Advice that many industry experts give motorists who are searching for cheap car insurance is to never assume that one company is the low-price leader for everyone. Because each driver’s profile and circumstances are different, an auto insurer that offers the cheapest policy for one person may be the most expensive option for another. And often, the best way for motorists to ensure that they are getting the lowest rates possible is to shop around and compare quotes.

Learn how to compare quotes for car insurance here.

This is what the media outlet U.S. News did in its latest study. To help drivers find out which auto insurers offer the least expensive policies, the firm compared premium prices in all 50 states using a range of parameters, including age, gender, driving history, credit score, and vehicle make and model. The results are revealed below.

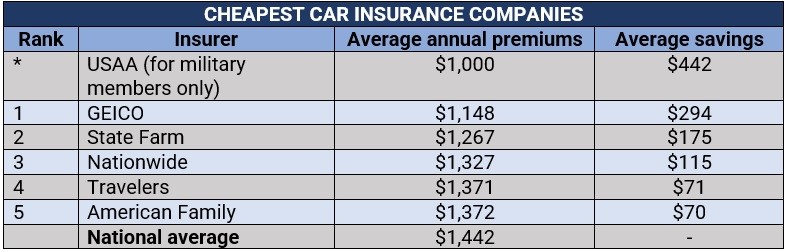

The average annual auto insurance premium across the country is $1,442, according to U.S. News’ analysis. Anything at that price point or below can be considered cheap car insurance. USAA offers the cheapest rate among all major car insurance providers at $1,000, almost a third lower than the national average. It also provides the least expensive premiums in almost every category. The insurer, however, has a restricted customer base, offering coverage only to active and former members of the US military and their families.

Among conventional insurers, GEICO has the cheapest car premiums, averaging $1,148 yearly. It is also the most affordable option for teens, seniors, safe drivers, and those with a poor credit history.

State Farm, meanwhile, ranks third on the list, with annual rates at $1,267. The country’s largest car insurer is also the cheapest choice for motorists with traffic violations, outside of USAA.

Here are the top five insurers offering the cheapest car insurance premiums based on U.S. News’ study.

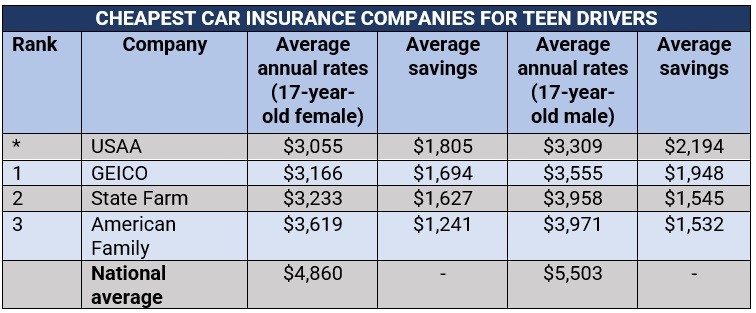

Cheap car insurance for teens

Car insurance premiums are higher for teen drivers than for any other age group. There is no way around it. Due to their inexperience, young drivers are more frequently involved in accidents than their adult counterparts. This puts them in a higher risk category, driving up their rates.

A 17-year-old female driver pays about $4,860 in car premiums annually, while males of the same age shell out $5,503. The figures are about three to four times higher than those for the average driver. Excluding USAA, the top three car insurers with the cheapest rates for teens, regardless of gender, are GEICO, State Farm, and American Family.

Find out how to find cheap car insurance for young drivers in this article.

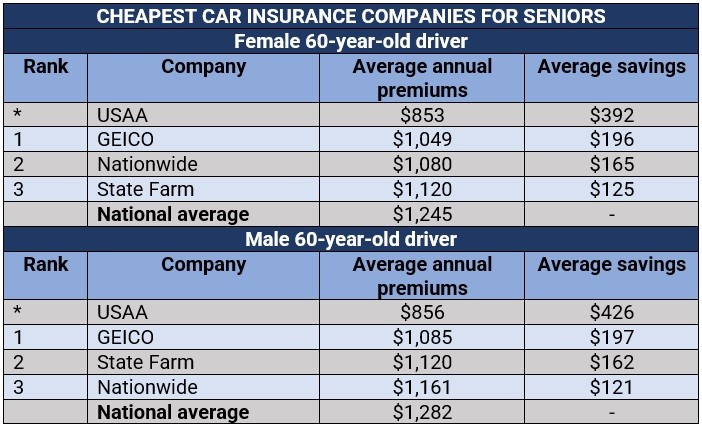

Cheap car insurance for seniors

Cheap car insurance for seniors

Senior drivers, or those in their 60s, are charged the lowest rates among all age groups, at $1,245 and $1,282 for females and males, respectively. Although the study did not reveal the reason for the cheap car insurance, it is widely known that many older people drive less and are, therefore, not likely to be involved in accidents. These are the insurers that offer the lowest rates for seniors.

Cheap car insurance for minimum coverage

Almost all states require drivers to have a bodily injury (BI) and property damage (PD) liability coverage, with the exception of Florida, where only PD is mandatory. Here are the cheapest auto insurance companies for minimum coverage based on the study.

