5-Star Carriers 2021

Jump to winners | Jump to methodology | View PDF

THE CARRIERS THAT ARE CARRYING ON

In insurance, priority on a carrier’s ability to pay claims and maintain a long-term relationship with the broker and the client. But unexpected events like those that have defined the past year – from the COVID-19 pandemic to civil unrest and climate chaos – can put even the best arrangements under strain.

“Clients are fatigued with 12 to 14 consecutive quarters of pricing increases almost across the board,” says Brian Wanat, chief broking officer at Aon. “That, coupled with the virtual COVID-19 environment, has made for a very challenging last year or so.”

Mike Rice, CEO of CAC Specialty, concurs, noting that the market has been in correction territory for more than two years, typified by rising premiums, coverage re-evaluations and reductions in limit deployment.

“For us, that means we need to differentiate the client’s risk into the marketplace and convince the carriers that client’s risk is worth taking,” he says. “For our clients, we have to ensure they are getting the best coverage. All of this means you must be prepared.”

Maintaining service during times of stress

A range of issues – COVID-19, civil unrest, wildfires, named storms, social inflation, litigation funding, runaway jury verdicts, #MeToo and ransomware – has led to a recent spike in claims volume. But despite that increase, Wanat believes carrier service levels have improved markedly over the past 12 months.

“The efficiency of the business and the ability to access the key decision-makers has been a benefit of the virtual environment,” he says. “I think we were able to operate effectively using the goodwill and the strength of some longstanding relationships that we and our customers had built up over years and years of face-to-face meetings. While we should certainly learn and take advantage of some of the learned efficiencies, I do think it will be important to get back to face-to-face. I also think that improving technology will continue to be an item of consideration for everyone.”

Both Wanat and Rice were impressed with the support they received from carriers throughout the pandemic, but they’re also both keenly aware that the current environment presents plenty of opportunities for a carrier to lose a broker’s business.

“The primary reason most recently has been the carriers themselves deciding to exit or retract from certain businesses, products or industries,” Wanat says. “Whether it’s the difficulty of turning an underwriting profit in a 0% interest rate environment or the inflationary claims aspect, many carriers have posted combined ratios north of 100%, some for years. Losing money for a long period of time isn’t a long-term business strategy, and some carriers just didn’t have the stomach to ride through market cycles; others didn’t have the critical mass or talent. The reasons vary, but I would say that most clients appreciate longstanding carrier relationships. Retention rates tend to be very high.”

According to Rice, “an inability to come to an agreement on depth of coverage and price of premiums are leading factors in altering or destroying a relationship with us. The combination of breadth of coverage and premium increases can have major implications on our relationship with a carrier. If a carrier has decided not to pay a claim we thought was covered, that would also affect our relationship.

“Having continuity in your relationship with a carrier is important,” he adds. “We have found that shopping programs and changing relationships with carriers from year to year benefits no one. We stress the importance of picking carriers wisely and picking carriers with a guise to building a long-term relation-ship with us and our clients.”

And in the current hard market, Wanat emphasizes that “communication is key, especially when delivering a difficult message. Don’t procrastinate, don’t hide and don’t back out of a commitment.”

