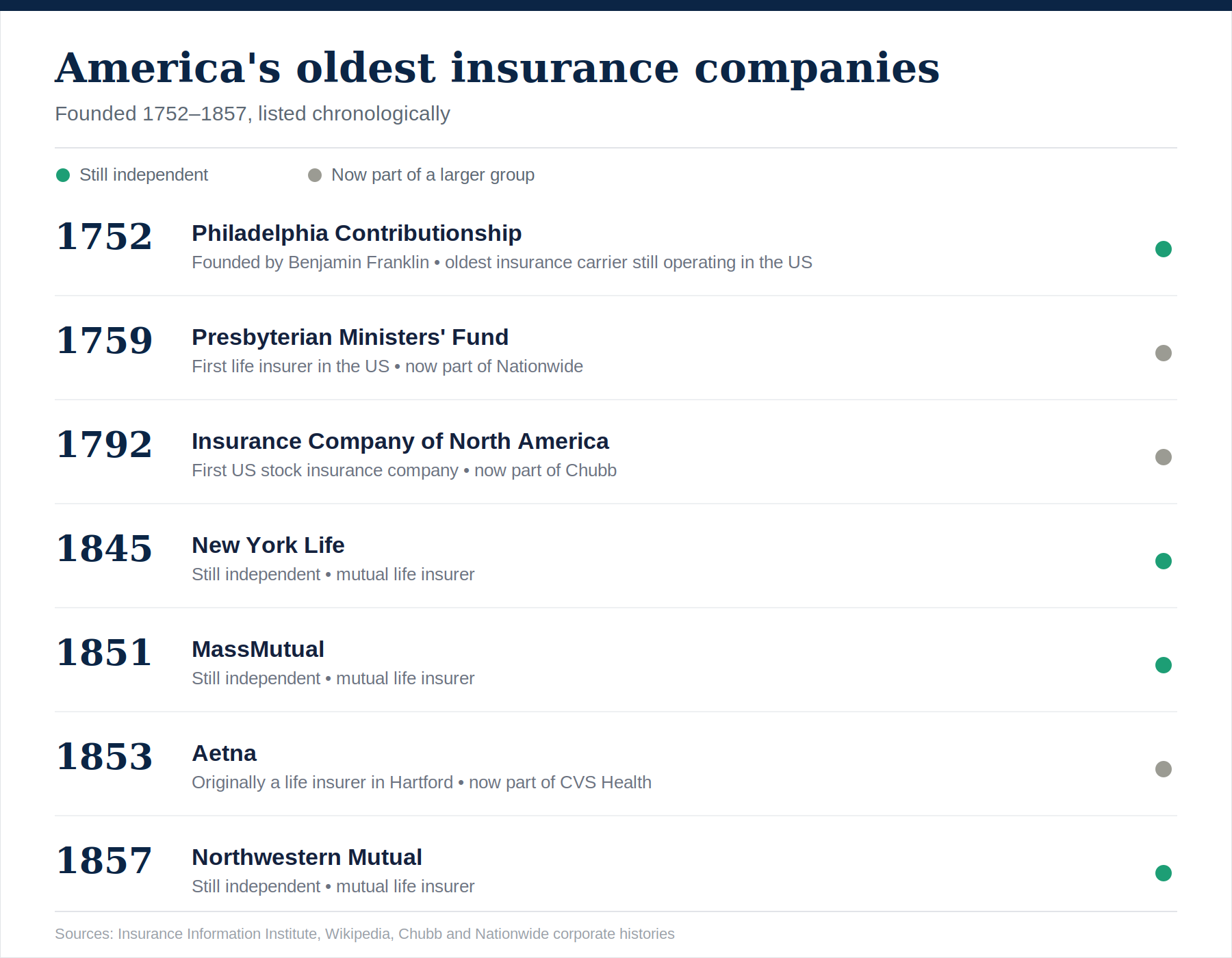

On a spring morning in 1752, a group of Philadelphians led by Benjamin Franklin sat down and did something that, in retrospect, looks a great deal like inventing an industry. They pooled their money into a mutual company, the Philadelphia Contributionship, and promised to rebuild each other's homes if fire ever took them. It was a modest, almost neighborly idea - insurance as a covenant among people who knew each other. Nearly 275 years later, that same impulse to pool risk underwrites a domestic market that, as of 2023 (the most recent verified figure), accounted for roughly 45% of the $7.2 trillion in insurance premiums written worldwide that year, according to Swiss Re figures cited in Wikipedia's overview of insurance in the United States. More current totals almost certainly exist but I was not able to verify a more recent figure, so treat this as directional rather than up to the minute. The story of how the country got from there to here is, in miniature, the story of the American economy itself: its fires, its wars, its migrations, its financial crises, and - increasingly - its climate.

