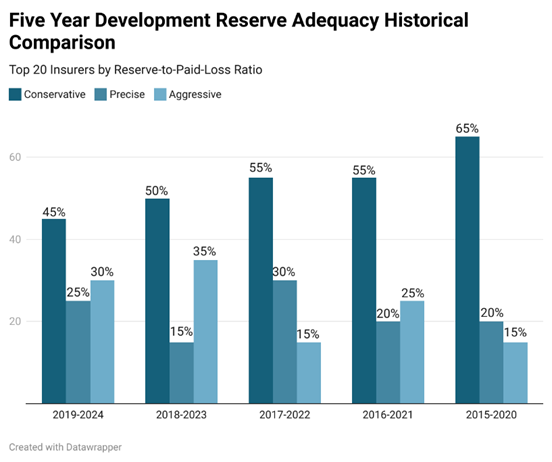

A new analysis of insurer reserve behaviors across the United States reveals a striking trend: 45% of the top 20 insurers by reserve-to-paid-loss ratio took a conservative approach to reserving, while 30% took an aggressive approach. The remaining 25% achieved actuarial precision.

Note: Based on Annual Statement Year 2024

The insight comes from the newly launched Property and Casualty Loss Development and Reserve Analysis Insights Dashboard, which evaluates the year-over-year development of incurred versus paid losses for more than 700 insurance groups. Using a heat-mapped grid and drill-down tables, the tool flags carriers based on how their reserves align with actual paid claims — classifying them as conservative, precise, or aggressive.

With a five-year development period starting in 2019, only 25% of the top 20 insurers by reserve-to-paid-loss ratio fell into the actuarial precision zone (with a ratio between 0.9 and 1.5), signaling well-calibrated assumptions and data-driven reserving.

While this remains the smallest category, it represents a notable increase from just 15% during the 2018–2023 development period. This rise has been accompanied by corresponding decreases in both conservative and aggressive reserving practices.

The shift is likely driven by several factors, including evolving regulatory and accounting standards such as IFRS 17 and NAIC requirements. These standards discourage excessive conservatism — which can distort a company’s financial position — and penalize under-reserving, which poses risks to solvency.

Advancements in data analytics, predictive modeling, and machine learning are also enabling insurers to access vast amounts of real-time claims data. These tools reduce uncertainty and allow actuaries to set reserves with greater accuracy, limiting the need for conservative buffers.

It’s worth noting that overly conservative reserving remains common among reinsurers and specialty carriers in long-tail lines, where greater reserve cushions are needed due to claim latency and volatility. These buffers reflect a more cautious stance on inflation and litigation risk.

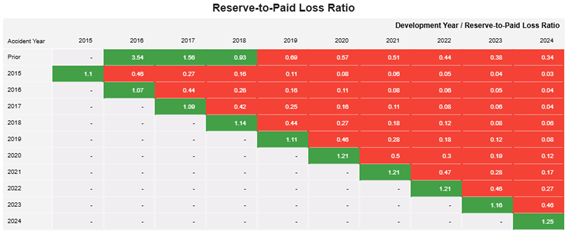

In recent development years — particularly from 2020 to 2024 — the reserve-to-paid-loss ratio has trended sharply downward for most insurers. This ratio, which compares carried reserves to cumulative paid losses, helps assess reserve sufficiency by showing how much reserve remains for every dollar already paid in claims. While a ratio below 0.9 isn’t necessarily problematic in isolation, a widespread and sustained decline may indicate that many companies are under-reserving — potentially to boost near-term financial results or due to overly optimistic assumptions about claim development.

The dashboard’s Loss Development Summary tab reveals that incurred losses mostly declined from a given accident year through the 2024 development year. For instance, incurred net losses from the 2020 accident year had decreased by 3.3% by 2024, while paid losses increased 90.4% over the same period.

One potential factor behind this trend is the timing of claims development. Incurred losses include both paid claims and adjustments to reserves for reported and unreported claims. If incurred losses are stabilizing, it could suggest most claims have already been reported and fully developed — reducing the need for additional reserves. Meanwhile, paid losses continue to rise as insurers pay out previously reported claims. This timing effect is particularly noticeable in long-tail lines like general liability or workers’ compensation, where claim resolution can span several years.

Other factors may include:

With litigation costs rising, inflation remaining stubborn, and social inflation pushing claim sizes higher, industry analysts warn that today’s under-reserving could lead to painful reserve strengthening tomorrow.

In an era where capital efficiency is paramount, some insurers may be tempted to release reserves too quickly. But regulatory pressure, scrutiny from rating agencies, and the demands of M&A due diligence mean reserve adequacy remains a critical indicator of an insurer’s financial health.

The dashboard’s drilldown capabilities allow brokers, reinsurers, and analysts to:

Ultimately, the industry is signaling optimism. Whether that optimism is warranted — or reckless — will depend on how claim development unfolds in the years ahead.

For a complete breakdown of loss development, reserve composition, and reserve adequacy benchmarking, visit the IB+ Property and Casualty Loss Development and Reserve Analysis Insights Dashboard.