What brokers are looking for

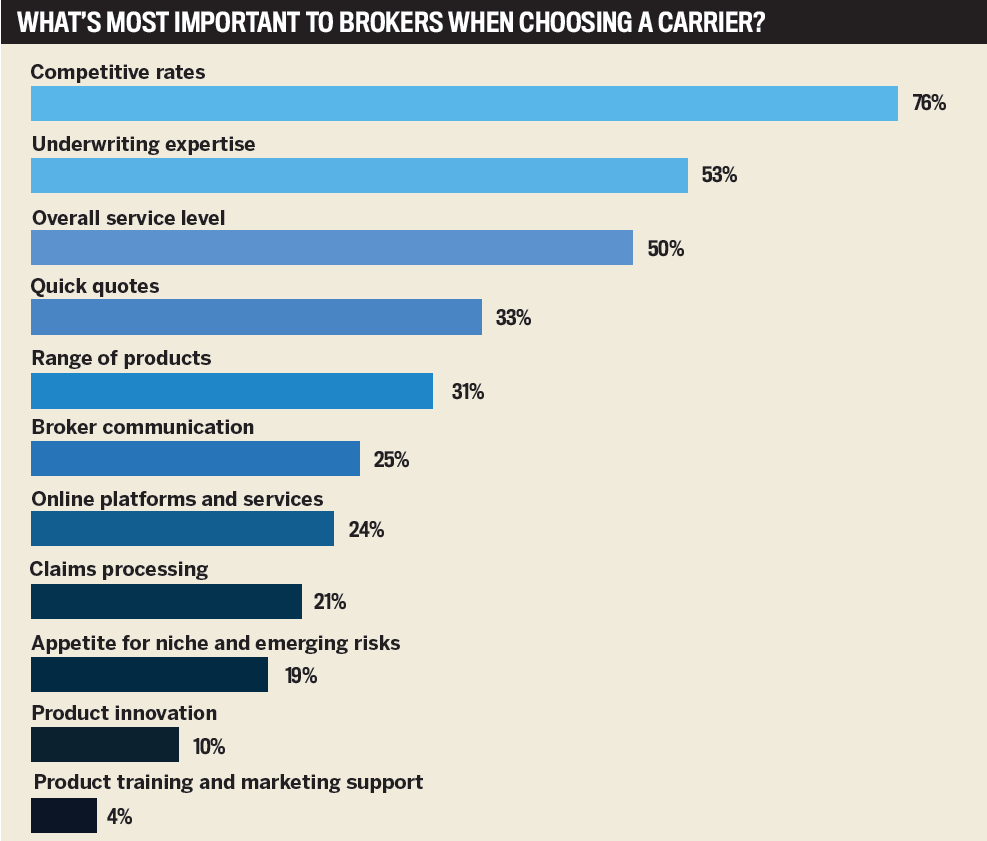

As part of IBA’s survey to determine the best carriers in the US insurance market, we asked hundreds of brokers to name the top three aspects they consider when looking for a carrier partner. Overwhelmingly, brokers named competitive rates as their top priority, which came as little surprise in a market where rates have been rising across the board. General liability, property and auto were all areas where brokers felt carriers should reconsider their pricing. Consistency was also a sticking point: “They need to properly figure out competitive rates and stick with them,” one broker advised.

Underwriting expertise is another high priority for brokers; 53% told IBA it’s one of the three most important things they look for when choosing a carrier. One broker noted that “underwriters that understand coverage” are vital, while another highlighted the need to get away from “strict, inflexible underwriting.” A few brokers mentioned a desire for clearer underwriting guides, while others said underwriting needs to be centralized and streamlined.

Almost equally important to brokers was the overall service they receive from carriers; 50% highlighted this as a top priority. For some, service comes down to the ease of doing business with a carrier, while others expressed a need for service levels that match today’s hyper-competitive customer expectations. “Provide us with services to ease our workload rather than putting more processing work on us brokers,” said one respondent. Another acknowledged the pandemic’s negative impact on service, noting that “since COVID, customer service on the phone has been extremely slow and time-consuming.”

The desire for a speedy response also extends to quoting: 33% of brokers said the ability to receive quick quotes is a top priority when choosing a carrier, and the need for faster quotes came up often when brokers were asked what carriers can do to improve their service. “Greater ease to quotes ... would be very helpful, especially for those of us who work atypical hours for the industry,” one broker said, while another noted the importance of “streamlining good, bindable quotes.”

Carriers’ product range was the fifth most important factor to brokers when choosing a carrier; 31% named it as one of their top three priorities. Product innovation was farther down the list (only 10% of brokers highlighted it as a top quality they look for in a carrier), but their comments made it clear that innovation is key to building a robust range of products. “It’s hard to innovate if carrier partners are not pushing new products,” said one broker. “Get more updated on today’s trends,” advised another.

A quarter of brokers highlighted communication as an important area, and their comments emphasized the need for carriers to keep their broker partners updated regularly via multiple channels, from email and phone to webinars and face-to-face meetings. “We are small and you are big, so we need to rely on you to reach out to us with any changes to ensure a continued successful partnership,” one broker pointed out. Another urged their carrier to “respond to our questions, concerns, issues – it is the worst when you have customers waiting and you get no or slow response.”

Twenty-four percent of brokers said the online platforms and services provided are an important factor when choosing a carrier partner. Several brokers said their carriers could improve by offering broader, faster or more efficient online platforms. However, not everyone was a fan: “The explosion of online raters is unwelcome from my POV,” said one broker. “They are time-consuming, and the return is often not worth the effort.”

