It means renewal notices that include relevant product suggestions based on documented life changes, not generic upsell scripts.

At its most sophisticated, it means dynamic pricing that adjusts in real time based on actual behaviour — the telematics-informed auto premium, the IoT-connected property policy that rewards the household with a functioning smart smoke detector, the health cover that responds to verified wellness activity.

A Simon-Kucher analysis notes that the usage-based insurance market alone is projected to grow from $43 billion in 2023 to over $70 billion by 2030. But personalisation extends well beyond pricing mechanics. As the same analysis observes, tools that identify visitor intent, surface relevant products, and create custom digital experiences in real time represent the fuller picture of what the market's leading edge looks like.

The honest obstacle to all of this is data — its quality, its completeness, and what carriers are permitted to do with it.

The Earnix survey is direct on this point: 83 per cent of insurance executives are concerned that their AI models are being trained on inaccurate or incomplete data. Two-thirds report that poor data quality actively slows decision-making and limits AI effectiveness. And nearly 40 per cent cite data security and privacy settings as the most significant challenge affecting their AI adoption initiatives.

These are not abstract concerns. Personalisation built on bad data produces the opposite of its intended effect — miscalibrated offers, inappropriate product recommendations, and the unsettling sense, for the customer, that the carrier does not actually know them at all.

The industry's response is a significant increase in third-party data investment. Eighty-three per cent of insurers surveyed by Earnix plan to increase investment in third-party datasets over the next three years — up six percentage points from 2023. Telematics, IoT, and behavioural data are among the fastest-growing sources. The challenge, as Insurance Business has noted in its coverage of digital customer experience transformation, is that enriching data while maintaining compliance and trust requires a level of governance architecture that many carriers are still constructing.

The business case for getting personalisation right extends well beyond customer satisfaction scores.

Accenture research cited in the Earnix report indicates that digital leaders in insurance can reduce operational costs by up to 30 per cent while improving satisfaction — a rare combination of top-line and bottom-line benefit. Carriers that deploy AI to proactively identify at-risk policyholders, present relevant retention offers at precisely the right moment, and resolve friction points before they escalate into cancellations are not just improving experience. They are fundamentally restructuring their customer economics.

The Pega Institute's research on personalisation in insurance is instructive here: proactive, AI-driven retention strategies represent a shift from "reactive save attempts to proactive relationship management." The calculus changes entirely when a carrier prevents a lapse rather than scrambles to reverse one.

For younger, digitally native customers — the cohort that will define premium volume over the next two decades — this is not a differentiator. It is, as the Earnix report describes, a baseline expectation. Gen Z customers, growing up with hyper-personalised experiences across every commercial interaction, are especially likely to view carriers as commoditised when offerings feel generic. The churn risk from this segment is not latent; it is structural.

Personalisation does not operate in a governance vacuum. Insurance executives surveyed by Earnix rank data security and privacy regulations as the compliance factor most likely to reshape strategy over the next two years — above AI regulation, ESG requirements, and solvency standards.

This is the unavoidable tension at the heart of insurance personalisation. The more granular and behavioural the data, the more powerful the personalisation — and the more complex the regulatory and ethical environment. Regional variation amplifies the challenge: the EU's AI Act and GDPR impose strict limits on automated decisioning and data use, while US carriers navigate a patchwork of state-by-state privacy laws alongside evolving federal requirements.

Carriers that treat this tension as a reason to delay personalisation investment are misreading the trade-off. Those that embed privacy governance into their personalisation architecture from the outset — rather than layering it on retrospectively — will be able to move faster, with greater certainty, than those who treat compliance as someone else's problem.

As Insurance Business reported in its coverage of how the industry is approaching bionic agent models, the firms gaining ground are those that give their people the right data and tools at the right time — not those automating indiscriminately. The personalisation goal is not to replace human judgement, but to inform and augment it.

The 60 per cent switching statistic is not a warning about a future possibility. It is a description of a present reality, operating quietly beneath the surface of retention numbers that may not yet reflect the underlying customer sentiment.

The customers who have not switched have not done so because they are satisfied. Many have not switched because the friction of switching — comparing policies, transferring documents, waiting for new coverage to activate — has historically been high enough to absorb a moderate level of dissatisfaction. That friction is eroding, fast, as comparison platforms improve and digital onboarding becomes instantaneous.

When switching becomes as easy as cancelling a streaming service, the reservoir of inertia that has buffered many carriers from the consequences of their personalisation gap will drain away. The insurers who have built genuine individual relationships with their policyholders — who know them, anticipate their needs, and deliver value between renewal cycles — will retain them. Those who have not will find themselves competing, with insufficient differentiation, in a race to the bottom on price.

The time to build that relationship is not after customers start leaving. It is now.

This article draws on the Earnix Insurance 2026: The Race to Reinvent report, based on a survey of 400 global insurance executives conducted by Market Strategy Group in late 2025. Additional data sourced from Accenture, Pega Institute, Simon-Kucher & Partners, and Insurity's 2025 Digital Experience Index.