5-Star Construction

Jump to winners | Jump to methodology

Covering the companies that build America

Construction insurance keeps America building throughout a wide variety of economic cycles and societal changes. Recently, the construction industry has been affected by everything from the COVID-19 pandemic to supply chain issues and inflation, while growing significantly at the same time. To determine which insurers were the best at meeting the needs of construction companies during this difficult period, IBA surveyed brokers on construction insurers’ work quality, specialist expertise, and client service, ultimately rewarding high-scoring companies in 14 different categories.

“Inflation has caused the cost of materials to skyrocket throughout the construction industry”

Christian Colangelo, Hull & Company

A mix of market conditions

IBA talks to representatives of four winners of its 5-Star Construction Awards 2022, who reflect on the past few years and share their thoughts on what’s ahead for the industry.

Christian Colangelo is a casualty broker at award-winner

Hull & Company. Considering the construction industry in general, he says: “While demand is still high, I feel the construction industry has grown accustomed to the ‘new normal’ over the past six to 12 months, and [companies] are beginning to increase salaries in order to maintain their existing workforces. I see this trend continuing with the overall demand starting to slow down throughout the remainder of 2022, as there is uncertainty around inflation and the economy as a whole.”

Looking at construction insurance in particular, Brad Tennant, founder and president of award-winner Tennant Special Risk, characterises the sector in four ways. To start with, he says the pandemic has led to supply chain issues, a lack of new housing inventory, and interest rate movements. Secondly, there’s been a shift in the minds of insureds, their clients, and additional insureds towards making the primary general liability policy more of a warranty contract. As a result, the area between warranty and true indemnity resulting from negligence has been irreparably blurred, he says.

Thirdly, additional insured tenders have caused problems and will drive expenses for years to come. Construction contracts are being written with no negligence coverage triggers on behalf of the named insured, with what many believe is the goal to recreate the ‘11/85’ additional insured coverage environment, Tennant says. And finally, the availability of capital coming into the insurance marketplace is leading to new construction risk underwriting facilities and greater competition, and often results in downward pressure on rates.

“Rising construction costs, materials costs, additional insured tenders with exploding expense reserves, nuclear social inflation settlements, and decreasing rates/premiums will lead to [an] industry reckoning,” says Tennant.

Risk Placement Services adds that coverage and pricing vary from state to state. Residential construction is getting more and more difficult, and there are more underwriting guidelines, stricter policy terms, more exclusions and more limitations. This is due to the increased cost of litigation, and of construction products and materials needed for building.

Meanwhile, Sean Dewalt, a senior loss control consultant at award-winner Umialik Insurance in Anchorage, Alaska, says his company is using local knowledge and expertise to hedge against uncertainty, respond to large-scale events, and maintain the best employees and management to keep up with expected growth rates.

“Rising construction costs, materials costs, additional insured tenders with exploding expense reserves, nuclear social inflation settlements, and decreasing rates/premiums will lead to [an] industry reckoning”

Brad Tennant, Tennant Special Risk

COVID, supply chain issues, inflation

Undoubtedly, the one event that’s had a huge impact over the past couple of years on both the construction and construction insurance industries has been the COVID-19 pandemic, which has caused secondary issues such as supply chain problems, and these, in turn, have contributed to inflation.

“COVID-19 did slow the growth of construction in Alaska since 2020,” says Dewalt. “That stated, most contractors worked through the entire pandemic without missing a beat.

“The construction industry lost out on a reported $50 million in canceled contracts and another $50 million in deferred spending during COVID-19. Those companies also spent millions of dollars responding to the new COVID-19 policies and procedures, [as well as on] logistics, quarantine requirements, and travel costs, including chartering aircraft. All this was on top of low oil prices in 2020. In a state where 90% of the state revenues come from that global commodity, that reduces funding for capital projects that affect contractors statewide.”

Colangelo, on the other hand, says COVID-19 created a demand for construction, while also causing issues within the industry. “It has led to scheduling constraints and oftentimes lengthy delays in projects,” he says. “In some states, contractors were not allowed to continue work, and owners faced tough challenges in figuring out how they were going to stay in business.”

Affecting working conditions and policies, COVID-19 has also led to supply chain problems. In the trucking industry, Tennant attributes the problems to fewer drivers due to trucking companies reducing salaries and benefits.

Meanwhile, in isolated Alaska, supply chain issues are nothing new. “Because of the vast distance between Alaska and the lower 48 states, understanding the cost of materials delivery, lead times, and availability of products and workarounds is crucial to these companies working in the Last Frontier,” says Dewalt.

“Creative solutions include bulk purchases for fuel and other essential commodities, negotiated purchases for construction materials in advance of bid letting as a hedge on future prices, and vendor negotiations and good relationships that can make or break contract performance if things go awry. Companies will ultimately fail if supply chain management is not well understood, or if critical paths are not dynamic.”

Colangelo says supply chain issues and inflation have been a one-two punch that’s been tough for contractors. “Not only are their supplies more expensive, but sometimes they are not even available, and they are forced to find substitutes,” he says. “Some worry this may lead to an increase in construction defect claims in the future due to contractors working with materials they are not familiar with.