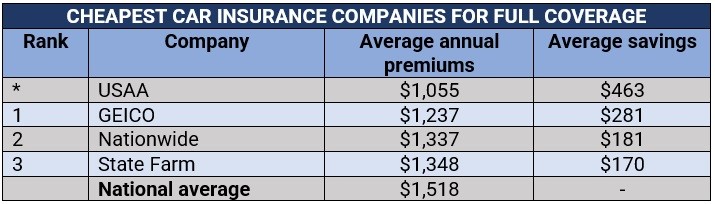

A full coverage car insurance policy combines liability (BI and PD), collision, and comprehensive coverage. Premiums for this type of coverage are typically higher as it provides more protection. These are the companies that offer drivers the most savings.

Cheap car insurance for drivers with poor credit

Insurance companies primarily use credit-based insurance scores to determine whether a motorist is eligible for coverage and how much premiums they will be charged. But according to many industry insiders, auto insurance scores also help prevent drivers with good credit standings from bearing some of the costs of higher-risk individuals.

These are the insurers that provide the cheapest rates for drivers with poor credit.

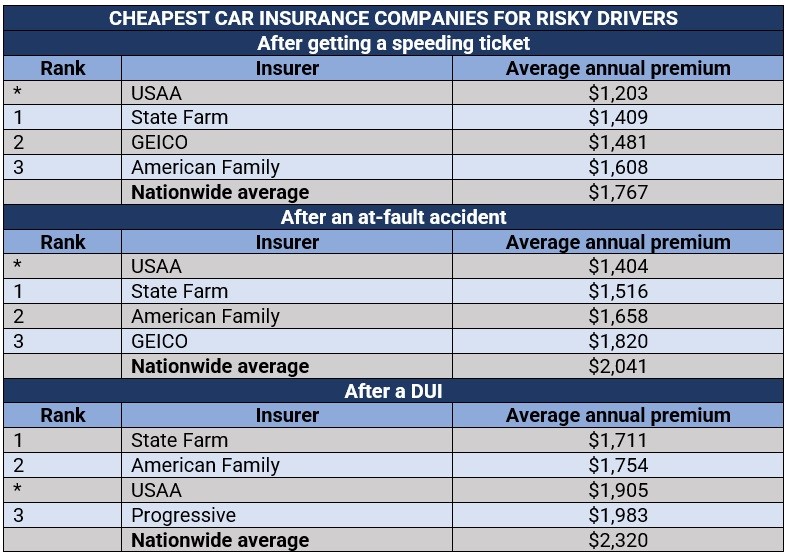

Car insurers tend to view high-risk drivers as less of an asset and more of a liability, which is the main reason why premiums for this demographic are often significantly higher. it has been shown that a speeding ticket can raise insurance costs by more than 22%, an at-fault accident by almost 42%, and about 61% after a DUI.

For those who have experienced these traffic incidents, these are the insurers that offer the best rates.

Each driver comes with a unique set of risks. To calculate how much a motorist should pay in car premiums, insurers look at a range of factors, including those already mentioned above. However, different auto insurance providers use different metrics in determining how much risk a driver poses to them. Here are some common factors auto insurers take into consideration when determining insurance rates, according to Triple-I.

Regardless of the factors listed above, drivers can employ an array of practical strategies to reduce auto insurance costs. Here are some of them:

Car insurance providers offer a range of discounts, which motorists can take advantage of to reduce their annual premiums. Drivers can often avail of these through:

Auto insurance companies offer several coverage options that impact how much premiums will cost. To slash rates, experts advise motors to ditch unnecessary coverages.

Keeping one’s driving record spotless is among the best ways motorists can access affordable car insurance rates. Safe driver discounts vary between insurance providers but usually, motorists can access between 10% and 25% reduction in premiums for adopting safe driving practices.

A higher deductible means motorists will pay lower premiums. However, this also increases the amount they need to pay before their auto insurance picks the tab, so policyholders should make sure to keep the value at a level that they can afford. Sometimes cheap car insurance can lead to expensive one-off costs.

Some cars are more expensive to insure than others. For motorists looking to save on car insurance costs, experts recommend checking out sedans, vans, and other family-friendly vehicles as these often have the lowest premiums.

Enrolling in a usage-based insurance (UBI) program is beneficial for drivers who log fewer than 10,000 miles every year. This is often done with the insurer installing a telematics device in the vehicle. This device, also called a black box, tracks driving behavior, allowing motorists to access discounts based on when, how well, and how much they drive.

Using mass transit reduces how much a person drives their vehicle, which may also have an impact on premium prices. Many car insurance providers charge based on your average yearly commuting, using public transportation more can help you get cheaper car insurance but talk to your provider about this.

Car insurance rates change often so that companies can stay competitive and get new customers. Because of this, it would be beneficial for motorists to review their policies every time it renews, so they can get the best coverage that fits their current needs at the cheapest price.

To operate a vehicle, motorists must carry auto insurance. It is mandated by the law in almost all states, except New Hampshire. Getting caught driving without one can result in hefty fines and affect future eligibility for obtaining coverage.

However, depending on where they live, drivers are required to secure different types of coverages. Here are the most common types of policies motorists need to take out, according to Triple-I.

You can check out the leading car insurance companies in the US in our special reports where we look at the best in insurance.

Which insurers do you think are the best options for affordable premiums? Do you have other rate-reduction tips to get cheap car insurance that you want to share? Share away in the comment box below.