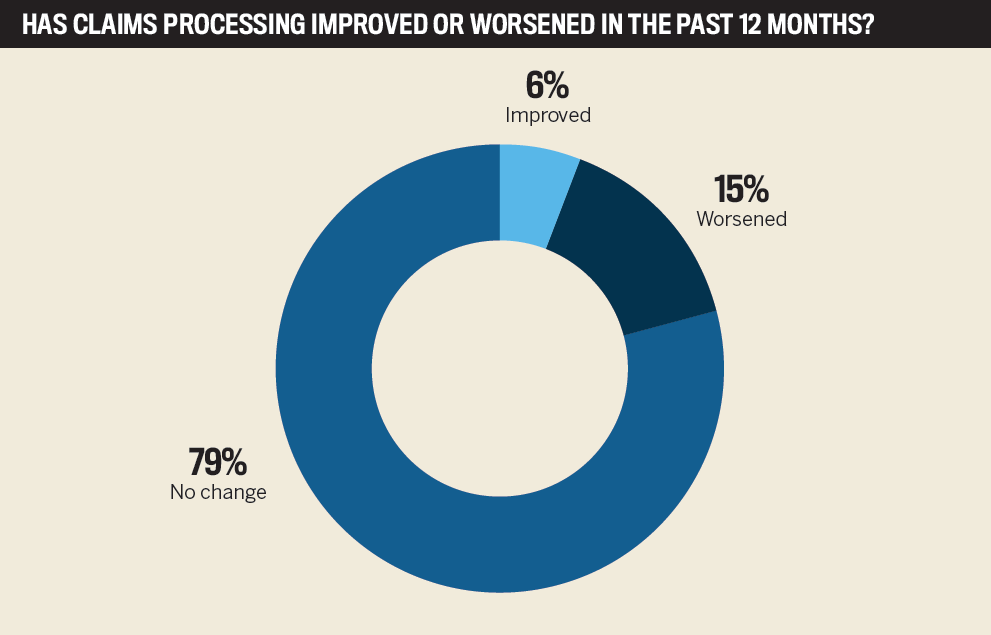

Surprisingly, claims processing ranked rather low this year on brokers’ list of priorities when choosing a carrier; only 21% named it among their top three. A lot of brokers were happy with their carriers’ claims service; 79% told IBA that claims processing has stayed consistent over the past year. Where it was an issue, brokers largely attributed the decline in service to the COVID-19 pandemic and carriers being overwhelmed with claims.

Less important to brokers was a carrier’s appetite for niche and emerging risks, which was rated as a top factor in choosing a carrier by only 19% of brokers, although several mentioned a desire for more niche products when asked what their carriers could do better. Even less important to brokers was the product training and marketing support carriers provide, although several wished for more marketing materials and regular updates on appetite and new products.

5-Star Carriers 2021

Competitive Rates

- AmTrust Financial Services

- Applied Underwriters

- Atlantic Casualty Insurance Company

- Century Surety Group

- Erie Insurance Group

- Evanston Insurance Company

- Nautilus Insurance Group

- Northfield Excess & Surplus Lines, a Travelers company

- Penn-America Group

- RSUI Group

- Safeco Insurance

- The Cincinnati Insurance Companies

Product Innovation

- Applied Underwriters

- Atlantic Casualty Insurance Company

- Colony Specialty

- Erie Insurance Group

- Evanston Insurance Company

- Markel

- Mesa Underwriters Specialty Insurance Company

- Nautilus Insurance Group

- Northfield Excess & Surplus Lines, a Travelers company

- RSUI Group

- Safeco Insurance

- The Hartford

- W. R. Berkley Insurance Group

- Zurich

Product Training and Marketing Support

- Applied Underwriters

- Colony Specialty

- Erie Insurance Group

- Markel

- Nautilus Insurance Group

- Northfield Excess & Surplus Lines, a Travelers company

- Penn-America Group

- Progressive

- Safeco Insurance

- The Cincinnati Insurance Companies

- Zurich

Underwriting Expertise

- AmTrust Financial Services

- Applied Underwriters

- Atlantic Casualty Insurance Company

- Colony Specialty

- Erie Insurance Group

- Evanston Insurance Company

- Liberty Mutual

- Markel

- Mesa Underwriters Specialty Insurance Company

- Nationwide Group (including Scottsdale Insurance Company)

