As a business owner, you cannot predict what’s going to happen in your day-to-day operations – and sometimes, even if you have exercised due diligence and taken all the necessary precautions, workplace accidents can still occur. This is where workers’ compensation insurance plays a crucial role, especially for small businesses weaving their way to profitability.

In this article, Insurance Business discusses the importance of workers comp insurance for small businesses. We will explain how this type of coverage works and how you can get the policy that suits your coverage needs. For industry professionals, we will touch on the attributes that insurance brokers are looking for when searching for a suitable carrier for their clients as uncovered by our special reports team through hundreds of interviews. Read on and learn more about the benefits workers’ compensation insurance brings to small businesses.

Workers’ compensation insurance is a legal requirement in almost all states for businesses with employees, regardless of their size. This type of coverage pays out for the following:

This means that by taking out workers comp insurance, your business is also protected from the financial liability of having to cover these costs out of pocket, which can be a great help given that small businesses and startups typically operate on limited financial resources.

But each state implements different rules on workers’ compensation. You can click on the links in the table below to find out how workers comp laws work in your state.

|

STATE-BY-STATE GUIDE TO WORKERS’ COMPENSATION LAWS |

|||

|---|---|---|---|

In addition, the state decides who handles and sells workers’ compensation insurance policies. These may be the following:

The 10 largest private providers of workers' compensation insurance account for almost half of the entire market. You can click on the link to find out which insurers made our latest rankings.

Workers’ compensation insurance policies have two main parts, according to the Insurance Information Institute (Triple-I). These are:

This is where the insurer agrees to pay any state-required amount of compensation. One important thing to remember is that, unlike other types of insurance, workers comp policies do not have a capped policy amount. This means the insurance company is required to pay whatever amount the business is obligated to because of a workplace accident.

This covers a business against lawsuits filed by an employee for a job-related illness or injury that is not subject to state statutory benefits. Unlike Part One of the policy, this comes with a monetary limit.

Workers’ compensation insurance, however, does not cover every illness or injury that happens in the workplace. Among the incidents that are excluded from coverage are:

Workers comp insurance claims, however, can be rejected for a slew of other reasons, most of which are avoidable. Find out the most common reasons why workers comp claims are denied and what small businesses can do to prevent them in this comprehensive guide.

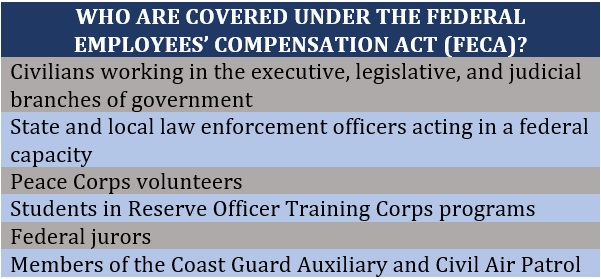

Workers’ compensation insurance also does not cover federal government employees as they already have coverage under the Federal Employees’ Compensation Act (FECA). The table below lists the group of workers covered by this legislation.

Annual premiums for workers comp insurance for small businesses can go for between hundreds to a few thousand dollars, depending on a range of factors. A business with a total payroll of around $100,000, for example, may pay around $700 to $3,000 in workers’ compensation costs each year.

You can also get an estimated cost of how much you need to pay in annual coverage by using this formula:

One important thing to remember is that workers’ compensation rates are set by your state’s rating agency using four main factors. These are:

So, if your small business has a yearly payroll of $85,000 and your workers' comp rate is at $1.50, your annual premiums will be calculated like this:

Your estimated annual premiums for workers’ compensation insurance cost $1,275.

Although most states require businesses with employees to take out workers comp insurance, not all businesses fit this category. According to Triple-I, there are certain types of businesses that may be exempted from getting workers' compensation coverage. These include:

*These types of businesses are given the option to self-insure unless they have employees who are not part of the ownership.

Independent contractors are often legally not considered employees. But Triple-I explains that under workers’ compensation rules in most states, contractors, subcontractors, and their employees are treated as your employees, meaning you may be held liable if they get sick or injured while working for you. To avoid liability, some businesses require independent contractors to carry workers’ comp insurance before agreeing to work with them.

Generally, no. The workers’ compensation system operates a no-fault model, meaning that if one of your employees gets sick or injured while working, they do not have to go the traditional tort route of proving negligence to make a claim. However, this also means that they cannot file charges against your business for the injuries or illnesses they sustain.

The Insurance Business research team conducted several one-on-one interviews with industry specialists and polled hundreds more to get their take on the most important attributes they are looking for when searching for workers' compensation coverage that fits their clients’ needs.

The survey results, which reflect what insurance brokers prioritize the most, can also serve as a guide for small businesses trying to decide which workers comp insurance providers offer the best protection.

Here are the top factors insurance brokers are considering when searching for a provider ranked in order of importance:

You can check out the complete survey results, along with the full roster of this year’s batch of Insurance Business’ five-star awardees for the Top Workers’ Compensation Insurance Companies in the USA here.

Triple-I shared several tips on how small businesses can save on workers comp insurance premiums. Here are some of them:

You can visit, and bookmark, our Workers Comp section for more of the latest news and industry developments in the workers’ compensation insurance space.

What do you think are the advantages of workers comp insurance for small businesses? Have you experienced filing a claim? Feel free to share your story in the comments section below.