“Inflation has caused the cost of materials to skyrocket throughout the construction industry,” he adds. “This leads to higher overall sales for the contractor, even though the amount of work may have stayed the same. The increased sales then lead to increased premiums, which has led to some tough conversations at renewal if the retailer and client have not been properly prepared.

“We have been able to negotiate with carriers in order to break out contractors’ supplies and materials from their total sales. We are then able to get the carrier to provide a lower rate on these goods, rather than charging the same rate for all their sales. This has helped mitigate the artificial inflation in sales due to the increased cost of goods.”

“The construction industry lost out on a reported $50 million in canceled contracts and another $50 million in deferred spending during COVID-19”

Sean Dewalt, Umialik Insurance

Excelling in specialized areas

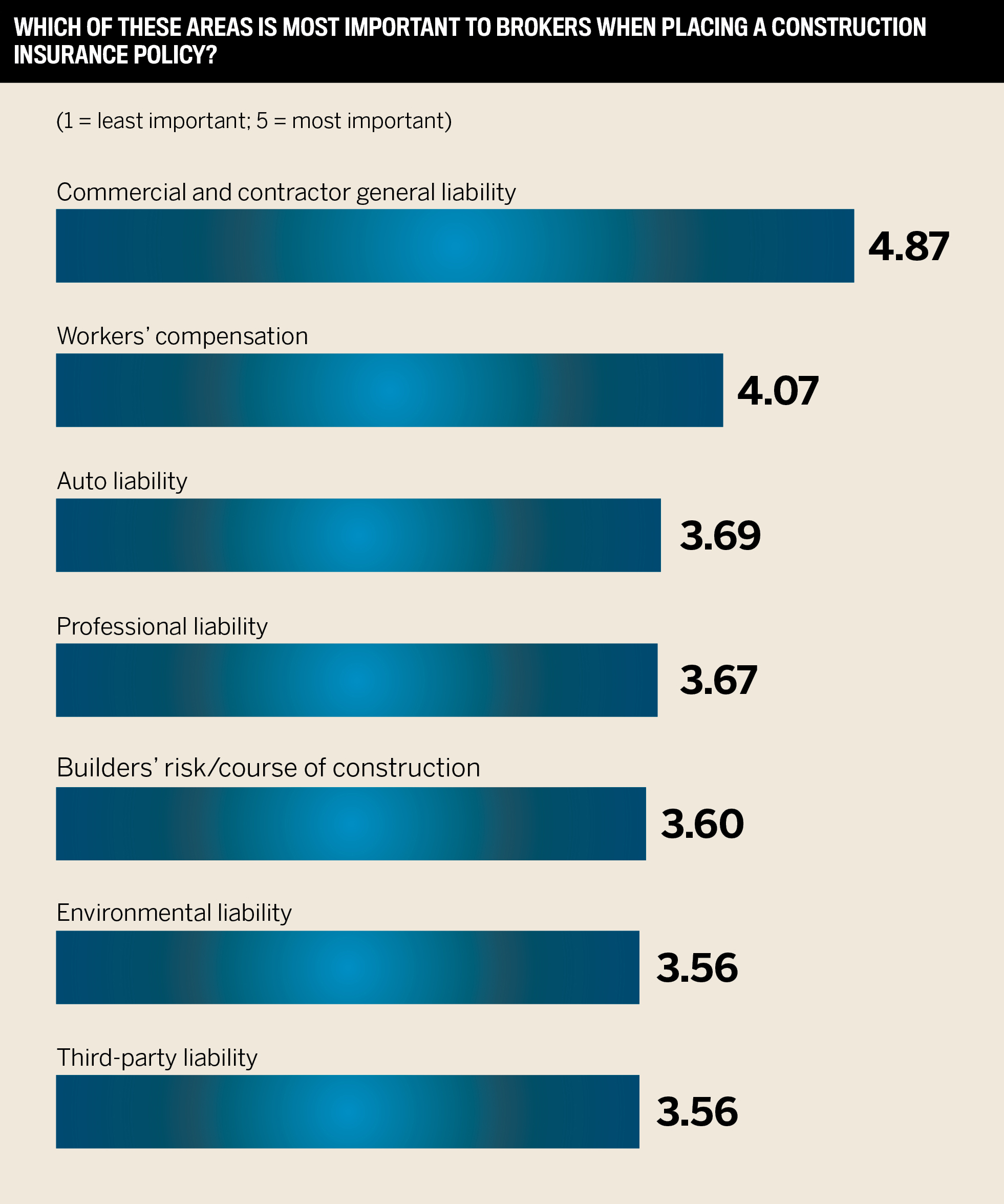

This year’s 5-Star Construction award winners were judged in the categories of builders' risk/cause of construction; commercial and contractor general liability; workers’ compensation; environmental liability; third-party liability; auto liability; professional liability; civil contractors; general contractors; specialty/subcontractors; professional construction service firms; developers and owners; heavy construction; and demolition.