Insurance did not begin as an American idea. It arrived, like so much else, from London, where merchants at Edward Lloyd's coffee house had been underwriting shipping ventures since the 1680s, and where the Great Fire of 1666 had pushed entrepreneur Nicholas Barbon to insure the very houses he was rebuilding, an episode Insurance Business has traced as the true origin point of modern property insurance. American colonists imported the concept almost immediately. The Friendly Society, founded in Charleston, South Carolina, in 1735, is generally recognized as the first insurance company on American soil, though it survived only five years. The Presbyterian Ministers' Fund, chartered in 1759, became the country's first life insurer, according to the Insurance Information Institute's timeline of the industry.

Franklin's Philadelphia Contributionship, formed in 1752, outlasted them all and remains in business today, making it the oldest continuously operating insurer in the country. Franklin's outfit was fussy about risk from the start - inspectors would only cover brick houses set back from trees, since contemporary fire hoses could not reach around them, according to a company history recounted by Empower Brokerage. That instinct - price the risk, don't just absorb it - would define the industry for the next two and a half centuries.

The Declaration of Independence did not interrupt the insurance business; if anything, it accelerated it. By the time the ink was dry in 1776, the Charleston Insurance Company and the South Carolina Insurance Company had already become the young nation's first dedicated marine insurers, underwriting the same transatlantic cargo trade that had made Lloyd's essential in London. At least ten property insurers were founded in the two decades following independence, according to a history of the US market published by Swiss Re, culminating in the 1792 chartering of the Insurance Company of North America, the first American insurer organized as a joint-stock company rather than a mutual.

That structural shift - from mutual societies bound by mutual trust to stock companies raising outside capital - mattered enormously. It meant insurance could scale beyond a circle of acquaintances and follow the country westward, financing the ships, warehouses, and eventually railroads of an expanding economy. By the mid-1800s, according to the Library of Congress's research guide to the industry, most states had a wide assortment of companies writing marine, fire, and life contracts, and the first Black-owned insurer, Philadelphia's African Insurance Company, had been organized in 1810 to serve a community the mainstream market largely ignored.

The nineteenth century gave the industry its formative catastrophes. Urban fires - Chicago's in 1871, Boston's in 1872, San Francisco's in 1906 - exposed how thinly capitalized many insurers were and how badly the industry needed shared standards. The National Board of Fire Underwriters, formed in New York in 1866, began the work of standardizing rates and inspections nationally, and Massachusetts adopted the country's first standard fire insurance policy in 1873, per the Insurance Information Institute's timeline cited above.

Life and casualty products multiplied alongside property coverage. The Civil War produced the first war-risk life policies. Travelers Insurance Company issued the country's first automobile policy in 1898, barely a year after the first pedestrian was killed by a car in New York City - a grim but telling illustration of how new technologies have always generated the next insurance product almost immediately, a pattern Insurance Business has argued is now repeating itself with artificial intelligence. Wisconsin passed the first enduring workers' compensation law in 1911, and Massachusetts made auto insurance compulsory in 1925 - the earliest instance of government treating insurance not as a private convenience but as a public-safety requirement.

Regulation itself was born in this period, and it was born state by state rather than in Washington. New Hampshire appointed the first state insurance commissioner in 1851; New York passed the country's first general insurance law in 1849. That state-centric architecture would prove durable. Even today, insurance in the United States remains regulated primarily by the states rather than the federal government - an arrangement with roots more than 170 years deep.

The Depression and the Second World War reshaped both the demand for insurance and its relationship to government. Franklin D. Roosevelt's Committee on Economic Security, convened amid the economic wreckage of the 1930s, led directly to the 1935 Social Security Act - a form of compulsory federal social insurance that had no real precedent in American life, according to Wikipedia's history of insurance. Health coverage, meanwhile, grew out of necessity rather than policy design: Baylor Hospital in Dallas created a prepaid plan for local schoolteachers in 1929, a model that evolved into the Blue Cross system, and wartime wage controls in the 1940s pushed employers toward offering health benefits as a way to compete for scarce labor without violating those controls - the true origin of the employer-sponsored coverage that still defines American health insurance today, as WTOP's retrospective on the topic lays out.

The most consequential legal event of the era, though, was almost bureaucratic in nature. In 1944, the Supreme Court ruled in United States v. South-Eastern Underwriters Association that insurance was interstate commerce and therefore subject to federal antitrust law - a decision that threatened to upend the state-based system built over the previous century. Congress responded within a year with the McCarran-Ferguson Act of 1945, which preserved state primacy over insurance regulation and granted the industry a limited antitrust exemption, a compromise the Insurance Information Institute credits with "assuring the pre-eminence of state regulation of the industry" ever since.