- Nautilus Insurance Group

- Northfield Excess & Surplus Lines, a Travelers company

- Penn-America Group

- RSUI Group

- Safeco Insurance

- Selective Insurance

- The Cincinnati Insurance Companies

- Western World

- Zurich

Range of Products

- Applied Underwriters

- Atlantic Casualty Insurance Company

- Chubb

- Colony Specialty

- Erie Insurance Group

- Evanston Insurance Company

- Liberty Mutual

- Markel

- Mesa Underwriters Specialty Insurance Company

- Nationwide Group (including Scottsdale Insurance Company)

- Nautilus Insurance Group

- Northfield Excess & Surplus Lines, a Travelers company

- Penn-America Group

- RSUI Group

- Safeco Insurance

- The Cincinnati Insurance Companies

- The Hartford

- Travelers

- Zurich

Quick Quotes

- AmTrust Financial Services

- Applied Underwriters

- Atlantic Casualty Insurance Company

- Auto-Owners Insurance Group

- Colony Specialty

- Erie Insurance Group

- Evanston Insurance Company

- Markel

- Mesa Underwriters Specialty Insurance Company

- Nautilus Insurance Group Northfield Excess & Surplus Lines, a Travelers company

- Penn-America Group

- Progressive

- RSUI Group

- Safeco Insurance

- The Cincinnati Insurance Companies

- The Hartford

- W. R. Berkley Insurance Group

Broker Communication

- Applied Underwriters

- Century Surety Group

- CNA

- Colony Specialty

- Erie Insurance Group

- Evanston Insurance Company

- Markel

- Mesa Underwriters Specialty Insurance Company

- Nautilus Insurance Group

- Northfield Excess & Surplus Lines, a Travelers company

- Penn-America Group

- RSUI Group

- Safeco Insurance

- Selective Insurance

- The Cincinnati Insurance Companies

- Zurich

Online Platforms and Services

- AmTrust Financial Services

- Applied Underwriters

- Century Surety Group

- Colony Specialty

- Erie Insurance Group

- Evanston Insurance Company

- Liberty Mutual

- Markel

- Nautilus Insurance Group

- Northfield Excess & Surplus Lines, a Travelers company

- RSUI Group

- Safeco Insurance

- Selective Insurance

- The Hartford

- Travelers

Claims Processing

- Applied Underwriters

- Atlantic Casualty Insurance Company

- Auto-Owners Insurance Group

- Chubb

- CNA

- Colony Specialty

- Erie Insurance Group

- Evanston Insurance Company

- Liberty Mutual

- Markel

- Mesa Underwriters Specialty Insurance Company

- Nautilus Insurance Group

- Northfield Excess & Surplus Lines, a Travelers company

- Penn-America Group

- RSUI Group

- Safeco Insurance

- Selective Insurance

- The Cincinnati Insurance Companies

- Travelers

- Western World

- Zurich

Overall Service Level

- AmTrust Financial Services

- Applied Underwriters

- Atlantic Casualty Insurance Company

- Century Surety Group

- Colony Specialty

- Erie Insurance Group

- Evanston Insurance Company

- Liberty Mutual

- Markel

- Mesa Underwriters Specialty Insurance Company

- Nautilus Insurance Group

- Northfield Excess & Surplus Lines, a Travelers company

- Penn-America Group

- RSUI Group

- Safeco Insurance

- Selective Insurance

- The Cincinnati Insurance Companies

- The Hartford

- Travelers

- Western World

- Zurich

Appetite For Niche and Emerging Risks

- Applied Underwriters

- Erie Insurance Group

- Markel

- RSUI Group

Methodology

For the eighth year in a row, IBA asked brokers to name the top carriers in the industry by rating how well they performed in 11 categories. Brokers evaluated carriers on a scale of 1 (poor) to 5 (excellent) in the following areas:

- competitive rates

- product innovation

- product training and marketing support

- underwriting expertise

- range of products

- quick quotes

- broker communication

- online platforms and services

- overall service level

- claims processing

- appetite for niche and emerging risks

Carriers that received an average score of 4.00 or higher were named a 5-Star Carrier for that category.

Keep up with the latest news and events

Join our mailing list, it’s free!