In the general contractors category, winner Umialik says what differentiated its offering was its underwriting philosophy, which Dewalt describes as "out of the box".

“If the underwriting and loss control team can wrap their heads around the risk, then it will likely be written,” he says. “While other insurers are moving into a black box style or large data assessment style, Umialik continues to work with local agents to personally underwrite each policy. This allows for a greater opportunity to build relationships, which in turn fosters long-term, positive effects that local Alaskan companies appreciate.”

Tennant Special Risk, a winner in the category of specialty/subcontractors, differentiates itself from the competition with its policy forms and endorsements.

“Tennant Special Risk has been complimented by our wholesalers, claims partners, and coverage attorneys regarding the clarity and unambiguous nature of our contractors’ specialty endorsements,” says Tennant.

“Many years ago, Tennant Special Risk removed the deductible on virtually all policies. That, coupled with broad-blanket additional insured forms needed to satisfy [our] subcontractual obligations, helped set us apart [from our competitors]. Our consistent approach to underwriting our subcontractor risks also helped. Historically, we have not changed our risk acceptability criteria, leading to a more consistent underwriting discipline that translates into effective broker communications.”

Hull & Company won awards in the civil contractors, professional liability, third-party liability, environmental liability, and commercial and contractor general liability categories. However, Colangelo considers the last of these to be the company’s ‘bread and butter’.

“Not only do we have the experience of working these deals on a daily basis, but we also have a strong relationship with [our] carrier partners that’s necessary to turn around competitive and comprehensive terms for our clients,” he says. “With the increase in demand for contractors has also come an increase in submissions for carriers. This has caused turnaround time to be extended, which is why it’s so important for us to leverage our strong relationships in order to continue to provide tailored terms in a timely fashion.”

Meanwhile, Risk Placement Services won in nearly all categories and notably in the area of environmental liability. Companies are concentrating on sustainability and reducing their carbon footprint, according to Risk Placement Services, and have started using materials such as cross laminated timber (CLT) instead of concrete and steel. As CLT is a new material, there’s no loss history, and the rigidity of the material is yet to be determined. Clients are also deploying other techniques such as modular construction and 3D printed technologies.

5-Star Construction

Builders’ risk/course of construction

- Great American Insurance

- Liberty Mutual Insurance

- Risk Placement Services

- RT Specialty

- SIS Insurance

- US Assure

- Zurich Insurance USA

Commercial and contractor general liability

- Hull & Company

- Scottish American

- SIS Insurance

- Tapco Underwriters

- Umialik Insurance

Workers’ compensation

- Appalachian Underwriters

- Builders Mutual

- Markel Specialty

- RT Specialty

- SIS Insurance

- State Compensation Insurance Fund

- Travelers USA

Environmental liability

- Berkley

- Evanston

- Hull & Company

- Risk Placement Services

- Scottish American

- SIS Insurance

Third-party liability

- Hull & Company

- Risk Placement Services

- Scottish American

- SIS Insurance

- Travelers USA

Auto liability

- Auto-Owners Insurance

- Berkshire Hathaway

- Everest Insurance

- Farmers Insurance

- Guard Insurance

- Infinity Insurance

- Liberty Mutual Insurance

- Nationwide

- Progressive Insurance

- Risk Placement Services

- SIS Insurance

Professional liability

- Hiscox USA

- Hull & Company

- Risk Placement Services

- SIS Insurance

- Tokio Marine HCC

Civil contractors

- Hiscox USA

- Hull & Company

- Risk Placement Services

- RT Specialty

- SIS Insurance

General contractors

- Hull & Company

- Navigators, a brand of The Hartford

- SIS Insurance

- Tapco Underwriters

- Travelers USA

- Umialik

Specialty subcontractors

- CNA USA

- Hull & Company

- Liberty Mutual Insurance

- SIS Insurance

- Tapco

- Tennant Special Risk LLC

- Tokio Marine HCC

Professional construction service firms

- CNA USA

- Hiscox USA

- Hull & Company

- Liberty Mutual Insurance

- Risk Placement Services

- SIS Insurance

Developers and owners

- Hull & Company

- Liberty Mutual Insurance

- Risk Placement Services

- SIS Insurance

Heavy construction

- Admiral Insurance Group

- Hull & Company

- Navigators, a brand of The Hartford

- Risk Placement Services

- SIS Insurance

- Travelers USA

Demolition

- Berkley

- Hull & Company

- Risk Placement Services

- SIS Insurance

Methodology

To select the best construction insurance providers for 2022, Insurance Business America sourced feedback from insurance brokers. IBA’s research team began by conducting a survey of a wide range of brokerages to determine what brokers value in a construction insurer. The team also spoke to hundreds of brokers across the country, asking them to rate the construction insurers they had worked with over the past 12 months.

The in-depth information gathered enabled the research team to assign weighted values to each of the criteria being rated by brokers. At the end of the research period, the insurance providers that received the highest rankings in terms of work quality, specialist expertise, and client service were named 5-Star Award winners in construction insurance.

Keep up with the latest news and events

Join our mailing list, it’s free!