For most of the industry's history, companies were legally confined to a single line of business - an insurer could write fire coverage or life coverage, but rarely both. That began to change in the 1950s, when states started permitting multi-line charters, allowing the emergence of the diversified national carriers that now dominate the landscape, as noted in Wikipedia's entry on insurance in the United States. Sears, Roebuck & Co. had already anticipated the shift toward mass-market, multi-product insurance when it launched Allstate by mail order in 1931; the company would go on to help pioneer seatbelt and airbag advocacy in the decades that followed, according to Insurance Business's profile of the carrier. Travelers, founded in 1853 to insure railroad and steamboat passengers, extended its firsts into the space age, writing the first policy for a manned lunar mission in 1969, per Insurance Business's company history. Farmers Insurance, founded in 1928 to serve rural drivers overlooked by urban-focused carriers, and American Family Insurance, founded a year earlier for the same purpose in Wisconsin, both grew from single-purpose regional mutuals into national multi-line groups, as detailed in Insurance Business's profiles of Farmers and American Family.

Technology followed the consolidation. Travelers installed one of the first IBM mainframes in the insurance sector in the 1960s, and by the 1980s personal computers had put back-office automation within reach of even small agencies - a slow, cumulative modernization one longtime industry technologist called "evolution, not revolution" in a first-person account written for Insurance Business, a corrective to the notion that the insurtech boom of the 2010s came out of nowhere.

The last quarter of the twentieth century tested the state-based system in new ways. Hurricane Andrew in 1992 and the September 11 attacks in 2001 exposed how concentrated catastrophic risk had become, feeding growth in reinsurance and catastrophe modeling. Hurricane Katrina in 2005 and the 2007–08 financial crisis raised, for the first time in decades, serious congressional interest in federal oversight of insurance. That interest produced the Dodd-Frank Act of 2010, which created a Federal Insurance Office inside the Treasury Department and a Financial Stability Oversight Council empowered to flag systemic risks in the sector - a modest but real expansion of Washington's footprint into a business the states had run almost unchallenged since 1945.

If the twentieth century was about scale, the twenty-first has been about the customer relationship itself. More than $1 trillion flowed into insurtech investment in the years leading up to 2019, according to Willis Towers Watson data cited by Insurance Business, and much of it targeted the same information asymmetry that had defined insurance since Franklin's day. Christian Bieck, global insurance leader at the IBM Institute for Business Value, told Insurance Business that digitalization now lets customers "gather more and more information on their own" than insurers can control, a dynamic he said is turning insurance from something sold into something bought. In a sense, the industry has circled back toward its origins at Lloyd's coffee house, where informed merchants once negotiated coverage among equals rather than simply accepting what an underwriter offered.

Artificial intelligence looks likely to be the next disruption in a lineage that includes the automobile, industrial automation, and the personal computer. Economists surveyed by the Wall Street Journal, in reporting relayed by Insurance Business, note that each prior technological shift eliminated entire job categories - telephone switchboard operators, for instance - while creating others that had no name beforehand, much of that new work landing in insurance and financial services. Harvard Business School's Rebecca Henderson, one of the economists in that survey, cautioned that the scale and speed of the AI transition lack a clean historical analogue, predicting displaced workers will eventually "get very, very angry and change the politics" if the transition is mismanaged.

Two hundred and fifty years after the Charleston Insurance Company began underwriting cargo ships, the industry's newest challenge looks a great deal like its oldest one: matching the price of risk to its true scale. Insured losses from natural catastrophes reached roughly $112.7 billion in the United States in 2024, a 36% increase over the prior year, according to the Center for American Progress, and in California, only about 12% of residential policies included earthquake coverage in 2024, down from 30% three decades earlier - a gap chronicled in reporting on Swiss Re's protection-gap research. Former California insurance commissioner Dave Jones has warned the country is "marching steadily toward an uninsurable future" in the highest-risk regions. Moody's has separately projected that the global economic toll of physical climate risk could reach $41.4 trillion by the mid-2040s, a figure Insurance Business reported alongside warnings that slow-onset perils like heat and water stress are outrunning the products built to cover them.

The industry's response echoes its earliest instincts: innovate the structure of the product rather than simply raise the price. Parametric insurance - which pays out against an objective trigger like windspeed or rainfall rather than assessed damage - has moved from a niche catastrophe tool toward a mainstream complement to traditional indemnity coverage, with the global market projected to reach $34.4 billion by 2033, Insurance Business has reported. It is, in its way, the same logic Franklin's inspectors applied to brick houses in 1752: define the risk precisely enough, and it becomes possible to price it - and insure it - at all.

What is striking about American insurance history is not how much has changed but how little the underlying task has. Every era has confronted the same question Franklin's mutual society faced in Philadelphia: how do you get enough people to share a risk that none of them can bear alone? Colonial merchants answered it with marine policies. Industrial-age cities answered it with fire codes and standardized policies. The New Deal answered it with Social Security. The postwar economy answered it with multi-line national carriers. And the current generation of underwriters, actuaries, and brokers is now being asked to answer it again, for risks - climate volatility, algorithmic decision-making, cyber exposure - that would have been unrecognizable to the men who met in that Philadelphia coffee house nearly 275 years ago, but whose solution, in outline, they would probably still recognize.