California’s largest homeowners’ insurer, State Farm, has petitioned state regulators for an urgent 22% rate hike, a move that underscores the deepening instability in the state’s insurance market. The request, submitted on Monday, reflects growing financial pressures as wildfires and other natural disasters continue to drive insurance costs upward.

Over the past few years, an increasing number of Californians have struggled to obtain or maintain affordable insurance. Many major providers have withdrawn from the market or sharply increased rates, citing rising risks. The latest wave of fires in Los Angeles, which left 12,000 homes in ruins, has only exacerbated concerns for both insurers and policyholders weighing whether to rebuild.

State Farm has already paid over $1 billion in claims related to the latest Los Angeles fires and expects further payouts, making this disaster one of the most expensive in its history. The company, which insures over a million homes in California, has warned that continued risk exposure requires significant rate adjustments to ensure financial stability.

“Insurance will cost more for customers in California going forward because the risk is greater in California,” the company stated, justifying the need for higher premiums. “We must appropriately match price to risk. That is foundational to how insurance works.”

The California Department of Insurance confirmed that it would review State Farm’s application. “State Farm General’s rate filings raise serious questions about its financial condition,” said department spokesman Gabriel Sanchez. “To protect millions of California consumers and the integrity of our residential property insurance market, the department will respond with urgency and transparency.”

State Farm’s move comes as California’s insurance sector faces an unprecedented crisis. Last year, the company opted not to renew 30,000 homeowners’ policies, adding to the uncertainty for residents. It had already ceased issuing new policies in the state in 2023.

In response to mounting pressure, California Insurance Commissioner Ricardo Lara introduced a strategy aimed at compelling insurers to provide more coverage in high-risk fire zones. This plan presents insurers with three options: maintaining an 85% policy-writing rate in high-risk regions, achieving a 5% growth in coverage, or transferring policies out of the state’s last-resort FAIR Plan.

Governor Gavin Newsom has backed the initiative, calling it a necessary measure to modernize California’s outdated insurance system. “As the climate crisis has rapidly intensified, the insurance system hasn’t been seriously reformed in 30 years – this is part of our strategy to strengthen our marketplace and get folks the coverage they need,” Newsom said.

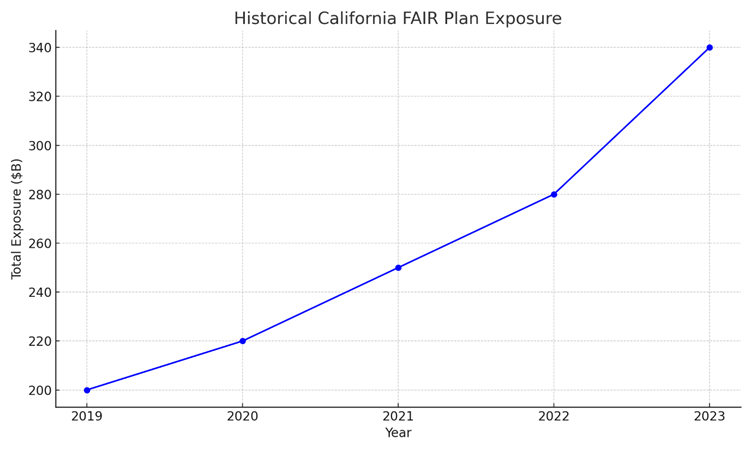

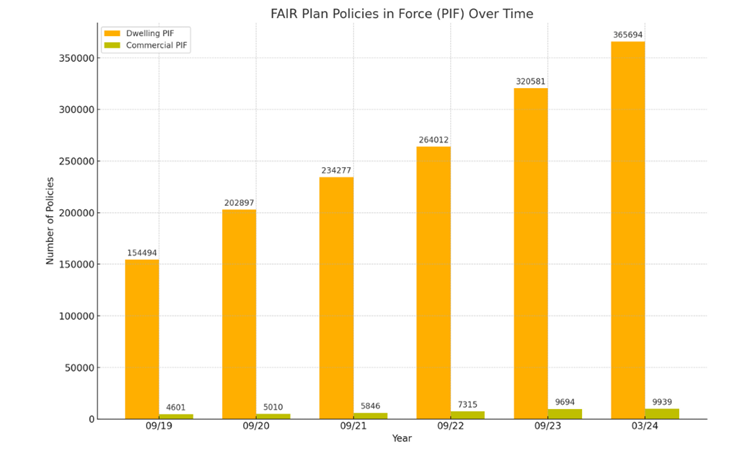

The state’s FAIR Plan, originally created in 1968 as a safety net for homeowners unable to obtain insurance elsewhere, has seen an explosion in demand. Its total, coverage exposure now stands at $340 billion, a 20% increase from the previous year.

With more insurers reducing their market presence or demanding steep rate increases, many Californians have been left with few choices. The FAIR Plan, however, is viewed by critics as a fragile system that could buckle under the weight of its growing obligations.

Consumer advocacy groups have raised concerns about State Farm’s repeated rate hikes, accusing the company of using California’s crisis to extract greater profits. “We think they’re taking advantage of the tragedy to try and squeeze Californians,” said Carmen Balber, executive director of Consumer Watchdog. She pointed out that the company had already increased rates by 20% earlier in 2024 and questioned the necessity of another mid-year hike.

As California grapples with a worsening insurance dilemma, both regulators and insurers face mounting pressure to find a sustainable solution. Whether Lara’s plan can stabilize the market remains to be seen, but, for now, homeowners must brace for further uncertainty in an already volatile landscape.