The latest IB Industry Report, the State Farm Carrier and Market Review, analyzes how the company’s public perception and litigation exposure have evolved in parallel with industry-leading expansion, revealing a pattern that carries direct implications for underwriting, regulation, and market posture.

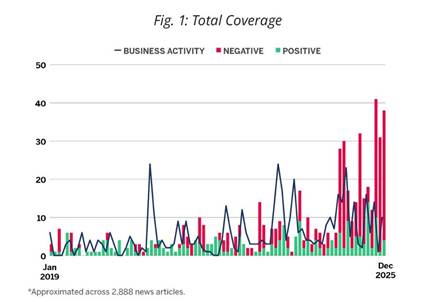

State Farm’s positive narratives, driven by hiring, innovation, and catastrophe response, continue to define the company’s brand. But they are now matched, and in some periods exceeded, by negative attention tied to litigation, claims disputes, and regulatory intervention.

State Farm’s recent litigation and regulatory exposure is closely tied to the scale and concentration of its catastrophe footprint. In Los Angeles County alone, the insurer covers roughly 250,000 homes and 880,000 vehicles, a concentration that translated into more than 12,000 wildfire claims during the January 2025 events. By mid-year, the company had paid over $4 billion related to those fires, with projected losses reaching $7.6 billion before reinsurance. This triggered a multi-layer regulatory response, including a proposed 22% rate increase, a mandated $500 million capital injection, and a formal market conduct investigation into claim-handling practices. Beyond California, litigation has expanded across multiple jurisdictions such as Texas and Illinois, including class action threats over policy language, federal lawsuits alleging systematic underpayment of claims, and ongoing disputes tied to catastrophe subrogation.

The 2025 California wildfire episode is presented as a case study in how these pressures converge: capital adequacy, claims governance, and regulatory negotiation unfolding simultaneously under public scrutiny.

Crucially, the report moves beyond headlines to aggregate litigation history, SERFF regulatory filings, and sentiment data to identify recurring patterns: where disputes arise, how they evolve, and how they intersect with the company’s broader strategy.

For insurance professionals, this matters in tangible ways:

Reputational risk is increasingly a driver of financial and operational outcomes.

Supported by six chapters, 29 figures, and a full data appendix, the report provides a structured framework to understand how perception and litigation shape one of the industry’s most prominent carriers.

Access the full State Farm Carrier and Market Review to see the complete risk landscape across sentiment, litigation, and regulation, and make more informed decisions in a market where scrutiny is becoming as important as scale.

Get the complete report here.